This is how much your ETF costs you over the years!

ETFs are popular because of their comparatively low ETF costs, among other things. But what charges do we really have to expect, how favourable are savings plans and how much of our return is actually eaten up by fees for longer investments?

If you are interested in such analyses or simply looking for the latest tips and tricks about your finances, you should also take a look at our free forum for personal loans. There you can exchange ideas with other investors and keep up to date with the latest developments.

ETF costs vs. net return

When we invest our money and take risks, we don’t do it for fun – we want to see a return! It is therefore only logical that we try to avoid all influences that reduce our profits.

Together with taxes and fees for brokers and banks, it is primarily the costs for the various financial products themselves that are causing our income to shrink. However, ETFs have brought about a significant improvement here in recent years.

This is because these funds do not require a large team to manage them: They track indices based on predefined rules. As this works largely automatically, an ETF can get by with significantly lower costs than an actively managed product.

However, ‘low’ is not ‘free’ and even with ETFs, the costs can add up. In addition, the various key figures and different purchase options often cause confusion among investors.

Right on trend: the savings plan

ETFs can be added to your own portfolio either via a single, regular purchase or via a savings plan subscription – both involve different costs. As they are currently enjoying great popularity, we want to take a closer look at savings plans today.

Here, a fixed amount is invested in the desired ETF at regular intervals – usually monthly, quarterly or semi-annually. Smaller amounts are also possible, which may even be less than the price of one unit of the ETF. The investor then acquires shares in the product bit by bit.

To better analyse the costs here, let’s take two different examples: Investor A would like to invest €250 per month in the iShares Core MSCI World ETF, while Investor B is prepared to invest €500.

Example 1: 250 euros in the savings plan

Investor A uses a savings plan for the EUR 250 he wants to invest each month. This will cost him 1.5 per cent. I did not choose this example amount by chance: This is how much is currently charged by ‘traditional’ brokers such as Comdirect or Commerzbank. This results in expenses of 3.75 euros per month or 45 euros per year.

Costs are also charged for the actual ETF. The iShares Core MSCI World charges 0.2 % per year. To make our example even clearer, let’s also assume that this ETF offers us an annual interest rate of 6 %.

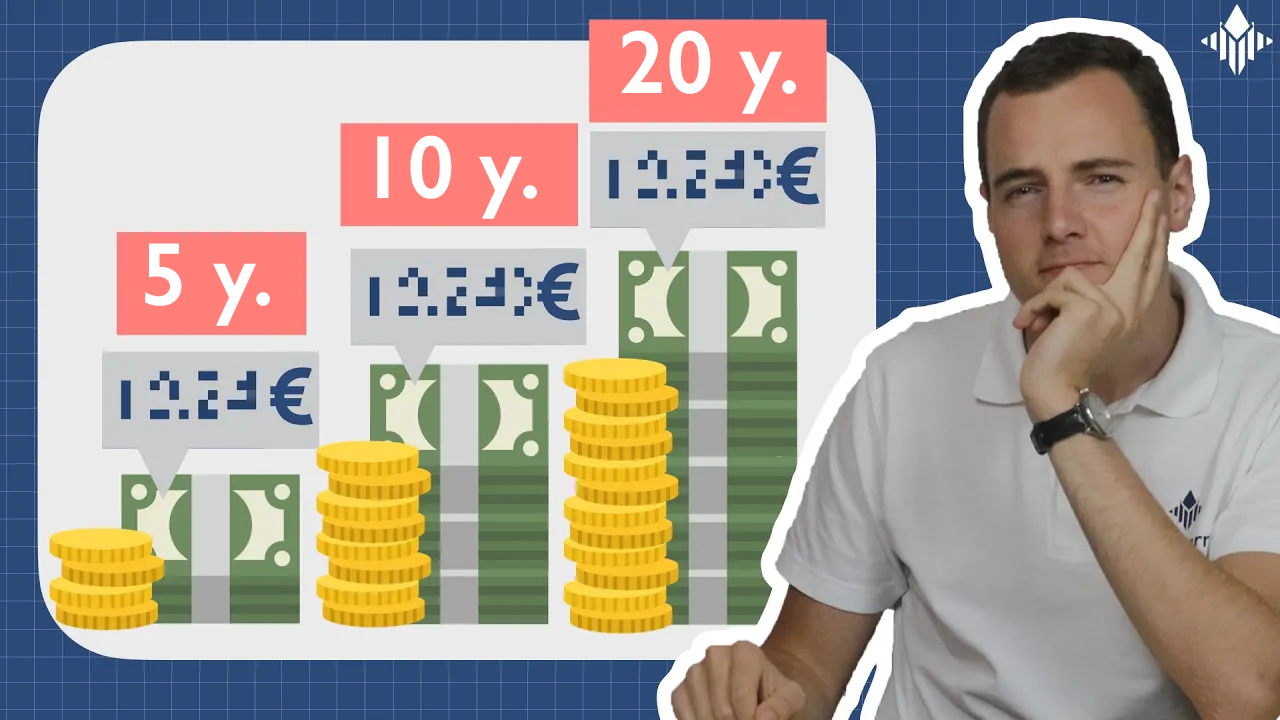

After five years, investor A has saved 17,000 euros in this way. After ten years, it is already 38,000 and after 15 years it is already 65,000. If our investor holds out for 20 years, he can look forward to a whopping 99,000 euros.

As our monthly deposit remains constant, the expenses for the savings plan do not change. After 20 years, investor A has lost a total of 900 euros due to these fees – shown in blue in our chart.

In contrast, ETF costs have naturally risen with increasing capital. After 20 years, this adds up to 2,600 euros, which you can see from the orange line.

This results in the following total costs (TER):

- 334 euros after five years

- 926 euros after ten years

- 1,900 euros after 15 years and

- 3500 euros after 20 years

Example 2: 500 euros in the savings plan

Next, let’s take a look at the costs of an ETF in a savings plan if we can invest 500 euros per month. Investor B invests double the amount and of course has to pay double the savings plan fees: €7.50 per month or €90 per year.

The other values also roughly double, so that after five years we have saved €34,000 and after ten years €76,000. If we invest at this rate for 15 years, we will realise €130,000 and after 20 years we will have €198,000 waiting for us.

It can be even cheaper!

Thanks to today’s much more open market and the offerings of numerous ‘neo-brokers’, ETF costs for savings plans have fallen dramatically. A prime example of this is Smartbroker, which charges just 80 cents for the execution of a savings plan and no order fees.

The difference of just under 3 euros in savings per month quickly becomes noticeable: After five years, investor A can already call €600 more his own in this way! After ten years it is already €2400, after 15 it is already €5,900. With a twenty-year investment, this brings him to an incredible €11,600!

After 20 years, we have 11,600 euros more in our custody account thanks to the Smartbroker price advantage. And that’s only because we’ve saved 3 euros a month on fees. This is because the money saved flows directly into the ETF instead of into its costs and earns interest again directly. It generates income for us instead of going into the pockets of your broker.

If we reduce our costs to a minimum in this way, the effect is even more noticeable at 500 euros per month. In this case, the fees for executing the savings plan do not double, but only increase by 20 cents to one euro.

Due to the favourable price of the smart broker, we can already collect an advantage of 1,300 euros after five years in this scenario. This figure rises to 5,400 euros after ten years, 13.00 euros after 15 years and a massive 25,000 euros after 20 years.

This advantage becomes particularly clear when we compare it with the monthly sum: After 20 years, we have the equivalent of 50 months of additional deposit. With one of the more expensive brokers, this money would be lost to us.

Hidden ETF costs: Spread and co.

In addition to the savings plan costs and the fees for the ETF itself, we unfortunately have to be prepared for other costs. These include, for example, the spread, which depends on the place of execution of the respective financial product.

For example, if you buy ETFs that include US shares, the opening hours of the US stock exchanges are important. If they are closed, the relevant brokers charge a hedging fee – the spread.

These ETF costs are therefore lower if you trade between 15:30 and 22:00, as the stock exchanges are regularly open during this period. If in doubt, you should not hesitate to ask your broker how exactly this is regulated.

Other, often hidden costs include custody account fees or safekeeping fees that some brokers charge. Due to competitive pressure within the industry, such charges are becoming increasingly rare, but they cannot be completely ruled out.

Some brokers also offer negative interest on excessive cash balances. However, these are usually tied to a certain period (e.g. -0.5 % interest if your money has been with your broker for more than 6 months and has not been invested), which you should be aware of and avoid accordingly.

My recommendations

As our example calculation has shown, even the smallest savings in savings plan fees can quickly add up to huge sums. When buying an ETF, it is therefore essential to consider the costs!

Since even the smallest savings are so clearly worthwhile, I therefore clearly recommend using one of the low-cost neobrokers such as Smartbroker if you want to buy ETFs with savings plans.

It’s no secret that I’m a big fan of Smartbroker and its particularly favourable costs, especially for ETFs.