Debitum review: 15% return and more

Debitum Investments attracts investors with returns of up to 15% and an almost perfect repayment record. Sounds too good to be true? I have been investing through the platform for some time now and have invested over €14,000. In this review, I will share my personal experiences with Debitum Investments, potential risks and disadvantages, and what you should look out for.

In brief:

- Debitum is a P2P provider from Latvia that finances business lending. Here, you invest in corporate lending and receive up to 15% interest.

- The provider is rather unknown, but reputable, fully regulated and has been operating for a long time.

- Its small size (around 30,000 users) is deceptive: Debitum is one of the best P2P platforms and my personal experience has been extremely positive.

My Debitum Investments review: Everything you need to know about the platform for corporate lending

P2P lending are rightly considered crisis-proof investments with high returns. So it’s no wonder that the market is growing steadily and more and more investors and platforms are joining. The special thing about the world of personal lending is that it’s quite difficult to keep track of everything!

As a result, an excellent platform such as Debitum largely flies under the radar of investors. Other, less attractive providers, on the other hand, have significantly more users for reasons unknown. To find out more about which service provider is really worth investing in in 2026, take a look at our current P2P lending ranking.

In this ranking, you will immediately find Debitum in first place. With the test winner from Latvia, you can invest in business lending from all over the world. Your capital is made available to companies and in return you receive a very attractive interest rate, which can be up to 15%!

Debitum acts as a marketplace where investors like you and me can connect with lending originators. They, in turn, take care of lending, screening and more. In my experience, this provides significantly greater choice and flexibility!

A few days ago, I increased my investment in Debitum by €1,800, transferring funds from Swaper to the platform. The reason for the transfer was a lack of available lending on Swaper, which meant I had no opportunity to invest. My total investment currently amounts to over €14,000. This makes Debitum the second largest platform in my €107,000 P2P lending portfolio.

For example, you can invest in a huge number of countries, thereby achieving excellent diversification. Debitum offers loans from:

- USA

- Brazil

- Spain

- Portugal

- Turkey

- Denmark

- United Kingdom

- Estonia

- Latvia

- And many other countries

However, you can also divide your investments by sector. For example, companies from the gaming industry, construction, agriculture and forestry, and other sectors are looking for capital. This makes DN an exciting alternative to the typical consumer lending you find at Mintos or Swaper, for example.

This business model has been successful for more than six years and has weathered the coronavirus crisis very well. During this entire period, all loans have been repaid to investors.

The default rate is 0%, which is an excellent figure that, in my experience, few competitors can match. Only loans from Ukraine are significantly past due due to the war – however, these account for only around 2% of the lending portfolio and are not actually defaults, but rather delays.

The most important data at a glance:

| Headquarters | Riga, Latvia |

| Regulation | Regulated by the Latvian Financial Supervisory Authority |

| Founded | 2019 |

| CEO | Erik Rengitis |

| Return for investors | 14.83% (XIRR) |

| Financed credit volume | + 176.000.000 € |

| Number of investors | + 30.640 |

| Financed business lending | + 11.475 |

| Minimum investment | amount €10 per loan |

| Extras | 🗙 Secondary market ✔ Auto-invest 🗙 App ✔ Translation in more languages |

| Repurchase obligation | Yes, for 100% of the capital |

How does investing work at Debitum?

With Debitum Investments, you make your money available to companies and are rewarded with attractive interest rates in return. The whole process works as follows:

- Companies regularly need money for further growth and new investments, but cannot always obtain loans from banks.

- They therefore turn to credit brokers (also known as ‘brokers’) such as Evergreen Capital, Flexidea or Triple Dragon, who work with Debitum. These companies have many years of experience in credit assessment and can quickly examine collateral and other important points.

- If everything looks good, they finance the loan. However, they want to refinance their capital as quickly as possible so that they can grant further loans. They therefore seek investors via Debitum.

- The P2P platform carries out an additional check to ensure that everything is in order with the individual lending. If everything is OK, the process moves on to the next step.

- DN now combines several such lending (at least five) into a so-called ‘asset-backed security’. Each of these products has a term, interest rate and a penalty interest rate in case the borrower does not repay on time.

- Investors like you and me can now invest our capital in these asset-backed securities. In return, we receive the promised interest.

- At the end of the term, the invested money is repaid. If there are any delays, DN takes care of collecting the funds and penalty interest.

If a borrower defaults completely and is unable to repay your money, the respective broker will step in: Each of these lending originators must offer a 100% repayment guarantee and repay the money to you in the event of default. Debitum also ensures that the originators actually have sufficient capital and limits the number of loans they are allowed to issue.

I am not the only one who has had very good experiences with this security concept: every investor has always received their money as planned, only the loans from Ukraine are still pending.And that has been the case since the beginning over 6 years ago!

The Debitum Investments platform and the lending originators who are active there naturally also want to make a profit. They take a small portion of the interest and invest it themselves in the respective loans. This last point is particularly important because, through their direct involvement, the brokers have a vested interest in ensuring that everything runs smoothly. After all, they themselves have a lot to lose!

The structure looks complex at first glance, but it is actually very simple: loan brokers arrange loans that you can invest in via the network. Numerous verification mechanisms ensure security.

This business model seems to be working for the initiators; however, DN itself has recently been in the red. This is not surprising, given that the company is still on a growth trajectory and has corresponding expenses.

My experience with asset-backed securities

If you already have experience with P2P lending, you will need to rethink your approach with Debitum: here, you do not invest in individual lending, but in so-called ‘asset-backed securities’. These are packages of at least five loans with similar characteristics that have been put together by DN.

In practice, this does not change your profits, but it does have significant advantages for your security:

- Asset-backed securities may only be issued by providers who hold an investment broker licence.

- Debitum is one of the few platforms (in my experience, there are only three other providers in the whole of Europe) that hold this licence.

- Licensing goes hand in hand with significantly stricter controls by the financial supervisory authorities.

- Investors also benefit from better security measures. In the event of the platform’s insolvency, your uninvested capital is protected by a deposit guarantee of up to €20,000.

- Since at least five loans are always grouped together, the risk for investors is reduced. Even if one P2P lending defaults, four others remain.

Overall, asset-backed products are a real blessing for investors. Many platforms are a black box for us, where we never really know what the financial situation is and whether our money is in good hands. At Debitum, on the other hand, everything is transparent thanks to the intensive controls that come with the investment broker licence.

You can find out more about the problems and risks associated with some P2P providers in my report on platform risks.

New offer at Debitum Investments: 12% through forests!

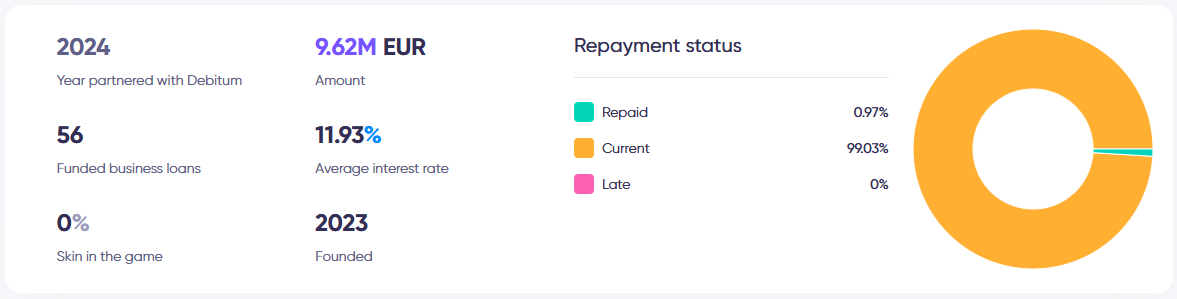

Since 2024, a new lending originator, the Latvian Forest Development Fund, has been available on Debitum Investments. It is already the second provider for investments in forest areas on the platform. Attractive interest rates, excellent collateral and a good opportunity for diversification await you here!

Prices for (construction) timber have risen massively in recent years, and forest owners are benefiting from this. This has not gone unnoticed by large investors:

- Private equity firms, private investors and companies such as IKEA are buying up huge areas of forest.

- They want to acquire thousands of hectares at a time.

- Latvian forests cover 50% of the country’s land area. Around 54% of this is privately owned.

- The owners often only have very small areas at their disposal, which means that the forests are highly fragmented.

- Latvian Forest Development Fund buys up small areas of forest, improves access and management, and combines them into larger plots.

- This optimisation enables the fund to generate high returns on the land.

- These ‘forest packages’ are then sold to large investors at a considerable profit.

This business model is highly effective: with an acquisition volume of €32 million, the company manages a total of €49 million in capital from investors!

The company currently owns 659 properties with a total area of 6,430 hectares of forest and has a repayment rate of 100%. This is a significant increase on the previous year and demonstrates the successful course that Latvian Development Funds is pursuing.

These acquisitions are financed through Debitum Investments. Investors have already had very good experiences with Foresto on the platform. This credit initiator pursues the same concept, but on a significantly smaller scale.

Interest in the Latvian Forest Development Fund is correspondingly high: €9.6 million had already been invested in June 2025, with an average interest rate of 11.9%!

Future prospects for the Latvian Forest Development Fund

In my opinion, the LFDF is a particularly exciting credit facilitator, as the company is active in one of the most attractive growth industries! It has struck a chord with forest owners, P2P investors, and large investors:

- Forest owners can request a sales offer via an online form that is distributed through advertisements.

- Demand is so high that the Latvian Forest Development Fund can barely keep up with all the inquiries.

- The number of projects and funds invested on Debitum is growing explosively: the company currently manages €49 million from investors.

- By selling logging rights, leasing usable land, and reselling, the company achieves a return of 35%.

- LFDF pays around 12% interest to Debitum users.

- Cheaper bank loans are expected to ensure even greater profitability in the future, but Debitum investments will continue to be part of the mix due to their flexibility.

Overall, the signs point to growth. The fund’s economic situation appears to be very good, which, in my experience, is the most important security for investors!

New feature 1 at Debitum: An exciting loyalty program

Debitum’s new loyalty program now replaces the previous cashback feature. With this program, investors receive an additional 0.5% more than before on investments of €6,000 or more. From €25,000, the interest rate increases by 1%, and from €50,000, it increases by as much as

What makes this loyalty program special is that you can also unlock the different levels by inviting friends to the platform if you don’t have the required amount. In my case, I could either invest another €12,000 or invite three more friends to reach the next level.

As an “Investor,” you also gain deeper insight into the benefits you enjoy as an investor with Debitum. I receive an annual loyalty bonus of 0.5% and a €20 bonus when I recommend Debitum to a friend. In addition, I receive a cashback of 1%, up to a maximum of €100.

The loyalty program on Debitum is definitely an attractive incentive to actively use the platform and recommend it to others. However, given the already very attractive base interest rates that investors receive at Debitum, the loyalty program is not a must for everyone.

New feature 2 at Debitum: Investing in land

Debitum is expanding its platform with another exciting financing partner. Investors now have the opportunity to invest in agricultural land in addition to forests. To this end, the platform has secured the financing partner and bond issuer Baltic Terra.

This investment opportunity offers investors an even more diversified portfolio and supports Debitum’s goal of connecting investors with real economy assets in order to generate sustainable returns.

The Baltic Terra investment fund focuses on farmland in Latvia, as the country is one of the most undervalued agricultural land markets in the EU. The fund acquires agricultural land and increases its productivity and structural quality in order to farm it professionally. This enables sustainable current income and long-term value appreciation to be achieved.

It can be well worth it for investors to invest in agricultural land. According to the provider, it is considered one of the most resilient real assets for investors.

Important characteristics of agricultural land:

- Lower volatility compared to financial markets

- Natural inflation protection

- Real collateral

- Returns driven by food production and land scarcity

In addition, land prices in Latvia are still well below the level in Western Europe. This results in long-term growth potential for investors.

Security for forest investments

The Latvian Forest Development Fund offers you a comprehensive security concept for your investment:

- The forest areas themselves serve as collateral and can be sold in the event of payment difficulties.

- As is customary with Debitum, we have first-rank claims for investors in the event of bankruptcy of the credit originator.

- Debitum Investments obliges LFDF to repay late or defaulted loans or replace them with equivalent products through its buyback guarantee.

Additional security is provided by the impressive growth and good economic situation of LFDF: although it is still a relatively young company, it is already operating profitably!

The fact that this is a serious project is also demonstrated by the career of its owner, Janis Upeniks: some time ago, he moved from his role as CEO of the Latvian Forest Development Fund into politics.

As Parliamentary Secretary, he now holds the second-highest position in the Latvian Ministry of Finance. I was recently able to meet him in person here.

Register and secure your bonus – here’s how it works!

Want to get started with what is arguably the best P2P platform and earn high interest rates? Nothing could be easier! Registration takes just a few minutes. Here’s how it works:

1. Use the bonus link and register

Start with my link to secure an additional 1% return!

This will take you to the DN homepage, where you can create your account by clicking on ‘Register today’. Start by entering your name, email address and a password.

You will then receive an email in your inbox containing a confirmation link.

2. Confirm identity

A platform that is as strictly regulated as DN must, of course, verify the identity of its customers. To do this, you will need to provide proof of identity.

This works via the camera on your mobile phone, tablet or computer. The name you provide must match the information on your passport/ID card/residence permit.

Once you have photographed your ID document, you will need to record a short video of yourself. This allows DN to verify that you are a real, living person. Alternatively, you can also verify your identity via video call with a service representative.

How do deposits and withdrawals work?

Once your account is open, you can deposit money and start investing. This works via bank transfer from any bank account. You only need €10, which is the minimum amount per lending. In my experience, however, it makes much more sense to invest a larger amount and spread it across several lending. In my experience, there are no defaults at DN, but delays in repayment are possible. Better distribution therefore gives you much more flexibility.

I have been active with Debitum Investments for several years now and currently have over €14,000 invested. All loans in my portfolio are currently at 100%, meaning none are in arrears. This reliable punctuality is one of the biggest advantages for investors and one of the most important reasons to use Debitum.

As far as interest rates are concerned, I have increased them every year since I started with Debitum in 2023. In the table below, you can see how my interest rates have developed and also the total amount I have already earned this year. I expect that I will exceed last year’s amount of €1,386.21 again this year.

Current interest rate development at Debitum since 2023

| 2023 | 2024 | 2025 | 2026 | TOTAL |

| 102,76 € | 502,63 € | 1.386,21 € | 126,77 € | 2.118,37 € |

My personal interest rate is currently 12.69%, which is higher than what a new investor can expect. This is mainly because the platform has become increasingly lucrative in recent years and is gradually paying out higher interest rates. The average return rose from 9.08% in 2023 to 10.53% in the following year and 11.40% in 2025. All this with stable repayments. last year 2025. All this with stable repayments.

Depending on which credit packages you choose, even higher profits are possible. Some loan packages offer interest rates of 15 or even 16%, which you can increase by another percentage point with my sign-up bonus.

Safety and risks associated with Debitum

If you already have some P2P experience, you know that lending always involves risk:

- If an individual borrower is no longer able to make their repayments, the platform or the credit broker steps in so that investors do not suffer any losses.

- However, if there are widespread payment defaults, as was the case during the COVID crisis, for example, the credit brokers may find themselves in financial difficulty. Your capital is then at risk!

- An entire platform can also become insolvent and may no longer be able to make outstanding payments.

- In addition, there is always a risk of fraud, although this is likely to be extremely low with P2P lending: the requirements for opening your own platform are simply too high.

Every provider tries to combat these risks with security mechanisms of varying complexity. Through my investments in dozens of P2P offerings, I have gained extensive experience with various forms. For me, there is no question that Debitum currently manages the risks of the lending business best!

This works in several steps:

1. Selection of credit brokers

DN is a marketplace where various credit brokers can obtain money from investors and pass it on to borrowers. Only a very small number of these providers are currently available on Debitum. This is not due to low demand, but rather to the extensive selection criteria of the Latvians!

Only providers who can comply with the platform’s strict guidelines are permitted. The Latvian Financial and Capital Market Commission also monitors and ensures that only reputable credit brokers are approved.

2. Control of the amount of credit

Once a credit broker has been approved on the platform, Debitum Investments keeps a close eye on the provider. The number of loans that an individual service provider is allowed to offer is limited: sufficient capital must be available to cover repayment from their own pocket in the event of an emergency!

3. Regulation of lending

The loans are additionally reviewed before being pooled into asset-backed securities and offered on Debitum Investments. In fact, there are three review bodies:

- The loan originator checks before passing the loans on to DN

- DN also checks before the loans are pooled and released for investment

- The Latvian Financial Supervisory Authority imposes strict requirements on lending, which are also incorporated into the review process.

Investors also enjoy the protection of the EU deposit guarantee. Unlike the higher German deposit guarantee, this only applies to amounts up to €20,000. Money that is in your Debitum account and has not been invested is protected up to this amount even in the event of insolvency.

Good to know:

Asset-backed securities are not part of a P2P provider’s special assets. In the event of insolvency, you cannot simply transfer them to another provider, as you would with a stock portfolio. However, due to strict regulations imposed by financial authorities, there is a good chance that investors will not be left empty-handed in this case either.

Advantages and disadvantages of debitum

My personal experience has given me a very positive impression of Debitum Investments. I would therefore like to start by listing the advantages:

- Very high interest rates of up to 15%. In some cases, even 16% is possible.

- Reliable payouts, even in times of crisis.

- Access to various countries and companies that you can finance. This makes it easy to achieve excellent diversification.

- Penalty interest for borrowers in the event of late payment. This can significantly increase your overall return.

- Platform fully regulated by the Latvian Financial Supervisory Authority with its own investment broker licence, fast and open communication and audited annual reports. In my experience, no other provider offers better transparency!

- Very low minimum amount: With €10, you can invest in a package of five or more loans, which corresponds to a total of €2 per loan. This allows you to diversify your capital very widely without any difficulty!

- Your uninvested capital is protected by deposit insurance up to an amount of €20,000.

- Asset-backed securities instead of individual loans: You invest in P2P packages, which increases your security and makes the whole process much easier.

- No cash drag: In my experience, there are always enough loans available so that your money does not lie around unused and depress your returns.

- The customer service is above average. You can reach the staff by phone, live chat or email. In addition, every investor can visit the company and take a look at the various projects in which you can invest. I was also able to take a trip to Latvia and get a first-hand impression.

- Very good bonus programme: With my registration link, you can secure an additional 1% interest.

Of course, there are also disadvantages. These include:

- With 30,000 users, the platform is still relatively small and recently posted a loss of €360,000. While this is no cause for concern, you should keep an eye on the business figures in the long term: DN cannot lose money indefinitely…

- There is no secondary market, so early exit is not possible. Your money is therefore tied up for some time – in the event of payment delays, even longer than expected.

- A German translation is available, but it is still very rough.

- The three Debitum founders launched a cryptocurrency of the same name in 2018, generating revenues of around €17 million. The coin was supposed to provide buyers with a regular return. However, it turned out to be a classic ‘rug pull’: the trio converted their shares directly into cash, the price collapsed and the unsuspecting investors lost 97% of their total capital. Although this episode has no impact on the company itself, it does not exactly inspire confidence.

As already mentioned, Debitum is known for its reliable and punctual payments at high interest rates. Only the Ukrainian lending, which account for around 2% of the current portfolio, cannot be repaid at present due to the ongoing war.

However, there are now also positive developments regarding the restructuring of these loans, as a subsidiary of Debitum has taken over the outstanding debt. According to the chart below, investors’ funds will be repaid as soon as martial law ends. This is not possible before then.

Community experiences with Debitum

Of course, I’m not the only investor who has had experience with Debitum! The opinion of the community seems to be overwhelmingly positive, which is not surprising given the 15% interest rate and zero defaults. Typical feedback looks like this:

Of course, there are also doubts and concerns, particularly regarding the medium- and long-term future prospects of the platform:

Given Russia’s ongoing war of aggression against Ukraine, there is justified concern that Russia could attack Latvia at any time. If this scenario were to occur, it would likely also have an impact on forest areas and thus on investors’ investments.

In this case, an investment in Debitum would also have to be reevaluated. The geopolitical situation should therefore be monitored continuously in order to stay up to date.

Conclusion: Debitum seems to be the best P2P platform at the moment!

However, there are also disadvantages. A significant disadvantage, in my view, is the lack of a secondary market. Investors have been promised this for years, but nothing has materialized so far. I think the problem here lies with the Central Bank of Latvia, which imposes strict regulations, making it difficult to incorporate new features.

This means that your capital is potentially tied up for a long period of time. If there are any defaults, the waiting time is extended even further. However, borrowers have to pay a penalty interest rate, which can increase your return. Investors who want to access their money at any time are likely to have a better experience with providers such as Monefit.

All in all, however, I am more than satisfied with Debitum. Over the last few years, I have achieved an impressive real return of 13.5%, which is definitely something to be happy about. I am confident that I will continue to invest money on Debitum, especially when other platforms are struggling, e.g., with no loans available for investment.

It is therefore not surprising that DN also took first place in my current P2P platform ranking!

FAQ – Frequently asked questions about Debitum experiences