My Monefit review in 2026: How reliable is a 10.5 per cent interest rate?

With Monefit’s SmartSaver, investors currently have the opportunity to earn up to 10.5 per cent interest per year, with daily payouts. I’ve been using the platform since the very beginning and have had a positive experience with Monefit so far. But how secure is Monefit really?

Its parent company, Creditstar, reports record profits in its annual accounts, but also record levels of debt. I have therefore taken a critical look at Monefit. In this review, you’ll find out whether the platform is worth it for you or whether you’d be better off with alternatives.

In brief:

- Monefit is one of the P2P platforms offering higher returns. Investors can earn up to 10.5% per annum.

- The parent company, Creditstar Group, is experiencing strong growth, thereby also bolstering investor confidence in Monefit.

- My experience with Monefit shows that the platform reliably pays interest, which, through consistent investment, contributes to sustainable wealth accumulation

- I have already invested over €14,000 and earn around €100 in interest each month, which I can withdraw daily if I need to.

My Monefit review: What you need to know about the platform

On Monefit, investors invest in loans from the Creditstar Group. The platform was founded in 2023 and now has over 48,000 investors, who earn interest of between 7.5% and 10.5% per annum, depending on the product.

In 2025, the average investment stood at €15,900 per investor, representing a substantial increase of €6,800 and demonstrating that the platform is increasingly attracting capital from investors.

Monefit is now available in 30 EU markets as well as Switzerland. Most investors come from Germany, Switzerland, Austria, Spain and Estonia.

What makes Monefit special is its combination of flexibility and attractive returns. Whilst many higher-yield investments either have a fixed term or restrictions on access to capital, Monefit allows for easy management of the investment with daily access to the balance.

Furthermore, investors do not have to select loans themselves, but instead automatically invest in the Creditstar Group’s loan portfolio. This makes Monefit an attractive option for investors who wish to enjoy a high degree of flexibility with minimal effort.

Key information at a glance:

| Foundation | 2023 |

| Head office | Estonia |

| Parent company | Creditstar Group |

| Investors | 48.000+ |

| Volume of financed investment | €450+ million |

| Return | approx. 7.5–10.5% p.a. |

| Minimum investment | 10 € |

| Auto-Invest | Yes (automatic portfolio allocation) |

| Secondary market | No |

| Buyback Guarantee | No |

| Group guarantee | No |

| Regulation | Yes |

Investing in loans on Monefit: The pros and cons

As with any P2P platform, Monefit also has pros and cons that are worth mentioning. Let’s start with the pros:

- High flexibility: As a SmartSaver investor, you can withdraw your balance flexibly at any time. This sets Monefit apart from platforms where capital is tied up for a fixed term.

- Attractive interest rates: Monefit is one of the P2P platforms offering attractive interest rates. Depending on the product, investors can earn interest rates of between 7.5% and 10.5% per annum.

- Daily interest crediting: Interest is calculated daily and credited to your balance. This means that, as an investor, you automatically benefit from the compound interest effect.

- Quick payouts: With SmartSaver, you can have amounts of up to €1,000 paid out immediately, which is already sufficient for many investors.

- Automatic reinvestment: You can automatically reinvest the interest you earn. This allows you to benefit from the power of compound interest and grow your assets even faster.

- Regulation: The companies within the Creditstar Group are regulated in the respective countries in which they grant loans. The group ensures that all lending complies with the applicable legal requirements and is carried out in accordance with the principles of responsible lending.

The disadvantages of Monefit include:

Limited transparency: As investors do not invest directly in individual loans, it is less easy to trace the specific use of the funds than on traditional P2P platforms.

High dependence on the parent company: Monefit’s performance is largely dependent on the financial success of the Creditstar Group. Whilst the company is currently performing well, any financial difficulties could have a direct impact on Monefit investors.

No buyback and no group guarantee: Unlike many other P2P platforms, Monefit does not offer a traditional buyback guarantee for individual loans. Nor is there a group guarantee.

No secondary market: Investors cannot buy or sell loans on the secondary market. Instead, they are reliant on Monefit’s regular disbursement processes.

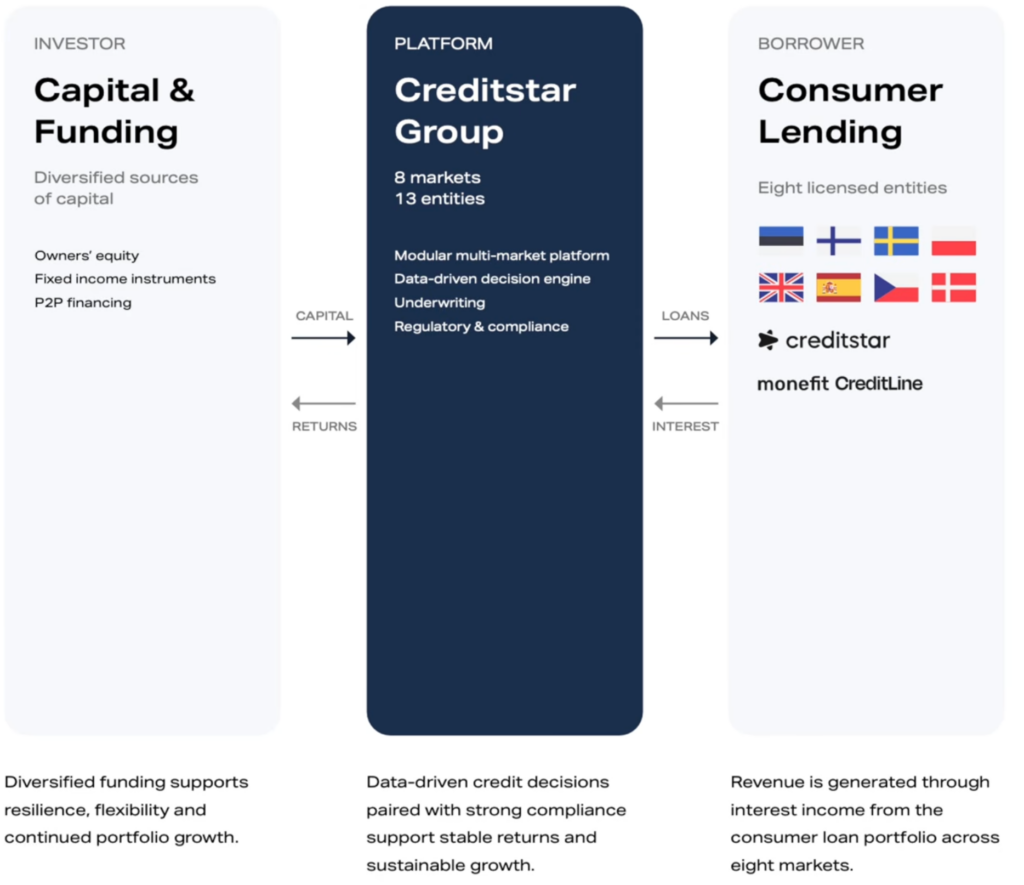

How does investing in Monefit’s consumer loans work?

The way the consumer loan platform works is simple:

- The parent company, Creditstar, raises capital for the group via bonds and P2P platforms.

- This capital is used to grant loans to consumers in what are now eight European countries, in all of which Creditstar is regulated:

- Estonia

- Finland

- Sweden

- Denmark

- Poland

- United Kingdom

- Spain

- Czech Republic

- The capital invested is automatically spread across a wide range of loans within the Creditstar Group, meaning investors do not have to select individual loans themselves. This diversification reduces the risk of individual loan defaults and can result in a more stable overall return.

- Before granting a loan, the Creditstar Group assesses borrowers’ creditworthiness based, amongst other things, on their income and financial situation. The loans are then repaid in monthly instalments, including interest and fees. Depending on the specific loan product and country, the total cost of the loan can amount to around 30 per cent over the term.

- Repayments made by borrowers form the basis for interest payments to SmartSaver investors. Depending on the investment product chosen, returns of up to 10.52% p.a. are possible. A portion of the proceeds remains with Monefit or the Creditstar Group

An interesting observation for me: more than half of all invested funds go into what are known as “Vaults”.

Vaults are customisable sub-accounts where money is held for a fixed term, for which investors generally receive higher interest rates of up to 10.5%. A true sign of investors’ confidence in Creditstar and Monefit.

How your wealth grows on Monefit

Monefit’s SmartSaver is a simple investment product that allows you to build your wealth in a targeted and straightforward way. This is also reflected in all the reviews for Monefit.

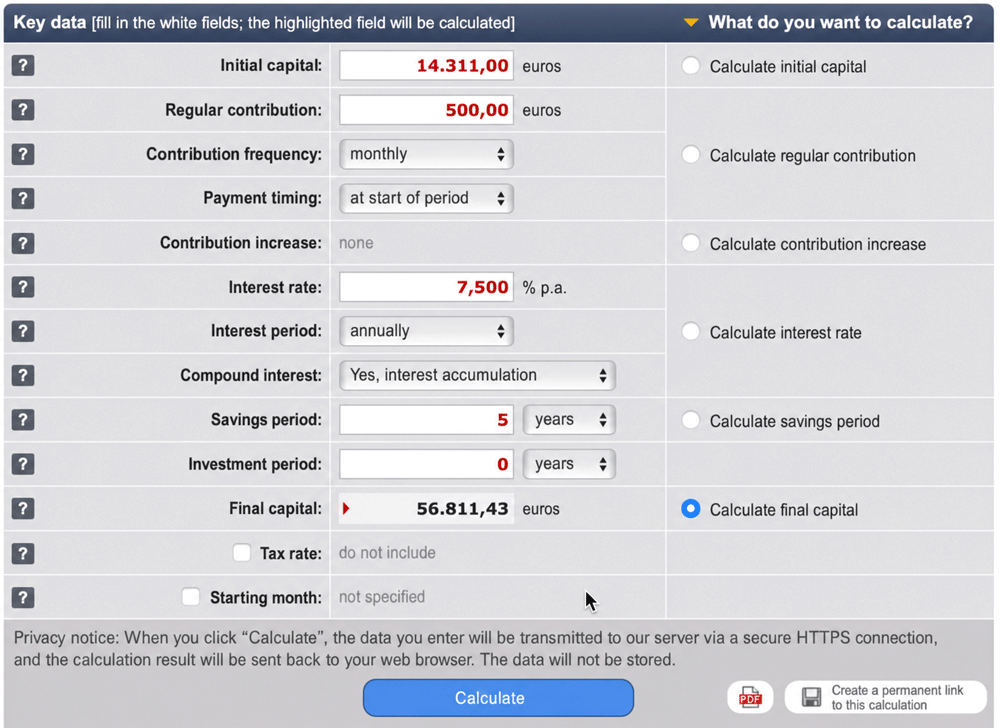

My current portfolio stands at €14,311. Assuming you start with this amount and invest €500 a month at 7.5%, you would have accumulated over €56,000 after 5 years (excluding tax).

If you stay disciplined and invest for a full 10 years, your assets would grow to a total of €117,826. So you can see that investing regularly in attractive asset classes is definitely worthwhile.

Creditstar Group Review: Just how profitable is the parent company really?

Creditstar Group’s annual accounts have been audited by KPMG and are therefore prepared in accordance with IFRS. This alone demonstrates that this is a high-quality and trustworthy document.

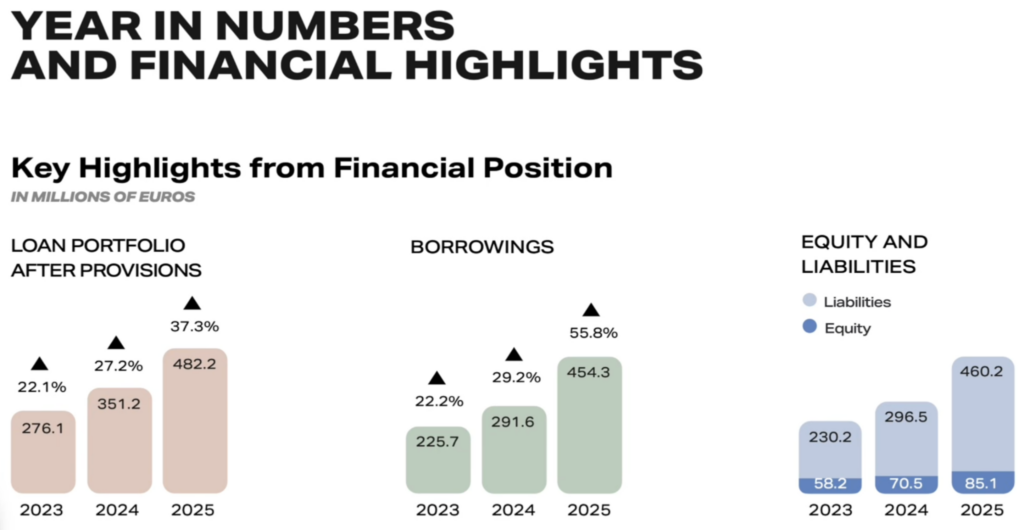

And even a quick glance at Monefit’s latest annual accounts reveals that all of the company’s indicators are showing a positive upward trend:

- from the loan portfolio, which has risen to €482 million over the last two years,

- to the increased interest rates that Monefit itself pays out

- and to turnover, which has broken the €100 million mark for the first time.

- Profit: Another positive aspect is that the company’s profit has almost doubled from €7.2 million in 2024 to €13.5 million in 2025! It must be noted, however, that this was achieved by taking on a considerable amount of debt, as can be seen under the ‘Borrowings’ section in the figure above.

- Debt ratio: The trend in debt becomes clear when looking at the net debt-to-equity ratio. According to the terms of Creditstar’s bond agreements, debt may rise to a maximum of five times the equity before the bond matures.

At Creditstar, debt now stands at 4.9 times equity. The company is therefore operating at the absolute limit of what is contractually permitted. Whilst an increase in debt strengthens returns for investors, it also significantly restricts the scope for taking on further debt.

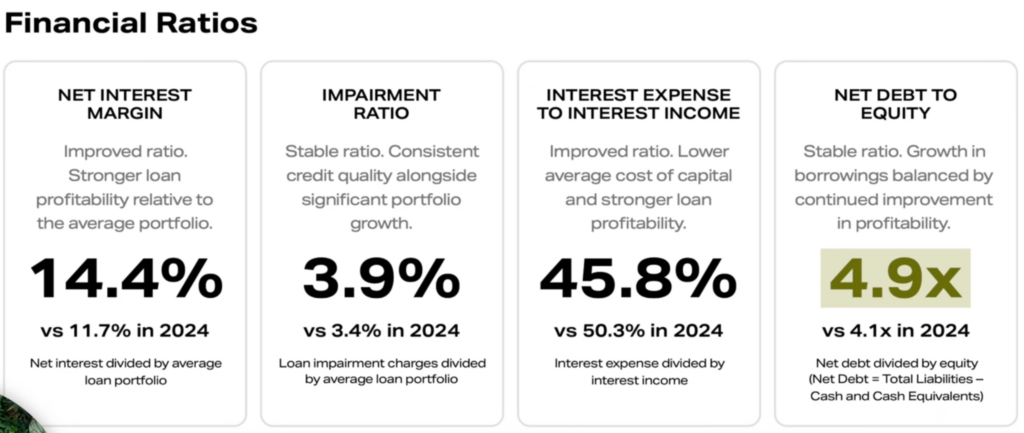

- Margin: In 2025, Creditstar’s loan portfolio achieved a margin of 14.4 per cent, which is a very healthy figure.

- Compound annual growth rate (CAGR): The Creditstar Group’s loan portfolio has grown by an average of 27.2% per year since 2020. This also represents very impressive growth for Monefit’s parent company.

- Registered users: As at 31 December 2025, there were a total of 1.7 million registered users, representing an increase of over 280,000 users compared with the previous year.

All in all, it can definitely be said that the Creditstar Group has steadily established itself in various markets in recent years and continues to achieve strong growth. Investors should, however, keep an eye on the group’s debt ratio, as it is currently walking a very fine line.

Monefit Risk

The Creditstar Group’s annual financial statements also show how punctually the respective loans are repaid, allowing investors to draw conclusions about the platform’s reliability.

The loans are divided into three tiers:

- Tier 1: Around 83% of the total loan portfolio was repaid on time, i.e. without even a single day’s delay. For 4% of the loans, there was a delay of up to 30 days.

- Tier 2: Around 1.8% of loans were delayed by between 31 and 90 days. This corresponds to approximately €10 million.

- Tier 3: Around 11% of the total loan portfolio was delayed by more than 90 days, which amounts to €58 million and represents a decrease compared with the previous year.

These thoroughly healthy figures clearly demonstrate that Creditstar has its credit risk under control, which is a positive sign from an investor’s perspective.

To be fair, it should be noted at this point that €27 million in loans were written off in 2025. There are therefore still some loan defaults, although this is common for P2P platforms.

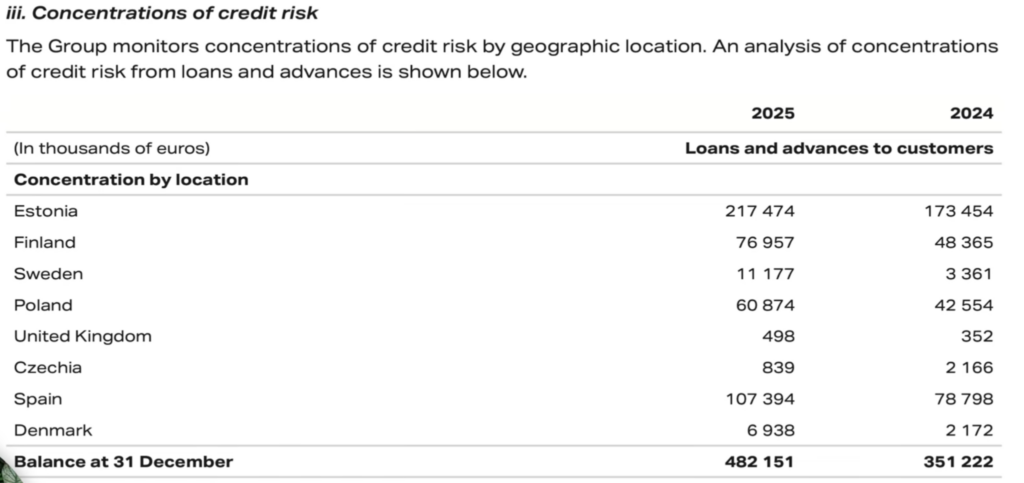

A look at the geographical distribution of the loans shows that the home market of Estonia remains the largest, followed by Spain, Finland and Poland. The loans are therefore also geographically diversified, which helps to reduce country risk.

Creditstar is therefore not only profitable but also strong in terms of the quality of its loan portfolio. Sounds perfect, doesn’t it? Unfortunately, on closer inspection of its liquidity, the enthusiasm wanes somewhat.

Monefit Liquidity

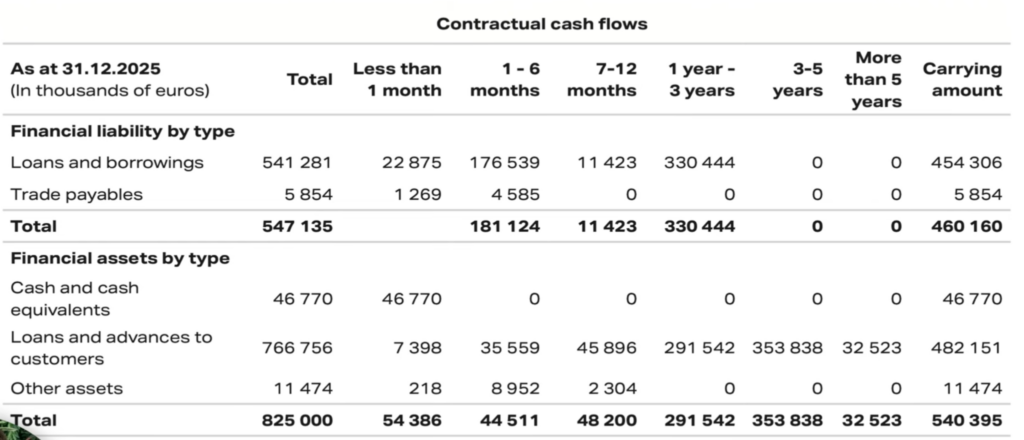

The Creditstar Group’s annual financial statements clearly show the cash flow the company expects to generate from its liabilities and assets over the coming months. The figure below shows the breakdown.

Over the 1–6-month period, liabilities of €181 million are due. At the same time, the company receives only €44 million in assets.

For many investors, this raises alarm bells, as it would appear that Creditstar is unable to meet its liabilities – though this is only partly true. What Creditstar is doing here is known as maturity transformation.

Good to know:

In the case of Creditstar, maturity transformation means that the company uses investor funds that are available at short notice (e.g. via Monefit SmartSaver with flexible payouts) to finance longer-term consumer loans.

Furthermore, the total assets of €540 million, compared with total liabilities of €460 million, show that Creditstar remains on a solid footing as long as investors continue to trust the company and reinvest their money.

In times of genuine crisis, either flawless liquidity management or an increase in interest rates is required to continue attracting investors and their capital. In the long term, this could pose a challenge for Creditstar.

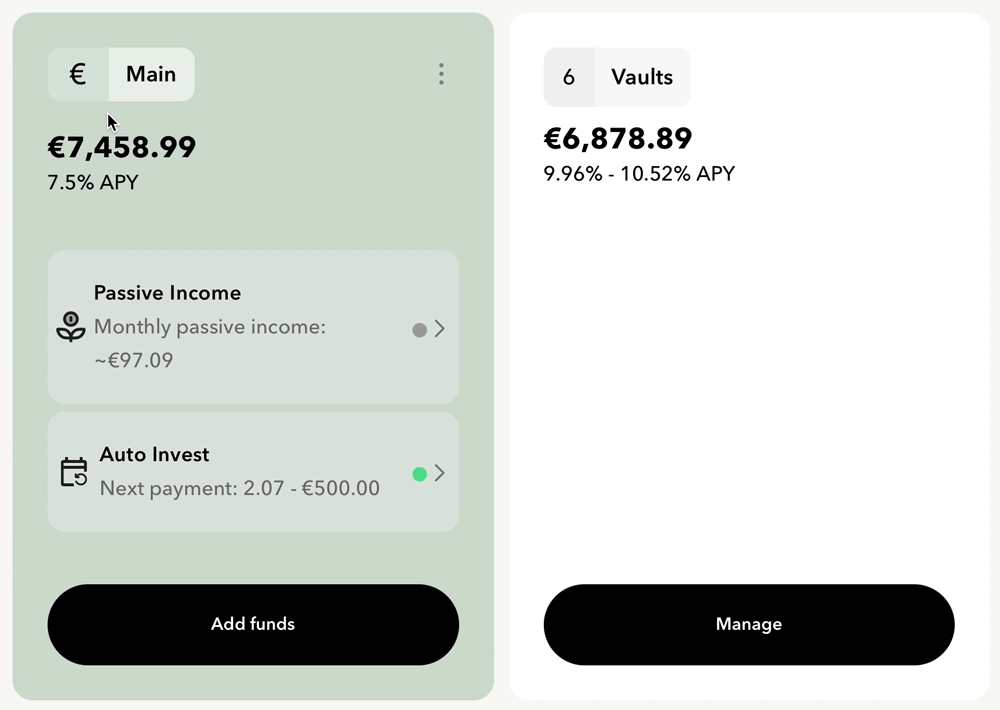

My Monefit SmartSaver experience: How my €14,000 portfolio is performing

My assets with Monefit currently amount to just over €14,300. This puts me just below the average of €15,900 that investors have invested on the platform.

I’ve invested just over half of this in the standard SmartSaver, where my money is available daily and which earns me around 7.5% interest. The other half is tied up in my Vaults, through which I earn around 10%

Between January and June 2026, I have already earned €621 in interest on Monefit, broken down as follows:

| Month | Interests |

| January | 107,80 € |

| February | 104,32 € |

| March | 111,44 € |

| April | 102,86 € |

| May | 96,74 € |

| June | 97,97 € |

| Total | 621,13 € |

For my investments with Monefit, I use the Auto-Invest feature, which invests on my behalf every month. At the moment, this amounts to €500 each month. As the Creditstar Group has made me feel so positive with the latest figures from its annual accounts, I invested an additional €500 in June.

Based on my experience with Monefit so far and the latest financial results, I’m continuing to use Monefit as an interesting addition to my portfolio.

Conclusion: Hard financial figures reflect Monefit’s success

Although Monefit is still a relatively young platform, it has proven itself to be a strong player in the P2P market in recent years. In particular, the audited annual accounts of the parent company, Creditstar Group, demonstrate the operational success of its core business: an interest margin of 14.4 per cent and a declining proportion of overdue loans.

Alongside its substantial cash buffer and the record profit achieved in 2025, Creditstar is also reporting record levels of debt. This high level of debt enables the company to achieve strong growth and higher returns, but at the same time increases its dependence on functioning capital markets and stable investor confidence.

The performance over recent years points to a growing and profitable company. At the same time, investors should continue to monitor the high level of debt and the reliance on external capital. In any case, I’m staying invested in Monefit and will continue to make my monthly investments, thereby earning interest of around €100 every month.

Take a look at my platform comparison Monefit vs. Bondora if you’d like to find out more about Monefit and an exciting alternative to it.

FAQ – Frequently asked questions about Monefit SmartSaver