Monefit vs. Bondora: Which platform is right for you?

Investors on Go & Grow receive 6% interest, whilst Monefit promises its investors 7.5%. But is the new Go & Grow – following Bondora’s recent rebranding – still of interest to investors, or is Monefit currently the more attractive option? In today’s post, we’ll take a detailed look at both platforms and explain when each one is the best choice for you as an investor.

In brief:

- Both Monefit and Bondora are similar in essence, but differ primarily in terms of interest rates and how they develop.

- Monefit investors currently receive 7.5% interest, whereas Go & Grow offers just 6% – and there is a likelihood that this will fall further soon.

- Monefit’s track record shows that, despite having been in existence for only a short time, the platform has developed very positively and is committed to continuous improvement.

- Monefit is a good choice for investors looking for higher interest rates and more customisation options, whilst Go & Grow stands out primarily for its long track record.

Monefit vs. Bondora: How are the platforms performing at the moment?

With both Go & Grow and Monefit, your money is invested in consumer loans. With Go & Grow, these are loans from the Bondora Group, whilst with Monefit they are loans from Creditstar.

Both platforms invest exclusively in European markets such as Finland, the Netherlands or Estonia with Go & Grow, and the UK, Spain or Sweden with Monefit.

I have been involved with both Go & Grow and Monefit from the very beginning and have now invested a total of more than €23,000.

My investment of just under €11,300 on Go & Grow earns me €1.64 in interest every day. Back in 2018, Bondora was still paying its investors 6.75%, but both the interest rates and the deposit limits have changed continuously.

Both Go & Grow (formerly Bondora Go & Grow) and Monefit currently offer investors the opportunity to earn attractive interest rates of 6% and 7.5% per annum respectively.

At the same time, you can withdraw your money quickly from both platforms – however, there are significant differences regarding the withdrawal limits, which we will discuss in more detail later.

The table below, however, gives you an initial overview of the key differences between the two platforms.

| Criterion | Bondora (Go & Grow) | Monefit (SmartSaver) |

| Launch of the platform | 2008 (Bondora) | 2023 (SmartSaver) |

| Company | Bondora AS | Creditstar Group |

| Loan type | Consumer credit (EU) | Consumer loans (Creditstar) |

| Investors | 511.513 | 35.000 |

| Target audience | Beginners & passive investors | Investors seeking returns who want flexibility |

| Yield (current) | ca. 6 % p.a. | ca. 7,5–10,5 % p.a. |

| Interest credited | daily | daily |

| Liquidity | at any time (in theory, immediately) | up to €1,000 immediately, the remainder in around 10 days |

| Minimum investment | from 1 € | from 10 € |

| Fees | None (€1 payout) | no fees |

| Special features | extremely simple, long history, high stability | higher returns, term deposits, bonus schemes |

Comparison 1: Monefit vs. Bondora – The Return

However, as mentioned above, the advantage Monefit has over Go & Grow is the higher interest rate.

At 1.5% more, this is significantly more attractive than Go & Grow. That might not sound like much at first glance, but it certainly is, especially if you’re investing slightly larger sums and want to grow your money.

The coronavirus pandemic led to fluctuating deposit limits at Go & Grow. Initially, investors could invest up to €400 per month via the platform, then this increased to €1,000. For investors wishing to deposit more than this, the interest rate was reduced to 4%.

In April 2025, this system was finally abolished and, at the same time, the interest rate fell from 6.75% to 6%. This interest rate remains in place to this day.

At Monefit, the interest rate was slightly higher from the outset, at a minimum of 7.25%, and those who invested more could earn even more. However, this model has been adapted to benefit investors, meaning that every investor now receives 7.5% interest.

Monefit’s interest rate of 7.5% remains unchanged to this day. However, I am very curious to see whether it will stay at this level in 2026, as current inflation in the US, Europe and around the world is rising, driven primarily by geopolitical tensions such as the war in Iran.

I therefore expect the European Central Bank to raise the base rate this year, potentially heralding the next shift in interest rates.

It remains to be seen whether and how Monefit and Go & Grow will pass on the higher interest rates to investors.

Comparison 2: Monefit vs. Bondora – Liquidity

Monefit is the right choice for you if you don’t need immediate access to your investment and would rather let your money work for you in the medium to long term. Especially if you don’t rely on constant liquidity in your day-to-day life, this model can certainly be worthwhile for you and offers more attractive interest rates in return.

This is because: An immediate withdrawal of up to €1,000 per month is possible via SmartSaver. These smaller amounts are therefore immediately available to you, which is already sufficient for many investors.

However, as soon as you wish to withdraw larger amounts, you will need to be patient. Any transfer over €1,000 can still take up to 10 working days. For me, this is the biggest drawback compared to Go & Grow, where the entire amount lands in your account within seconds.

This limited liquidity means that Monefit is less suitable as a short-term parking spot for your money, but should rather be used for long-term wealth accumulation.

So, if you’re willing to sacrifice maximum flexibility in exchange for a higher return, then Monefit is the better choice for your portfolio.

Comparison 3: Monefit vs. Bondora – The Features

For anyone who values a personalised platform, Monefit is the more attractive choice.

Monefit has responded to investors’ desire to increase their passive income and has introduced this feature for its SmartSaver. Interest is transferred to the current account on a monthly basis.

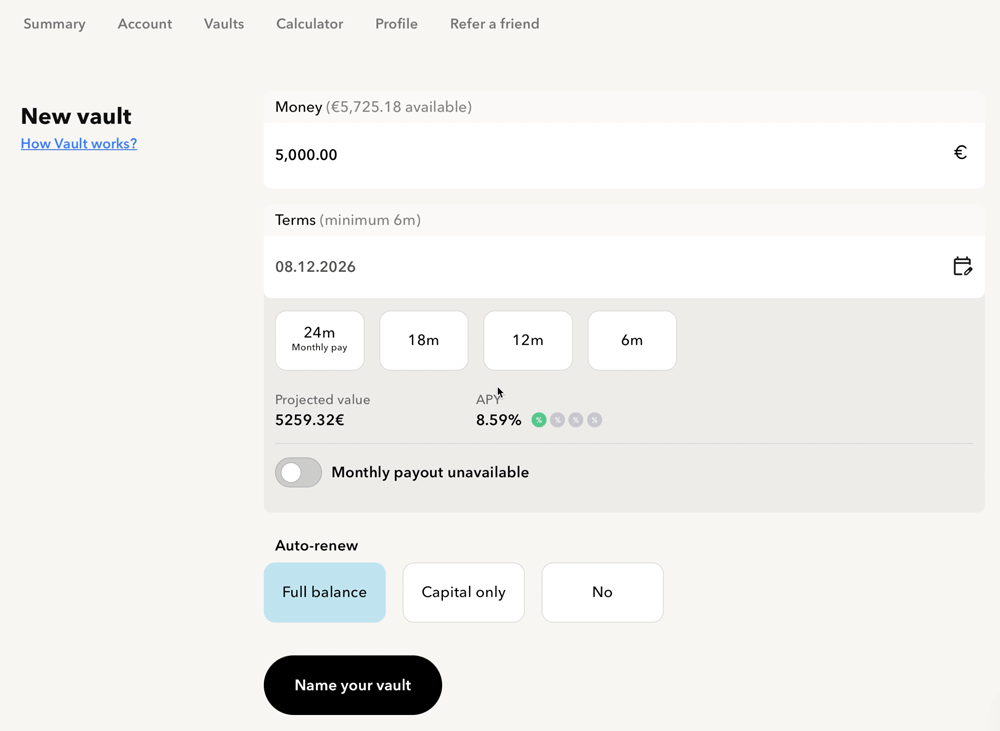

This feature may be of particular interest to investors who, like me, use various vaults, i.e. fixed-income products.

In addition, you can specify the date on which you would like to receive the money – and the further into the future the payout is, the higher the interest rate will be.

In practical terms, this means that investors: who invest their capital via the Vault feature for a term of 24 months can earn up to 10.5% interest per year.

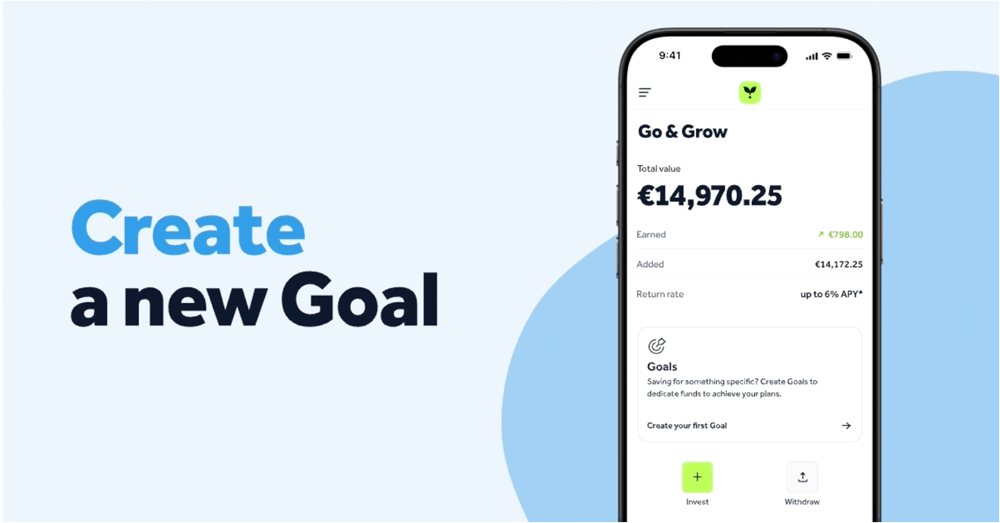

Bondora, or rather Go & Grow, has seen somewhat less development in terms of its features in recent years, but has nevertheless recently announced an exciting new feature: the Goals feature.

With the Goals feature, investors can better organise their money and build it up in a targeted way. Specifically, it allows users to set savings goals, name them individually and track their progress at any time.

The balance continues to earn the maximum return of 6% per year, regardless of how many goals are set.

Outlook: How do the platforms finance themselves now and in the future?

In February of this year, Bondora’s lending volume was lower than new investments from investors. This was also the case in March. An initial trend is therefore emerging here, suggesting that Bondora currently has too much cash on hand.

Furthermore, Bondora is currently in the process of obtaining a banking licence. If successful, Bondora will be able to refinance at significantly lower costs in future than before, meaning that the returns and interest rates for Go & Grow investors are highly likely to fall thereafter. At least, that is my assessment.

The Creditstar Group, and therefore also its financing platform Monefit, are not currently on the path to becoming a bank. This means the platform will have to continue paying its investors higher interest rates to remain attractive.

So whilst Bondora, through its pursuit of a banking licence, is moving towards an environment of lower refinancing costs, Monefit must remain rather aggressive in the current interest rate environment and continue to offer higher returns and interest rates in order to attract capital in the future. This naturally plays into the hands of yield seekers like us.

Another key difference between Monefit and Bondora is the fact that Monefit’s parent company, Creditstar, raises funds through bonds. These are traded on the NASDAQ Baltic, as shown in the figure below. Bondora, on the other hand, still primarily funds itself through its own Go & Grow platform

Creditstar raised €46 million through its bonds last year. This includes funding sources such as the private lending platform Kilde from Singapore. However, I reckon that Monefit, with its 7.5% interest rate, is the cheapest source of funding.

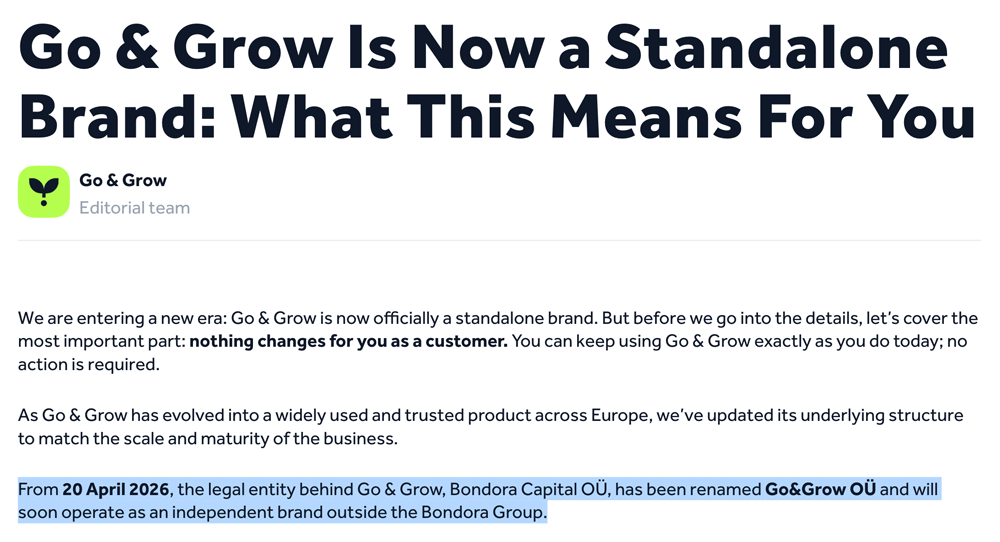

What is really behind Bondora’s rebranding?

Bondora recently underwent a rebranding and turned Go & Grow into a standalone brand.

At first glance, the changes for investors aren’t particularly significant – the way things work has largely remained the same – but in my opinion, this strategic move has deeper motivations that aren’t being discussed yet.

It should already be clear to investors that funding from Go & Grow investors is to be clearly separated from the rest of Bondora’s loan portfolio, as well as from a potential banking licence. Bondora is drawing a clear line here, separating the two divisions even more sharply than was previously the case.

We will now look in detail at whether an investment on Bondora remains attractive to you as an investor following this measure, or whether Monefit is now the better choice.

Is Monefit the better Bondora alternative?

For me, Monefit is currently the better Bondora alternative. I will continue to invest new funds in Monefit, as I have done previously. Go & Grow certainly has its advantages, particularly when it comes to payouts, but for me, Monefit has caught up significantly in recent years.

For this reason, alongside my share savings plan, I also have my €500 savings plan with Monefit running, which is executed on the 2nd of every month.

As soon as Go & Grow shows any signs that interest rates are set to fall in the future, I will certainly withdraw the bulk of my investment.

I don’t know exactly how much that will be, as it naturally always depends on the interest rate, but 6% is, to be honest, already the lower limit for me when it comes to the risk involved in consumer loans.

Because even if Bondora were to obtain a banking licence, there would most likely be no deposit protection for Go & Grow investments.

If there were, I’d be happy to correct my statement, but 6% AND deposit protection – we haven’t seen that anywhere yet.

Who shouldn’t bother with Monefit?

It’s easy to summarise which investors wouldn’t benefit from switching from Go & Grow to Monefit. If your focus is more on S security than on returns, Go & Grow is probably the better option for you.

Added to this is the age of the two platforms. Bondora was founded back in 2008 and can therefore draw on a long history and a wealth of experience.

Consequently, the platform has also weathered crises such as the coronavirus pandemic well, which was not the case for other platforms. Monefit, on the other hand, was only founded in 2023 and is therefore comparatively young.

| Criterion | Monefit (Credistar) | Go & Grow |

| The 2020 coronavirus crisis | Repayments have largely been met, though some have been delayed | Interest income remains stable, with payments usually made within a few days |

| Crisis management | Flexible adjustments to risk and lending | Tried-and-tested systems, with hardly any restrictions |

| Experience | Benefited from a strong group structure (Creditstar) | Proven in a crisis and reliable as early as 2008 |

| Reliability | Good, but dependent on Creditstar | Very high, thanks to broad diversification and experience with the system |

Nevertheless, it should be noted at this point that, over this period, Monefit has grown to a comparable size of loan portfolio and has presumably also achieved similar levels of profitability. However, this will become clearer once the forthcoming annual accounts are published.

Creditstar’s currently unaudited annual accounts show the following figures:

- €110.9 million in interest income

- €15.3 million in net profit

- €547.0 million in total assets

- Over 1.53 million registered users of credit products

Conclusion: Monefit can certainly be worthwhile for certain investors

I have been investing in Monefit and Go & Grow since the very beginning. I have had good experiences with both platforms, but my experience with Monefit has become increasingly positive over the years. This is mainly due to the significantly more attractive interest rates that investors receive here – Monefit offers 7.5% compared to just 6% on Go & Grow.

There is also a good chance that interest rates on Go & Grow will fall further in the near future. Furthermore, I am impressed by the individual features at Monefit. This shows that the platform is constantly working to improve its products, which pleases me as an investor. For those who need to access all their money in an emergency, Go & Grow is the better choice. Those who want to earn higher interest rates are better off with Monefit

You can find more exciting platforms in our P2P platform comparison.

FAQ – Frequently asked questions