Set up a share savings plan and invest automatically on a regular basis

Are you currently looking into personal finance and keen to start building your wealth and planning for your future? Whatever your goal – providing for your family, boosting returns or topping up your pension – a share savings plan offers one option. In this article, we’ll take a closer look at how shares work, who would benefit from a share savings plan, and what advantages and disadvantages it offers.

In brief:

- In this article, you’ll learn how shares work, the different types available, and the opportunities and risks associated with them

- Share savings plan vs. one-off investment: We’ll show you which type of investment can deliver a higher return

- You will learn which investors should set up a savings plan and what drawbacks you need to be aware of

What are stocks?

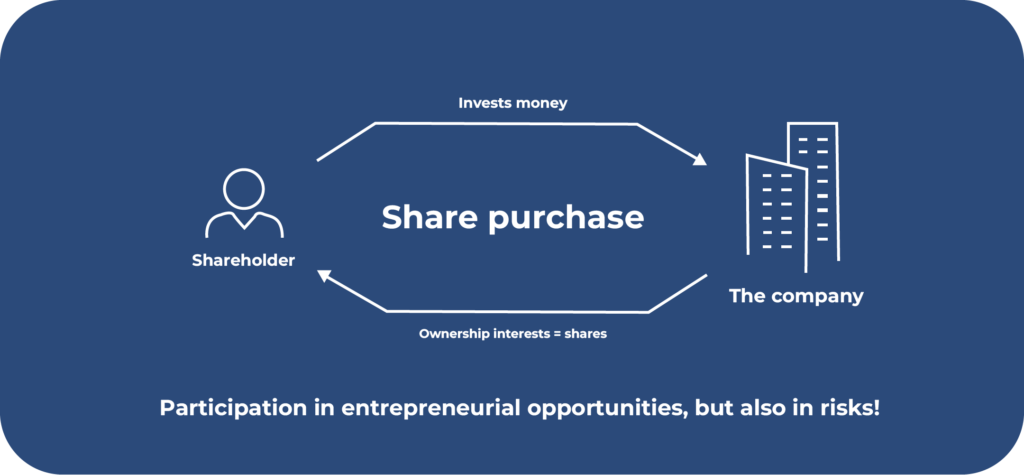

When you buy a share, you are providing capital to a company. In return, you receive the share and, with it, a stake in that company. Owning a share comes with certain rights. These include, for example, a say in the company’s affairs.

- Depending on the type of shares you hold, you can attend companies’ annual general meetings

- This is where important decisions for the future are discussed, such as how profits should be used

- In reality, it is usually only major shareholders who attend in order to exercise their right to have a say

- Private shareholders generally view their shares merely as an investment and are less interested in influencing company policy

There are various ways in which shareholders can benefit from their securities. They seek to make a profit through capital appreciation. In doing so, they buy company shares in the hope that they will perform well and increase in value over time, enabling the investor to sell them at a higher price.

Another option is a dividend strategy. Companies can pay out a portion of their profits to their investors in the form of dividends. Although companies are not obliged to do so, there are some that are known for their regular dividend payments. These are known as ‘dividend kings’.

What types of shares are there?

A basic distinction is made between registered shares and bearer shares. If a public limited company decides to issue registered shares, a share register is established.

- This section sets out which shareholders hold how many shares

- This gives companies a clearer picture of how the group is structured in terms of its shareholders

- It is important for investors to note that they can only attend general meetings if their name is on the register

Normally, shareholders do not need to take any further action to ensure that the previous owner’s name is removed and their own name is entered. This is handled by their custodian bank. A fee may apply in some cases.

In the case of bearer shares, it is not necessary to maintain a register. Anyone who currently holds a share in the company in question may exercise the associated rights. With this type of share, companies have only a vague overview of their shareholder structure.

A further distinction is made between preference shares and ordinary shares. Holding an ordinary share confers the right to attend the annual general meeting and to vote. Holders of preference shares do not have voting rights, but they do benefit from higher dividends.

Why invest in shares?

When it comes to the question “What is the best investment at the moment?”, company shares play an important role. They offer attractive opportunities and benefits for investors. In this section, we’ll look at the reasons why it can be worthwhile to invest in shares.

Offsetting inflation

The term ‘inflation’ refers to a general rise in prices. When wages remain the same but prices rise, purchasing power falls. For the same amount of money, consumers can afford fewer and fewer goods and services.

Inflation is measured using the Consumer Price Index, which is compiled by the Federal Statistical Office. This involves calculating, at regular intervals, the price of a hypothetical basket of goods comprising various goods and services. When compiling this basket, the Federal Statistical Office aims to ensure that it is representative of prices across Germany.

Over the long term, inflation can erode the value of your money in this way, which is why it is important to protect your assets. Traditional investment vehicles such as savings accounts offer too low a return. They are not enough to protect you from inflation. Shares offer attractive potential returns and can better safeguard your money.

Attractive opportunities for returns

Inflation also brings with it this advantage: if we look back over history, company shares have delivered the highest returns. The average return ranges between 7 and 9 per cent. It is therefore a high-yield investment that you can use to build up your wealth.

Investors use shares to benefit from capital appreciation, receive regular dividend payments or achieve financial freedom. It is particularly in this respect that shares differ significantly from the types of investment that were more commonly chosen in the past, such as building society savings plans or savings accounts. However, the potential for higher returns also comes with risks.

However, with the right knowledge and safety measures, you can mitigate this risk, even though a residual risk will always remain. Are you looking for an investment that combines attractive potential returns with greater security? If so, you might be interested in the topic of ‘shares or ETFs’.

Flexibility

If you’re looking for a flexible investment option, you might be interested in shares. They are traded on the stock exchange and can be bought and sold during normal trading hours.

- Other asset classes, such as fixed-term deposits, cannot be traded at any time and tie you into specific time periods

- Nevertheless, you should be aware that long-term investing allows you to reduce certain risks

- For example, with a long-term investment horizon, you can smooth out price fluctuations

Potential risks associated with trading in shares

If you’re interested in investing in shares, however, you should also consider the risks involved. We’ll take a closer look at these in this section so that you can get a better overview. Only by fully understanding the risks can you protect yourself against them.

Exchange rate fluctuations

Shares are traded on the stock market and are therefore subject to price fluctuations. Prices fluctuate constantly and can rise and fall rapidly. In the event of an economic crisis, shares can lose 50 per cent or even more of their value. A total loss is also possible should a company be forced to file for bankruptcy.

You should also ensure that your portfolio is sufficiently diversified. This is particularly important for beginners when it comes to investing. Invest in a variety of companies, sectors and countries so that your risk is spread across a wide range of securities.

Investing in a single share carries a degree of risk. If the share performs worse than expected, this can lead to significant losses. If, on the other hand, you invest in a large number of shares, losses on individual shares can be offset by gains on others. This diversification can protect your investment. Investors who invest in an ETF place particular emphasis on this approach.

Good to know:

Investors need to be prepared for such difficulties. You should therefore only invest money that you definitely won’t need in the near future, so that you aren’t forced to sell at unfavourable prices. Building up a nest egg can help here, providing you with a financial buffer to protect you during difficult economic times.

Planning difficulties and uncertainty

If, for example, you invest in fixed-income products, it’s easy to plan your finances. You know exactly how much money you’ll get back. That’s not the case with shares.

Prices are constantly changing, so you can’t say exactly how much return you’ll make. Because of price fluctuations, you also don’t have a specific exit point. Instead, you should take current prices into account and only sell when the price is right.

This uncertainty also applies if you are following a dividend strategy. Whilst there are some companies known for paying out dividends regularly, the amount of these payments does vary. This creates uncertainty when it comes to planning your finances.

Sufficient knowledge is required

If you want to trade shares, you’ll need a fair bit of knowledge. There are numerous different strategies and terms you should familiarise yourself with before you start investing. As diversification is only partial in this case, it’s particularly important to consider which shares you want to invest in.

It takes time to get to grips with these things and learn the basics. Once you’ve done that, you should develop your own strategy – for example, how to build up a share-based pension. You should also find out more about the companies in question so that you know exactly which ones you’re investing your money in.

If you want to invest, you don’t necessarily need to start with a large sum. Instead, you could opt to set up a savings plan. In this section, we’ll take a closer look at exactly how this works and who might benefit from a savings plan.

How does a share savings plan work?

Instead of investing a large sum of money all at once, investors can invest smaller amounts regularly over a set period of time. This can be done, for example, on a monthly, quarterly or half-yearly basis.

You will need a securities account for this:

- Investors can choose shares and set up a savings plan

- The investor then selects the time periods during which the money is to be debited

- In addition, they can choose a specific amount

- The savings plan will then run automatically

- This is how wealth is built up in small, steady steps

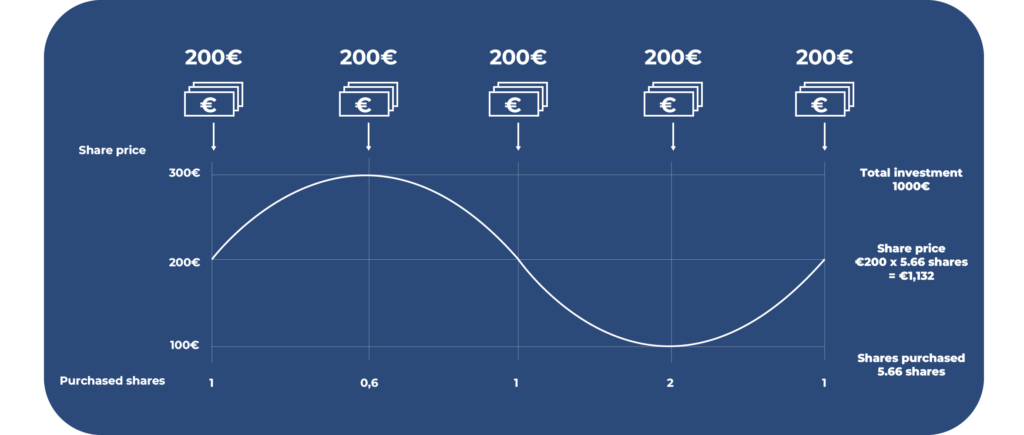

As share prices fluctuate constantly, you’ll buy your shares at different prices. Sometimes they’ll be cheaper, sometimes more expensive. Overall, this brings you closer to an average price – a phenomenon known as the cost-averaging effect.

As a fixed amount is invested and prices are constantly changing, investors with a savings plan do not buy whole shares, but only fractions of shares. This is a useful way of buying an expensive share in small increments.

Share savings plan vs. one-off investment

You might be wondering which is the better option: buying shares now and investing everything at once, or setting up a savings plan? Both can be worthwhile and depend on your current financial situation.

If, for example, an investor receives a large sum as a gift or has already built up a substantial nest egg, it may well be worth making a single investment. In this way, the entire sum can start working for the investor and generating interest. By taking this approach, it is possible to achieve a higher return in the long run.

However, there is also a downside: if you decide to make a single investment, the timing of your entry is crucial. You should aim to buy at the lowest possible price so as not to reduce your future returns.

If you don’t have any money to hand just yet, that’s no problem either:

- In such cases, a savings plan is a good idea

- Most providers allow you to set up a savings plan starting from as little as one euro a month

- So you don’t need a fortune to start investing

- Instead, you can easily adjust your savings plan to suit your circumstances

Unlike with a one-off investment, the timing of your entry is irrelevant here. You have little control over this anyway, as your custodian bank automatically debits the amount you have specified at set intervals. You are effectively averaging the price.

Good to know:

A share savings plan is a good option if you don’t yet have a large amount of capital and want to build your wealth gradually. If you already have a larger sum, a one-off investment is a good choice, as it allows your money to start working for you straight away and generate returns.

Share Savings Plan – The pros and cons you should be aware of

One of the key advantages of a share savings plan is that you don’t have to worry about finding the right time to buy. This can be difficult to pinpoint, as share prices are constantly fluctuating. Buying at the wrong time can certainly have a negative impact on your future returns.

This risk does not exist thanks to the cost-averaging effect. You buy your shares at a wide range of prices, which brings you closer to an average price. You therefore don’t need to worry about finding the right time to buy.

What’s more, a savings plan doesn’t take much time to set up. Once it’s in place, your savings plan runs completely automatically. Your bank deducts the amount you’ve specified and invests it automatically. Once it’s set up, you don’t have to worry about a thing and you don’t have to invest the amount yourself every month, which would be time-consuming.

What’s more, you mustn’t forget about or lose sight of building your wealth. You invest a one-off amount of time and get to grips with the details; after that, everything runs automatically and you can build your wealth in small steps without having to think about it regularly.

The high level of flexibility offered by savings plans is also particularly popular. If your financial situation changes unexpectedly, you can adjust your savings plan at any time. Do you have some extra money to spare? Then you can easily increase your monthly savings amount. If you need to reduce or pause your monthly savings, that’s easy to do.

But what are the drawbacks of a share savings plan?

- Lower returns: If you already have a larger sum available, it’s worth investing it all at once. That way, you can generate higher returns. Savings plans are only worthwhile if you can’t yet invest a larger sum, as otherwise you would achieve lower returns.

- Limited options for direct debits: You only have a limited choice of dates on which your bank can deduct and invest the amount. This is usually possible on a monthly, quarterly or half-yearly basis. You can often choose specific dates as well, such as the first day of the month. However, these options are limited and depend on your bank.

- Not available for every share: You cannot invest in every share via a savings plan. Some only allow you to buy whole shares, not fractional shares. This means the choice of shares is limited.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

When you buy a share, you acquire a stake in a company. You can benefit from increases in value or dividends, and you are granted certain rights, such as the right to attend and vote at a company’s annual general meeting.

Shares are an exciting investment and offer many advantages, such as the potential to hedge against inflation, attractive returns and a high degree of flexibility. On the other hand, you need to be prepared for the following drawbacks: price fluctuations, the time required to build up your knowledge, and the difficulty of planning due to uncertainties.

You can buy shares through a savings plan and receive units. Alternatively, you can make a one-off investment. A savings plan is particularly worthwhile if you don’t yet have a large sum to invest. In this case, the timing of your first investment doesn’t matter. You can also benefit from the cost-averaging effect and it requires very little time.

A single investment is worthwhile if you’ve already saved up a substantial amount. This way, you can achieve higher returns, as your money starts earning interest sooner. Good luck with your share investment! You might also be interested in the topics “Scalable Capital vs Trade Republic”, “Broker Comparison” or “P2P Lending Comparison”? Find out more here.

FAQ – Frequently asked questions about share savings plans