Northern Finance P2P lending comparison: the best providers for 2026

Peer-to-peer lending is becoming increasingly popular – no wonder, given the high returns! But there are big differences between the individual platforms. For six years now, the Northern Finance P2P lending comparison has been helping you find the best deals and avoid dubious providers.

In brief:

- The individual P2P lending providers have different focuses and target different investment strategies.

- The first four places are impressive across the board. From fifth place onwards, however, the quality declines sharply.

- The winner and runner-up are two well-known platforms. However, there are a few surprises further down the list!

What are P2P lending plattforms and why is it worth comparing them?

Banks lend money to their customers and earn interest. With peer-to-peer lending, or P2P for short, you too can do this! To do so, you join forces with other investors and jointly finance lending for other individuals or companies.

And it’s worth it:

- You can earn very high interest rates. An average return of 15, 16 or even 17% is entirely possible

- The entire process is very simple, as the P2P platforms take care of the processing.

- Since several people finance a loan, it is possible to get started with small amounts.

This also allows you to achieve good diversification: your money is spread across several lending.

P2P lending have many advantages over traditional investment products. With their high flexibility, some platforms are ideal as an alternative to overnight money. Other offers provide such high returns that they even make the best ETFs or the typical 70-30 portfolio look outdated.

But of course, such results do not come out of nowhere: you have to accept a fundamental risk. Repayments can be delayed or, in extreme cases, an entire P2P platform can fail! However, in my opinion, the high interest rates are absolutely worth these risks.

I had my first experience with P2P lending over 10 years ago and have since received thousands of euros in interest. This regular income is an important pillar of my portfolio, which has grown to over €400,000 as a result!

The Northern Finance P2P lending comparison works according to these criteria

The Northern Finance P2P lending comparison is entering its sixth round: I have been independently analysing and evaluating the most important platforms since 2020. The ranking is updated several times a year so that you always have the latest information.

What sets this comparison apart is that I invest large amounts with the individual providers myself and evaluate them from an investor’s perspective. No dry financial jargon, but a focus on the really important aspects!

To do this, I use eight categories that provide excellent insight into opportunities and risks:

| Category | Ideal value | Maximum points |

| Age | Over 5 years | 5 |

| Investors | More than 50,000 | 5 |

| Audited Annual Report | Available | 10 |

| Profitability | Achieved profit | 10 |

| Regulation | Platform and lender regulated by supervisory authorities | 10 |

| Features | Secondary market, auto-invest, German interface, tax report available | 20 |

| Ability to pay | Full solvency and no defaults | 20 |

| Growth | Growth intact after the crisis and good current developments | 20 |

A perfect P2P platform could achieve a maximum of 100 points. All ratings are based on real, verifiable data and my personal experiences. You can find out more about my invested amounts and results to date in my review, which I have linked to each platform for you.

Northern Finance P2P Lending Comparison: The Top 10 for 2026

The following list provides a brief introduction and rating of each P2P lending provider. The actual ranking follows at the end of this article.

Good to know:

The following valuation is a personal opinion and not investment advice.

Debitum Investments

We start with an old acquaintance: Debitum Investments has been included in the Northern Finance P2P comparison for many years and has always achieved very good results. It will still be worth investing in 2026.

The platform offers you the opportunity to invest in business loans and receive 11 to 15% interest. For the evaluation, we assume an average value of 13%. Granting loans to companies is an exciting addition to broaden a portfolio.

Despite its many advantages, relatively few investors have used Debitum Investments so far. This results in a point deduction, as does the fact that there is still no secondary market for the early sale of investments. In all other categories, however, the platform achieves full marks.

The overall result is extremely strong: 93 out of a possible 100 points! This means that Debitum Investments, as usual, occupies one of the top spots in the Northern Finance P2P lending comparison!

I have invested over €7,000 with Debitum Investments. You can find out how I have invested my capital there in my Debitum review.

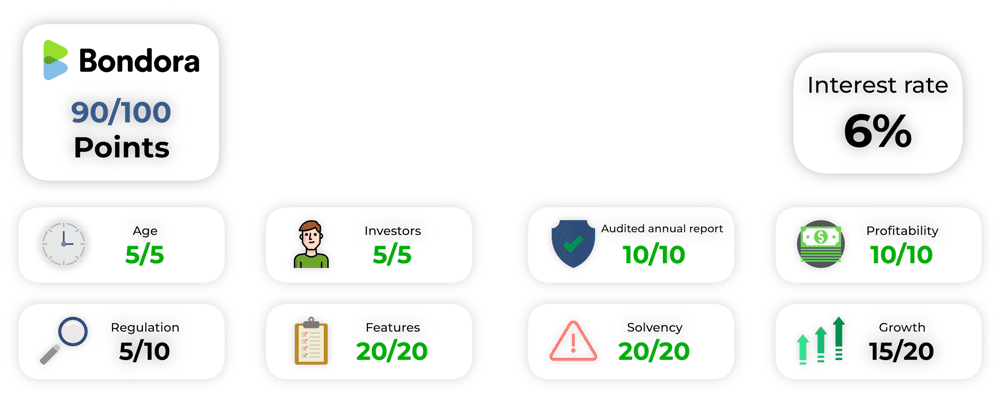

Bondora

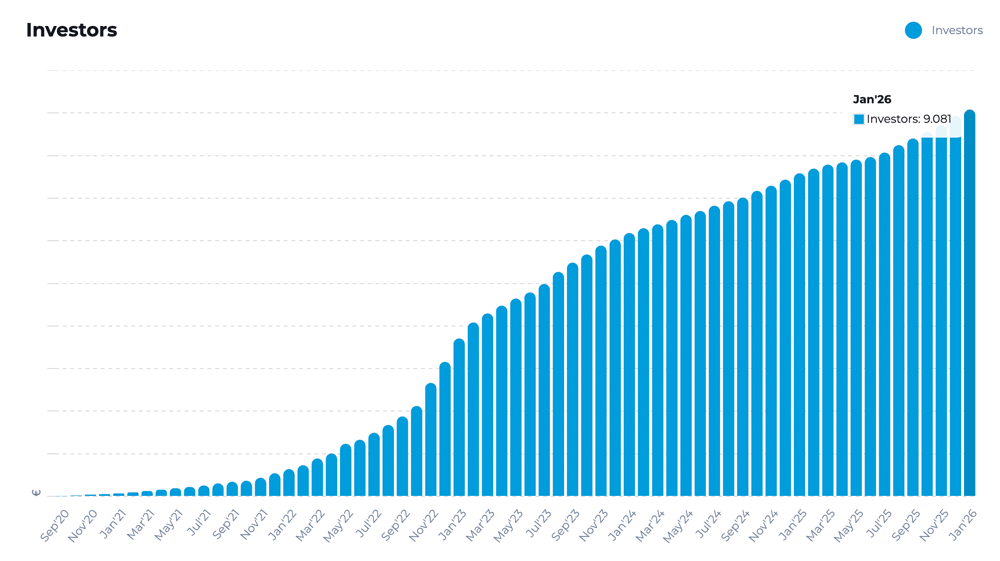

Bondora is not only the oldest European P2P platform (founded in 2008), but also one of the largest, with over half a million users. The reason for its great success is likely to be its unusual concept: you don’t invest in individual loans here, but in the company’s entire lending portfolio.

At 6% per annum, the interest rates are rather low compared to other P2P lending, but you can access your money at any time and have it paid out. In addition, interest is credited daily, which ensures a strong compounding effect.

All this works with just one click – investing couldn’t be easier! That’s why Bondora receives a near-perfect rating across the board. Exception: A small deduction in terms of regulation (the platform itself is not regulated, but the loan originator is) and growth.

This is because the company has lowered the interest rates that investors receive here, despite good business figures. Instead of the previous 6.75%, the rate is now only 6%. It remains to be seen how the return will develop in the future. Until then, however, a very good 90 points!

My own investment has experienced ups and downs in recent years, as I have repeatedly withdrawn and deposited money. Currently, my account here is worth around €7,500. You can find out more about the platform in my Bondora review.

Monetfit Smartsaver

With its Smartsaver, Monefit pursues a similar concept to Bondora: you don’t invest in individual loans, but in an entire loan portfolio. This means you can withdraw up to €1,000 per month at any time and receive daily interest on your capital. The interest rate is a respectable 7.5% per annum.

Although this is less than many other platforms in the Northern Finance P2P lending comparison, the quick accessibility and cool features such as a savings plan make the offer very attractive nonetheless!

Word has spread: Monefit has experienced extreme growth and is now a very popular alternative to instant access savings accounts! I have also invested over €15,000. Just under €5,000 is in ‘Vaults’, where interest rates of up to 10.5% are possible, but your capital is also tied up for some time.

Monefit loses a few points in some areas. The platform is still quite young and, with ‘only’ 30,000 investors, rather small. In addition, only the credit companies are regulated by supervisory authorities, not the platform itself. Nevertheless, it still manages to score a very strong 86 points!

You can see how I personally invest my capital and how worthwhile it is in my Monefit review.

Mintos

Back to a particularly large platform: no provider in the P2P lending comparison can compete with Mintos and its over 600,000 investors in terms of size! In addition to traditional lending, you can now also invest in bonds, ETFs and real estate companies. The average return is very attractive at around 11%.

Bonds are particularly interesting for many investors: even a high-quality broker such as Freedom24 only allows you to invest €1,000 or more per bond. With Mintos, on the other hand, you can start with as little as €50! This is a clear advantage for the P2P platform.

As you would expect from the market leader, the overall impression is good; the provider only loses points in terms of profitability. Due to heavy investment, it recorded a bitter loss of €2.7 million in 2024. There is also room for improvement in terms of solvency and growth.

Nevertheless, the result is very good at 80 out of 100 points!

Mintos has also been part of my P2P portfolio for over 9 years. During this time, I have received over €1,100 in interest. You can find out what my current investment looks like and how it will develop in my Mintos experience.

Lande

Lande is an old acquaintance in the P2P lending comparison. Since 2020, you have been able to make your money available to farmers. This is a good thing, for which you are rewarded with an average interest rate of 11%. Tangible assets such as machinery, livestock or land serve as collateral.

This sounds like a safe bet, but in practice it works rather moderately: defaults have continued to accumulate in recent months and recovery takes an extremely long time. Therefore, there is a significant deduction in solvency.

The low number of investors – and the associated weak growth – also does not make a good impression.

This makes Lande the biggest loser in the Northern Finance P2P lending comparison: it lost 15 points compared to the previous year and now only scores 66/100. This is not a good sign for an established platform.

You can find out how I personally deal with the increasing number of failures in my Lande review.

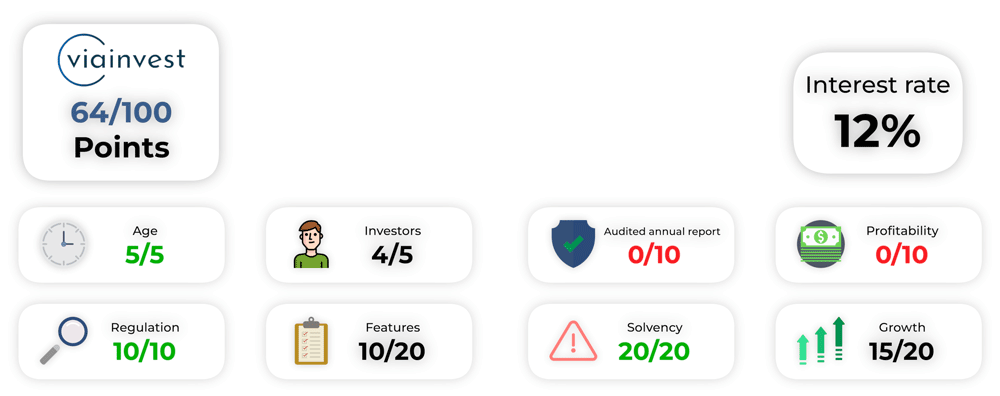

Viainvest

Although it has been in business for 10 years, Viainvest is one of the lesser-known platforms. So far, it has only attracted around 46,000 investors. This is surprising, as the provider reliably pays attractive interest rates averaging 12%!

Here, you invest in loans from the ViaSMS Group, which is active in Sweden, Czechia, Latvia and Romania. However, the fully regulated platform loses a lot of points due to the lack of annual financial statements: the ViaSMS Group (in whose loans we invest here) still owes us the 2024 annual report!

This causes Viainvest to drop 15 points in the Northern Finance P2P lending comparison, leaving it with a meagre 64 points. We can only hope that an annual report will be submitted soon so that the platform can return to its former glory!

With only around €2,500, Viainvest is a smaller position in my portfolio. Despite the lack of an annual report, I wouldn’t want to be without this provider: over the years, it has been a real anchor of stability and has earned me high interest rates! You can find out more about my success story in my Viainvest review.

EstateGuru

The Northern Finance P2P lending comparison helps you avoid bad and risky platforms. We have such a case with EstateGuru: the real estate loan provider has gone from being an excellent P2P service provider to an unreliable trap.

Some investors have been waiting for years for the repayment of defaulted lending. Those who finally get their money back quickly take flight. EstateGuru has lost more than 5,000 investors in this way over the last six months. In terms of solvency and growth, it therefore scores zero points.

Overall, EstateGuru scores a weak 60 out of 100 points. The interest rates offered, at around 9%, are also far too low to make the provider attractive. My recommendation is therefore: stay away!

Unfortunately, I still have over €5,000 invested with EstateGuru. However, if I get my money back, I will withdraw it and invest it on other platforms.

Due to the high level of loan defaults currently at EstateGuru, I am currently investing my capital in Viainvest (obtained with this link*). With Viainvest I earn over 13% interest, which is significantly more than with EstateGuru. As a welcome bonus, you will only receive 1% cashback on your investment after 90 days via this link.

Ventus Energy

With its very high interest rates and unusual concept, Ventus Energy has already caused a stir in the Northern Finance P2P comparison. It will be back again in 2026: here, you invest in energy projects such as power plants or solar installations. In return, you receive up to 17% interest, which can be even higher thanks to regular bonus promotions.

The very young platform (active since 2024) has attracted 5,000 users so far. Considering the very high minimum amount of €1,000 per lending, this is an impressive achievement!

Particularly noteworthy are the excellent transparency and reliable repayments. Unfortunately, the current annual report has not yet been published, so many points are lost here: it is therefore not possible to make any statements about profitability!

However, with 58 points, the result is still solid for such a young and specialised provider.

I myself have invested over €11,000 in Ventus Energy and earn €5.90 in interest every day! You can find out more about this highly lucrative investment in my Ventus Energy review.

Freeze on investments:

As early as May 13, 2026, Ventus Energy responded by announcing that, for “regulatory reasons,” new investments by individuals residing in Germany would no longer be possible for the time being.

Ventus Energy is currently undergoing restructuring and is not accepting new investors or investments. That's why I'm investing my new funds on Monefit. As a welcome gift, you'll receive a €5 bonus + 0.75% (for 90 days).

Devon

Devon is another new addition to Northern Finance’s P2P lending comparison: a company that creates affordable housing through modular buildings. It has been successful for 30 years and has been financed in the past through marketplaces such as EstateGuru.

Issuing its own P2P lending was a logical next step. The payment history is excellent (on other platforms), and growth has been enormous. With 15% interest, that’s no surprise!

As it is a very young provider with few users and no annual report available yet, it does not receive too many points. However, this is completely normal for new P2P platforms. I am definitely excited to see what Devon will achieve in the future! Currently, it only scores 52 out of 100 points.

Of course, I’ve invested in this myself! I currently have €2,700 in my Devon account. You can find out how I’ve got on with it and all the important details in my Devon review.

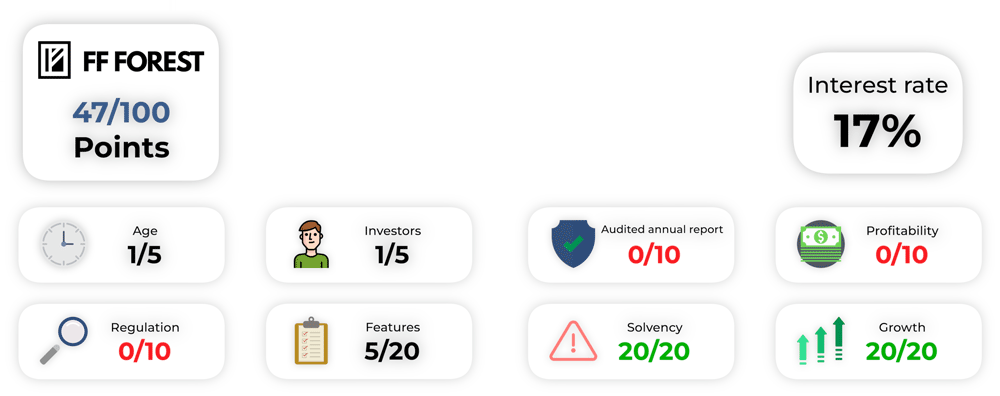

FF Forest

With FF Forest, we come to the first new addition to the P2P lending comparison. As is usual for young companies, the provider cannot yet score too many points due to a lack of users, age and annual reports. Nevertheless, I would like to mention this platform because it pursues a very exciting concept!

Here, you invest in forests. The company buys, leases and manages smaller forest areas, combines them into larger packages and then sells them on to large investors. With this very lucrative business, they can pay you interest of up to 18%!

This has always worked very well so far. As is usual with young providers, however, there is also a serious risk. For courageous investors, getting on board could be very worthwhile and future developments are likely to remain exciting. Currently, however, it is only enough for 47 points.

Although it is a new platform, I have already invested over €3,000. You can read about my experience with it in my FF Forest review.

Conclusion: Major changes in the comparison of P2P lending providers!

There are some changes in the Northern Finance P2P lending comparison for 2026! Here is a look at the scores:

| Age | Investors | Audited annual report | Profitability | Regulation | Feautures | Solvency | Growth | Interests | Total | |

| Debitum | 5 | 3 | 10 | 10 | 10 | 15 | 20 | 20 | 13 % | 93 |

| Bondora | 5 | 5 | 10 | 10 | 5 | 20 | 20 | 15 | 6 % | 90 |

| Monefit | 3 | 3 | 10 | 10 | 5 | 20 | 15 | 20 | 7,5 – 10,5 % | 86 |

| Mintos | 5 | 5 | 10 | 0 | 10 | 20 | 15 | 15 | 11 % | 80 |

| LANDE | 5 | 1 | 10 | 10 | 10 | 20 | 5 | 5 | 11 % | 66 |

| Viainvest | 5 | 4 | 0 | 0 | 10 | 10 | 20 | 15 | 12 % | 64 |

| Estateguru | 5 | 5 | 10 | 10 | 10 | 20 | 0 | 0 | 9 % | 60 |

| Ventus Energy | 2 | 1 | 0 | 0 | 5 | 10 | 20 | 20 | 17 % | 58 |

| Devon | 1 | 1 | 0 | 0 | 0 | 10 | 20 | 20 | 15 % | 52 |

| FF Forest | 1 | 1 | 0 | 0 | 0 | 5 | 20 | 20 | 17 % | 47 |

Debitum Investments has once again claimed victory. With an extremely strong 93 points, it is an almost perfect platform! However, the runner-up, Bondora, also performs very well with 90 points.

Monefit and Mintos are two other very attractive providers in the ranking. After that, however, there is a significant drop in quality: from fifth place (LANDE) onwards, the scores drop sharply.

These providers are not necessarily bad, but you should be aware of the potential disadvantages and assess the risk correctly. If you are unsure, you can confidently turn to the top 4 in the P2P comparison.

They are well suited for most types of investors and help you build passive income with P2P lending!

FAQ – Frequently asked questions about the P2P lending ranking