Living off dividends: My strategic path to financial freedom

The dream of letting one’s shares work for oneself and thereby being able to finance one’s livelihood is becoming increasingly important amongst the general public. Some investors even manage to live off dividends, whilst others lack a clear strategy for achieving this goal.

The good news is: you don’t need an inheritance or a lottery win to build up a substantial fortune. As long as you bear a few key points in mind when investing, you too can generate passive income.

In this article, we’ll show you which investment strategies are the right ones, how much capital you really need to achieve your financial goals, and how my personal portfolio is structured to achieve them.

In brief:

- Companies such as Coca-Cola, Procter & Gamble and Johnson & Johnson are known for their reliable dividend payments.

- Dividends are not guaranteed. Companies may reduce, suspend or completely cancel their dividends at any time.

- If you want to live off dividends, you should focus on high-quality shares and ETFs. However, don’t rely solely on the dividend yield.

- The amount of dividend income you need to live on depends on your lifestyle. To generate a monthly dividend income of €2,000, you would need assets worth €480,000, assuming a 5 per cent return.

Living off dividends: Why I let my money work for me

I realised the power of compound interest at a young age and decided to embark on my investment journey as soon as possible, so that one day I could live off my investment income.

It certainly wasn’t easy at the start, as it takes some time for the power of compound interest to really kick in, but the most important thing when investing is to stick with it – and that’s exactly what I’ve done.

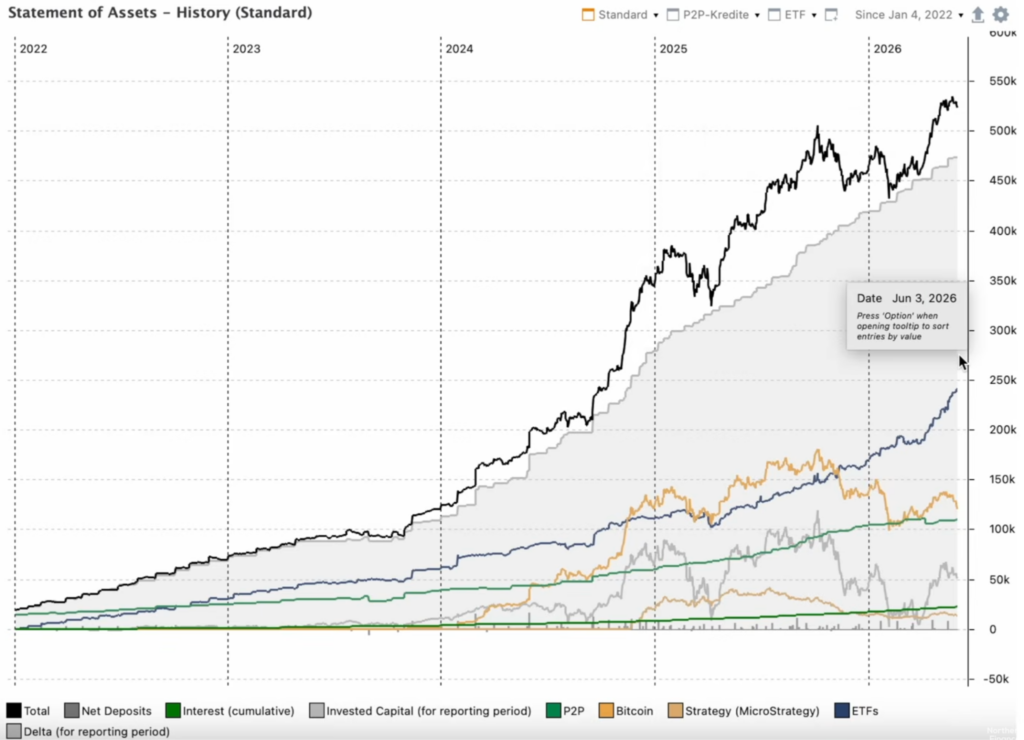

I’m now very proud of how my investments have performed. My portfolio has surpassed the half-million mark this year. So I’m making good progress towards my goal, which is: financial freedom by 2030.

As diversification is extremely important, my portfolio consists of various asset classes.

Alongside P2P loans, my investments in ETFs – which I have been investing in for many years – are among my largest holdings. The companies included in these ETFs have so far generated strong dividends, which I continuously reinvest to help my wealth grow more quickly.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Living off dividends: The best-known asset classes

Dividends are distributions of profits by listed companies. In Europe, the amount of the dividend is usually decided at the annual general meeting and paid out either annually, half-yearly or quarterly.

For many investors, dividends offer an attractive way of benefiting from regular passive income. However, it is also worth noting that dividend payments can fluctuate and are not always guaranteed.

That’s why, as well as shares, I also invest in P2P loans, where interest payments are more predictable. Take a look at my latest P2P lending ranking to find out more about the individual platforms.

The best-known asset classes for dividends include:

- Dividend-paying shares: Shares in these companies pay out a portion of their profits as dividends. Companies known for paying stable or rising dividends are particularly popular.

- Example: Coca-Cola, Procter & Gamble, PepsiCo

- Dividend ETFs: Here, rather than investing in individual shares, investors invest in funds comprising several high-dividend-paying companies. ETFs are particularly suitable for investors who wish to diversify their portfolio and invest in several dividend-paying shares with a single investment.

- Example: Vanguard FTSE All-World High Dividend Yield UCITS ETF

- REITs: Through Real Estate Investment Trusts (listed property companies), investors can invest in property such as office buildings, shopping centres or logistics parks without becoming owners or landlords themselves. REITs are required to pay out a large proportion of their profits as dividends, which is why they are a popular high-dividend option.

- Example: Realty Income, W. P. Carey, Prologis

Personally, I’m investing more and more in ETFs, but I regularly add individual shares to my portfolio with a view to improving my dividend yield.

At what point can you live off your dividends?

You’ve no doubt asked yourself this question before: “How many shares do I need to live off the dividends?”. There’s no one-size-fits-all answer to this question, as it depends on various factors:

- Personal lifestyle: The higher your standard of living, the higher your dividends need to be to maintain it. So work out for yourself what you need to live on, so that you can set clear investment goals.

- Available start-up capital: Whilst start-up capital is not the only or most important factor when investing, it certainly gives you a head start. The more capital you have at your disposal, the quicker you will generate significant returns.

- The quality of dividend-paying shares: Some shares are known for their reliable dividend payments, whilst others are more prone to fluctuations in their payouts. Choosing the right shares is therefore crucial if you want to live off dividends.

- Expected return: The higher the dividend yield, the quicker you’ll reach your goal. Bear in mind, however, that higher returns can also result from falls in share prices and often come with a higher level of risk. So think carefully in advance about your risk tolerance when investing.

In addition to these points, you can use the dividend calculation formula to work out how much capital you need to be able to live off dividends:

Capital required = desired annual income ÷ dividend yield

In the table below, we have provided some sample calculations to help guide you.

Please note that these are illustrative scenarios. Real-world market conditions are often subject to fluctuations and may therefore also result in fluctuating returns on investment.

| Monthly dividend income | 3 % return | 4% return | 5 % return | 6 % return |

| 500 € | 200.000 € | 150.000 € | 120.000 € | 100.000 € |

| 1.000 € | 400.000 € | 300.000 € | 240.000 € | 200.000 € |

| 1.500 € | 600.000 € | 450.000 € | 360.000 € | 300.000 € |

| 2.000 € | 800.000 € | 600.000 € | 480.000 € | 400.000 € |

| 3.000 € | 1.200.000 € | 900.000 € | 720.000 € | 600.000 € |

We have created a dividend calculator. With this interactive financial simulation, you can find out in just a few steps when you’ll be able to live off your dividends.

Enter either your current capital or your desired dividends. The calculator will then show you your passive income or how much capital you need to achieve your financial goals.

Living off interest calculator

Calculate income from capital or the required assets

💰 Capital → Income

Monthly: –

Annually: –

🎯 Income → Capital

Capital required: –

Good to know:

This calculator is for guidance only. Actual dividends may differ from the calculated figures due to dividend cuts, tax liabilities, currency fluctuations or changes in the dividend yield.

Living off dividends: achieving financial freedom with ETFs

When it comes to passive investing, ETFs have become one of the most popular asset classes in recent years. For beginners in particular, they offer a simple way to invest regularly and without hassle.

If you’re already investing in ETFs, you’ve already taken the first important step towards financial freedom. It’s important that you stay disciplined now, even if the amounts are a bit smaller or fluctuate.

Savings plans such as those offered by Freedom24 can help you make your monthly investments automatically. Make sure you claim the Freedom24 bonus to get more out of your investment.

Good to know:

With an ETF portfolio worth €50,000, you’re already in the top 10 per cent of the German population.

Below, we’ll take a look at the seven stages of building wealth with ETFs – from newcomer to ‘Fat FIRE’ millionaire. This will help you quickly work out just how wealthy you already are and when you’ll be able to live off your dividends.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Stage 1: The starting signal

- Every beginning is difficult, but once you’ve invested your first €10,000 in ETFs, I reckon you’ve already got off to a successful start.

- With this amount, the return does not yet contribute significantly to your wealth. Applying the 4 per cent rule, you’ll earn just €400 a year, or €33 a month. The biggest factor at this stage is your savings rate, so try to keep it as high as possible.

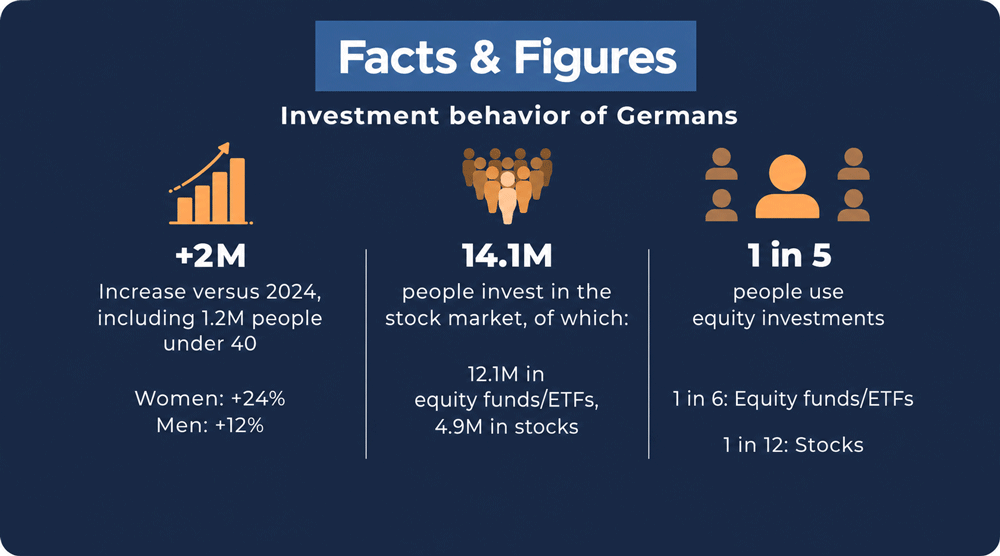

- Even if you’re just starting out with €10,000, you’re already ahead of 83 per cent of the German population. That’s because only one in six Germans invests their money in equity funds or ETFs.

- If you have invested between €10,000 and €40,000 in ETFs, you are already in the top 10 per cent, as figures from UBS and the German Equity Institute show.

Stage 2: First Freedom

- If your assets are between €50,000 and €100,000, you’re already enjoying a certain degree of freedom. That’s because this amount means you don’t have to go along with everything and can already shape your life much more in line with your own ideas.

- The dividends you receive within this income bracket range from €145 to €267 per month. This also means you are already among the top 6 per cent of the German population.

- Having this financial security also gives you greater peace of mind and stability in your day-to-day life, as unexpected events such as losing your job will no longer hit you as hard as they used to.

Stage 3: Coast FIRE

- Things really start to get exciting from Level 3 onwards! By this stage, you’ll have already built up an impressive ETF portfolio worth between €150,000 and €300,000.

Good to know:

Coast FIRE refers to the point at which the wealth you have already accumulated is sufficient to grow to your target amount by the time you retire – solely through returns and the power of compound interest. From that point onwards, you no longer need to invest any additional money to build up your wealth; you simply need to cover your day-to-day living costs.

- Suppose you have built up assets of €225,000 by the age of 40; with a return of 7 per cent, you would have a total of €888,000 at your disposal by the time you retire at 67 – without having to pay in a single cent more.

- At this level, you are already among the top 2.5 per cent of the total population.

Level 4: Barista FIRE

- As the name suggests, at this stage you no longer need to work full-time, but can take on a more relaxed part-time job with fewer hours – for example, as a barista in a café.

- The required ETF portfolio at this level is between €400,000 and €600,000, which will generate monthly dividends of more than €1,000 after tax.

- Only 1 per cent of the total population settle at this level.

Stage 5: Lean FIRE

- From this point onwards, it’s possible to completely leave the traditional 9-to-5 job behind. With Lean FIRE, you’re already a millionaire or on the verge of becoming one.

- Once you reach this level, you no longer have to work for a living and, if you live within your means, you can live off your dividends. So your life is 100 per cent your own.

- To achieve Lean FIRE, you need to have invested between €750,000 and €1 million, which only 0.5 per cent of the population manages to do.

- After tax, this portfolio generates dividends of over €1,800 every month – as much as many people’s salaries.

Stage 6: Classic FIRE

- From this stage onwards, you’ll enjoy financial independence without having to make any compromises. Reaching this point requires not only a high income (e.g. as an entrepreneur) but also great discipline when it comes to saving and a great deal of perseverance.

- With Classic FIRE, you need to have invested between €1.5 million and €2.0 million, which will provide you with monthly dividends of over €3,700.

- At this stage, you’ll be living the life of a well-paid employee – such as a senior consultant or a department head – but without any of the responsibilities that come with such a position.

- At this level, you are among the top 0.2 per cent of the population.

Level 7: Fat FIRE

- At this stage, you’ll need between €3 million and €10 million invested in ETFs. These will generate dividends of over €7,000 per month, after tax.

- Fat FIRE lets you do just about anything: from first-class flights and several holidays a year to expensive sports cars and costly treatments.

- The dividends you receive here usually exceed your expenses. This means you are not only building up wealth for yourself, but also for future generations.

- At this level, many investors are considering emigrating to countries with favourable tax regimes or setting up trusts.

- At this level, you are among the top 0.1 per cent of the population.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

My dividend portfolio: my investments for passive income

I have been investing in various asset classes for several years, partly so that I can live off my investment income in the future, and partly to diversify my investments.

My asset classes:

- ETFs

- individual shares

- P2P lendings

- Bitcoin

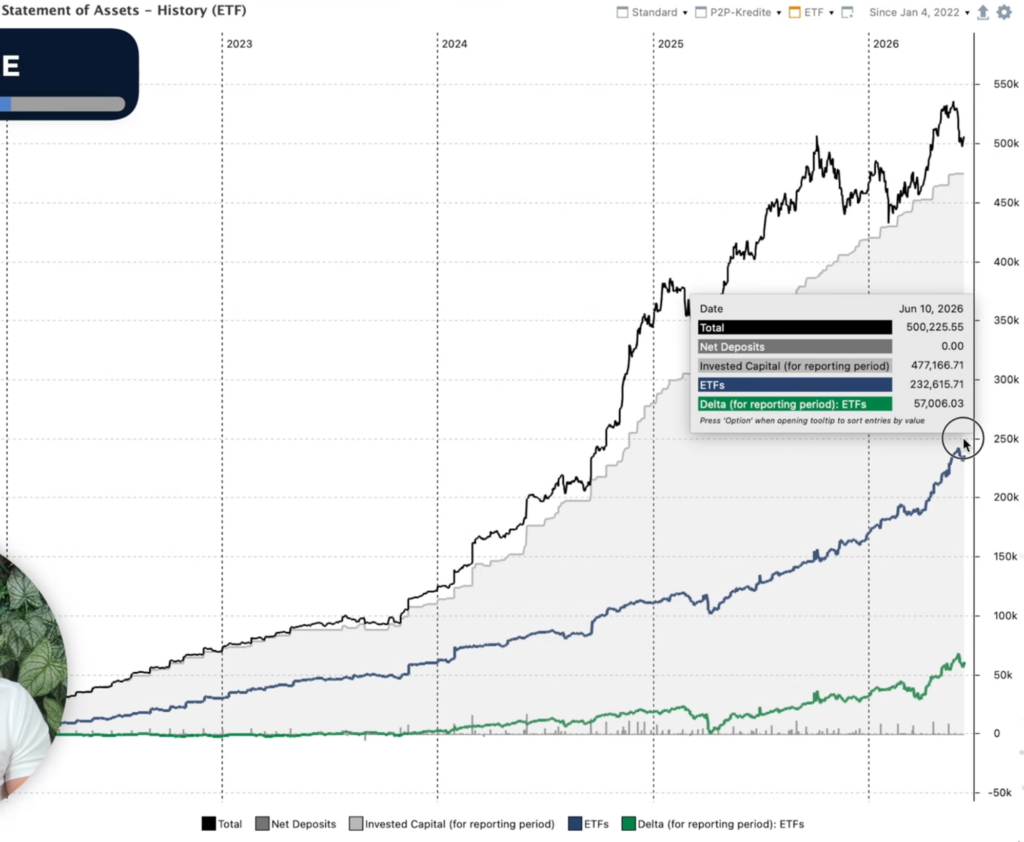

Through my ETF investments, I have already built up a portfolio worth €232,000, which puts me at Level 3: Coast FIRE.

I keep my ETF strategy relatively simple. I focus on:

- iShares Core MSCI World and the

- iShares Core MSCI Emerging Markets

Although these ETFs are not traditional dividend ETFs, they include many companies that pay dividends on a regular basis.

With these two ETFs, I track the majority of the global economy, spreading my investment across several thousand companies. In doing so, I make sure that I am always invested 50 per cent in each of the two ETFs.

In particular, the performance of my emerging markets ETF has skyrocketed since last year. My year-to-date performance here stands at almost 28 per cent! Whilst I don’t believe it will continue to perform at this rate, I will continue to invest in this ETF.

The MSCI World index is also performing well, with a year-to-date return of just under 11 per cent.

I’ve been using Freedom24 for my savings plans for several years now. I’m very happy with this broker, and if you’d like to get started on this platform too, you can regularly secure attractive bonuses. Take a look at my Freedom24 bonus review to find out more.

As well as ETFs, I also invest a small proportion of my portfolio in individual shares. These include:

- Wise plc

- Strategy (Microstrategy)

Here’s how you can build up passive income with ETFs

Individual shares, and ETFs in particular, are a popular way of steadily building up one’s wealth, in some cases passively. If you, too, would like to live off dividends one day, a targeted share or ETF strategy is a sensible approach.

Popular dividend shares:

- Coca-Cola

- Procter & Gamble

- Johnson & Johnson

- PepsiCo

- AbbVie

Popular dividend ETFs:

- Vanguard FTSE All-World High Dividend Yield UCITS ETF

- Fidelity Global Quality Income UCITS ETF

- SPDR S&P Global Dividend Aristocrats UCITS ETF

When devising your dividend strategy, bear the following in mind:

- Focus on high-quality companies: Especially when investing in individual shares, you should set aside enough time to carry out thorough research. Choose companies that have a sustainable business model and are known for paying regular dividends.

- Don’t just focus on the dividend yield: particularly high dividend yields may seem attractive at first glance, but they can also be the result of a sharp fall in the share price. You should therefore always consider a company’s overall performance.

- Take the payout ratio into account: Do not focus solely on a company’s payout ratio. Although a high ratio is generally a good sign, it means the company has less money left to invest in its own growth.

- Reinvesting dividends: The best way to grow your wealth quickly is to reinvest your returns. This allows you to benefit from the power of compound interest and means you can live off your dividends much sooner.

Common mistakes when investing

When investing in individual shares and ETFs, there are also common mistakes that can cost investors valuable returns. Avoid these from the outset to get the most out of your investments:

- No clear objectives: Investors who do not set clear objectives for their investments are investing haphazardly. Before you start, you should be clear about how much you want your dividends to be, how much capital you wish to invest in each individual share or ETF, and for how long this capital is to be tied up.

- Lack of diversification: The more capital you invest in individual shares, the higher the risk of losses. When investing, always ensure you have a good level of diversification to spread your risk, for example through ETFs.

- Ignoring inflation: Only by taking inflation into account can you work out what your real return is. Historically, inflation in the euro area has stood at around 2 per cent. So subtract this figure from your returns.

- Don’t forget about tax: dividends are also subject to tax. Remember to pay this on time if your broker does not do so automatically on your behalf.

- Don’t let your emotions dictate your decisions: always keep a cool head when investing. Investors who invest rationally and do not allow themselves to be thrown off balance by short-term fluctuations are more successful in the long term. Stay patient and consistent.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Conclusion: Living off dividends with the right strategy

Some people refer to the power of compound interest as the 8th wonder of the world, but it is still far from being fully understood by the general public. If that were the case, far more people would certainly be making the most of it.

If you want to live off dividends, you should invest in the right shares and ETFs and invest regularly over the long term. This is the only way your wealth can really start to grow, and it’s how you can take big steps towards financial freedom, even with modest amounts.

To start with, ETFs are a good option, as they allow you to invest passively across a large number of companies, thereby spreading your risk. Also, always keep your goal in mind and stay consistent. After all, investing is not a sprint but a marathon, which richly rewards investors with great perseverance.

FAQ: How can you live off dividends using simple methods?