My P2P lending review: over €100,000 invested

P2P lending have developed into an attractive investment opportunity in recent years. Their double-digit interest rates are particularly appealing in times of falling base rates or economic uncertainty.

But it’s not just the number of investors that continues to grow; the selection of P2P platforms is also steadily increasing. Below, I have summarised my experiences with P2P lending. Find out now what my P2P portfolio of more than €100,000 looks like in detail and how I generate up to 19.72% annual returns.

In brief:

- P2P lending offer attractive interest rates, which can reach up to 19.72 per cent per annum.

- Additional advantages include the possibility of diversification and the high liquidity offered by some providers.

- Past experience shows that P2P lending is more resilient to crises than other investment classes!

- However, a fundamental risk remains

- It is important to choose the right platform. I will show you a brief comparison of the best providers based on my experience.

P2P experiences: Why I invest in P2P lending

With P2P lending, private individuals like you and me can join forces and finance lending with our About 10 years ago, I started investing in P2P lending, and looking back, it was one of my best financial decisions. At the time, I was looking for a way to invest my money wisely without relying solely on traditional dividend stocks.

The average distributions of 2 to 4% on dividend stocks are nice to have, but I wanted more. It was important to me to achieve real financial freedom as quickly as possible. P2P lending, on the other hand, offered a good 12% interest rate and were therefore an attractive addition to my portfolio.

- Independence from the stock market: P2P returns are largely unaffected by stock market fluctuations, which is a major advantage in volatile times.

- Financial freedom: P2P lending provide me with regular passive income and bring me closer to my goal of achieving financial freedom.

- Diversification: P2P investments allow me to spread my risk more effectively across different asset classes.

- Attractive returns: Double-digit interest rates are not uncommon. This is significantly more than with dividend stocks or overnight money.

- Compound interest effect: Reinvested profits ensure exponential capital growth over time.

- Short-term availability: Many platforms offer buy-back programmes or secondary markets, which allow for greater flexibility.

- Automated strategies: Thanks to auto-invest functions, much of the process runs itself.

- Low barrier to entry: Even small amounts can be used to build a diversified loan portfolio.

My portfolio to replicate: Investing in P2P leding is this easy

My P2P investments now generate around €900 to €1,000 in passive income every month. This is a long-awaited milestone that I am really proud of. It brings me closer to financial freedom step by step, as I will soon be able to cover all my fixed costs with this income alone.

Looking back, I always dreamed of this kind of growth, but I was never sure if I would really be able to achieve it. A few years ago, my monthly income was still around €200 to €300.

Through consistent reinvestment, patience and the steady expansion of my portfolios, this has turned into a stable, reliable income. It feels great to see what long-term thinking and perseverance can achieve.

For me, P2P lending are now a real, super passive additional income that I have built up bit by bit on the side and that will continue to grow in the future.

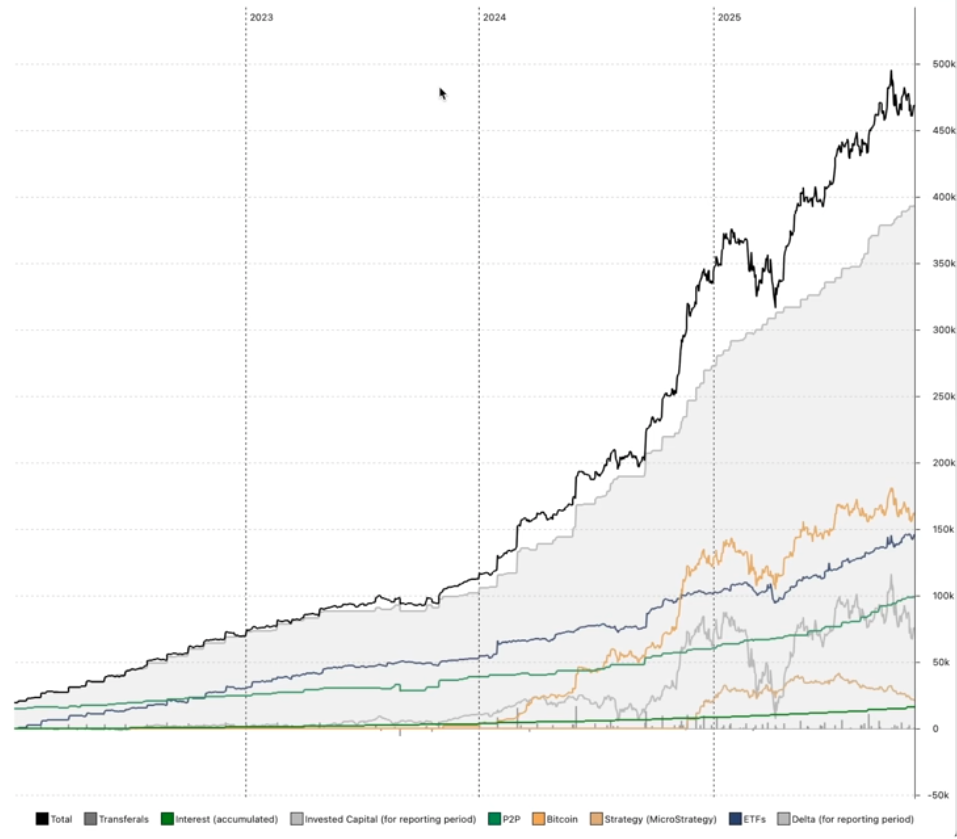

In January 2022, my total investments were still around €19,000, of which €15,000 was in P2P lending. By January 2023, my portfolio had grown to a total of €74,000, with €25,000 in P2P investments.

By 2024, my portfolio was already worth €114,000, €39,000 of which was in P2P platforms. In January 2025, it exploded to a total of €336,000, €61,000 of which was in P2P lending.

And now, in November 2025, I can look back on a proud portfolio value of €471,000. With my P2P investments, I have finally reached €100,000. That is around 21% of my portfolio.

In the long term, I would like to adjust this ratio to around 15% and further expand my ETFs. If you are interested in the exact composition of my portfolio, you can find a special article on this topic in my blog.

Good to know:

These investments earn me over €900 in interest per month! Ventus Energy, Monefit, Swaper and Debitum in particular provide this fantastic additional income.

P2P platform experiences: These are the best providers

In more than 10 years of P2P investing, I have had both good and bad experiences. Early on, I summarised my 5 worst platforms in a report.

However, a lot has changed since then: both the P2P market and my analysis methods have been refined. I reliably achieve up to 19.72% return per year through personal lending and, with this form of investment, I was able to weather the COVID crisis and the attack on Ukraine without major damage.

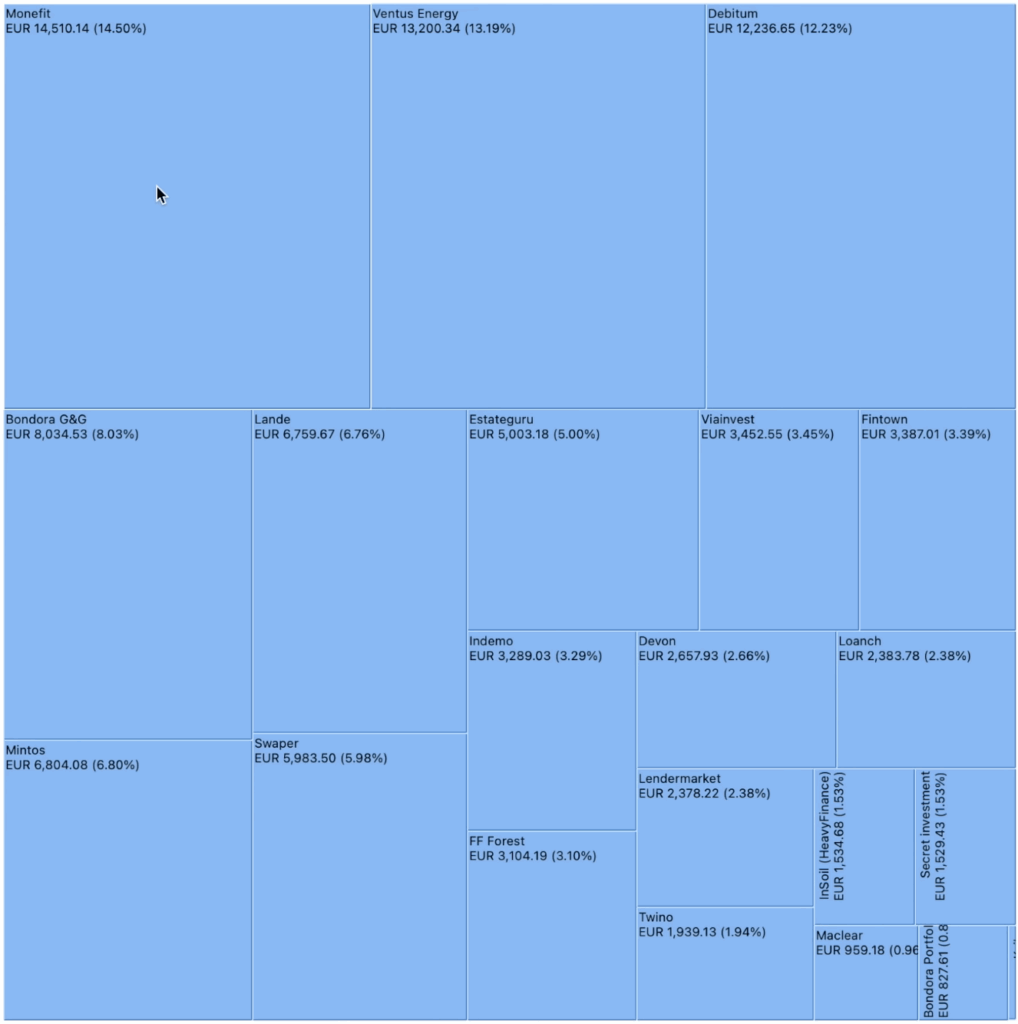

My P2P investments are spread across 14 P2P platforms, which I will present below and share my experiences with. The order is based on the respective weighting, i.e. the amount of my investments.

1. Monetfit Smartsaver: €14,260 invested, up to 10.52% return

Monefit belongs to a special category of P2P platforms: here, you make your money available directly to the company and do not have to select or manage the lending yourself. At 7.5%, the interest rates for SmartSaver are in the middle range for P2P, but in return you get a big advantage: you can withdraw your money at any time!

If you want to generate higher returns and are willing to accept slightly longer terms, you can earn around 10 to 10.5% per year with so-called vaults.

This makes Monefit suitable for your nest egg, as a substitute for instant access savings or for temporarily parking capital. It is a particularly simple way to grow your money, without having to worry about anything.

There is even a savings plan for automatic investments to make it even easier for you to build up your assets.

I have been with the platform since its launch and have had very good experiences with it so far. I particularly like the fact that the company is extremely profitable and has enormous reserves. This means I can face any crises with confidence.

You can find out more about the advantages and disadvantages in my Monefit experiences.

2. Ventus Energy: €13,200 invested, up to 19.72% return

No other P2P provider is growing as fast as Ventus Energy! It is an energy company from the Baltic region that operates power plants, solar plants, combined heat and power plants and other energy projects.

Ventus Energy is extremely successful because demand is high and the European Union provides generous subsidies. In addition, Ventus Energy often acquires power plants and other facilities at very low prices and modernises them. To do this, it uses capital from investors like you and me.

In return, I receive high-interest P2P lending with up to 19.72% interest, which can be increased to up to 24% through sign-up bonuses and cashback promotions! One disadvantage, however, is the very high minimum investment of €1,000.

Ventus Energy is ideal for investors who are looking for the highest returns and are willing to accept a slightly higher risk in return. I have been involved since the beginning and have now increased my investment to over €13,200. You can find out more about this in my Ventus Energy experience.

Ventus Energy is currently undergoing restructuring and is not accepting new investors or investments. That's why I'm investing my new funds on Monefit. As a welcome gift, you'll receive a €5 bonus + 0.75% (for 90 days).

3. Debitum Investments: €12,114 invested, up to 12.76% return

Most P2P platforms focus on consumer lending. Debitum is a welcome change, as here investments flow into business lending and earn an average interest rate of 12.76%.

I have been active here for many years and, like all other users, have only had good experiences: payments have always been punctual and reliable. Even in times of economic crisis, there were no noticeable problems!

Although Debitum always scores highly in my P2P lending ranking, it is still something of an insider tip: relatively few users have signed up so far. You can find out more in my report on my experiences with Debitum.

4. Bondora Go & Grow: €8,048 invested, up to 6.00% return

I currently have €8,048 invested in Go & Grow (formerly Bondora Go & Grow) and am earning a solid 6.00% return per year. In my opinion, the platform is a perfect, stress-free addition to other riskier P2P platforms in my portfolio.

Interest is credited daily, which really boosts the compound interest effect, and I can reinvest without a single click – all I have to do is deposit money! What I like best is the quick availability of my money.

Withdrawals are easy, at the touch of a button, and are in my bank account within seconds. This could make Bondora particularly exciting for someone who wants to invest flexibly.

5. LANDE: €7,813 invested, up to 16.00% return

Farmers need money too, and you can provide it to them through LANDE. Not only will you be supporting this vital industry, but you will also receive attractive interest rates averaging 11%. Some projects can even offer up to 16%!

Machinery, livestock or land are used as collateral. This means that such investments offer additional security that you will not find with other providers.

However, Lande offers an extremely exciting industry, good collateral and is ideal for diversification. Other investors have also noticed this: the number of users has been growing steadily for a long time!

I have now paused my investments and am monitoring how the situation at LANDE continues to develop. The reason for this is that the default rate here is higher than on other P2P platforms. In addition, it takes relatively longer to recover defaulted lending.

6. Mintos: €6,804 invested, up to 9.00% return

I currently have €6,804 invested with Mintos and am achieving a return of up to 9.00%. In recent months, I have been increasingly focusing on bonds, which currently make up around 60% of my Mintos portfolio, while traditional P2P lending still account for around 40%.

The reason for this shift is a number of lending defaults, while I am hoping for a better repayment rate on the bonds. The interest rates on the bonds are only slightly lower than on the lending, which I consider to be a good risk/return ratio.

Overall, I am very satisfied with the return of around 9% after defaults and am excited to see how this development continues in the future.

7. Swaper: €5,983 invested, up to 16.00% return

At first glance, Swaper appears to be a typical consumer credit platform. However, in addition to the very attractive 16% interest rate, there is another advantage that is not immediately apparent: you can sell lending you have invested in to other investors in a matter of seconds!

This means you can exit an investment at any time. In my experience, this makes Swaper one of the most flexible P2P lending providers around!

I also really like Swaper’s auto-invest feature because it makes the whole process completely stress-free. Simply set criteria such as amount, term or interest rate, turn on reinvestment, and boom, the algorithm invests in suitable lending around the clock without me having to constantly worry about it.

In my Swaper experiences, I have compiled further important facts for you.

7.5%–10.5% interest

8. Estateguru: €4,992 invested, up to 9.60% return

At this point, I must honestly admit that investing in Estateguru was my biggest mistake in the P2P sector to date. Currently, only a third of my original €15,000 is still invested.

Unfortunately, a large number of lending worth €4,184 have defaulted, and it is uncertain whether they will ever be repaid. For this reason, I am letting the lending expire and will observe how the platform develops in the future.

Due to the high level of loan defaults currently at EstateGuru, I am currently investing my capital in Viainvest (obtained with this link*). With Viainvest I earn over 13% interest, which is significantly more than with EstateGuru. As a welcome bonus, you will only receive 1% cashback on your investment after 90 days via this link.

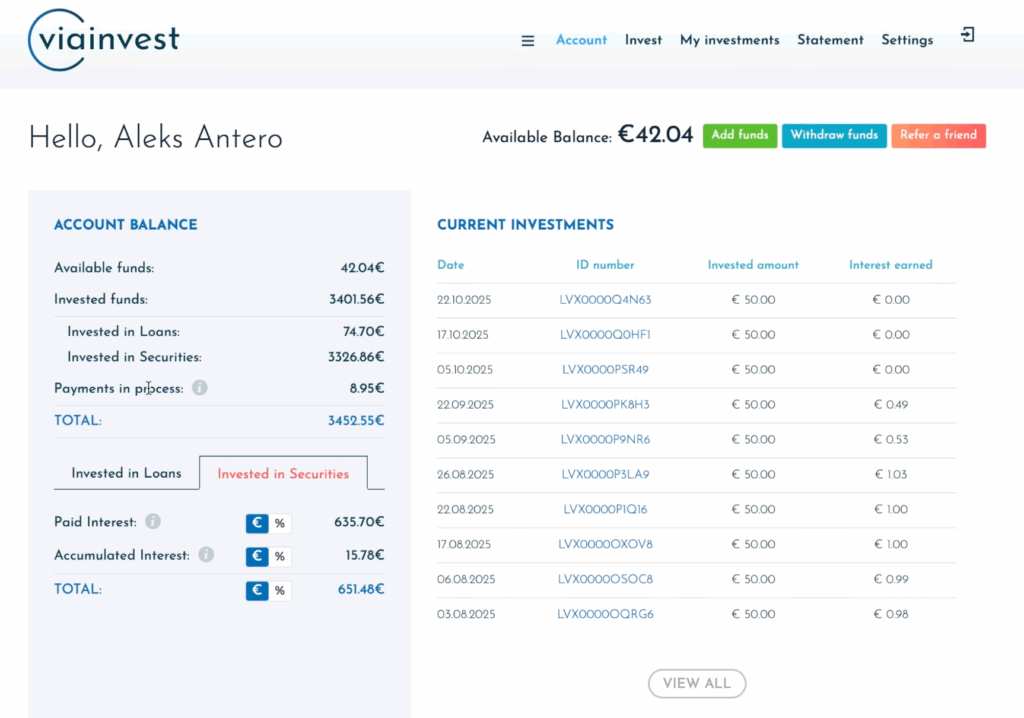

Viainvest: €3,452 invested, up to 13.30% return

I have had very good experiences with Viainvest so far. The platform has been running smoothly for me for a long time, payouts have been on time and there have been no defaults that would have significantly reduced my returns.

I am seriously considering increasing my current investment of €3,452 in order to further expand my broad diversification.

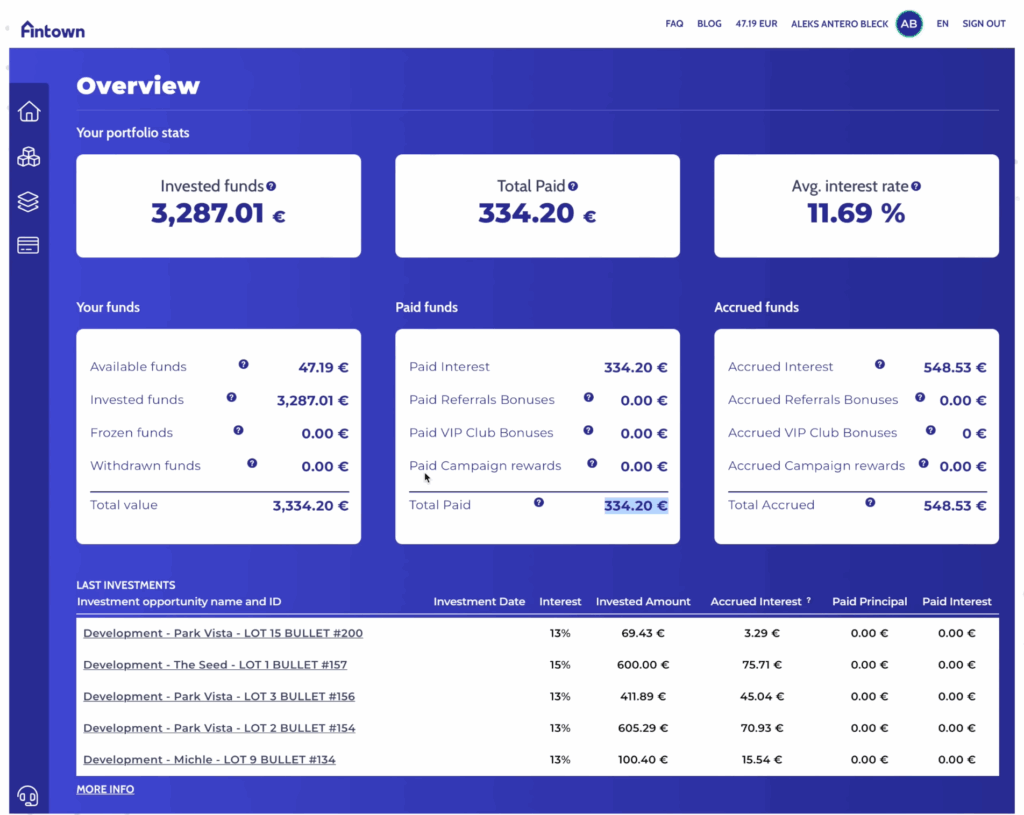

10. Fintown: €3,287 invested, up to 11.69% return

For me, Fintown has been an exciting addition to the P2P/real estate sector so far. The platform pays out interest from rental properties on a regular basis.

I find the model of investing in already rented flats and thus achieving returns in the range of around 10 to 12% per annum particularly exciting, even if Fintown, as a young, unregulated platform, naturally carries an increased risk.

I will continue to increase my investments in Fintown in the future, but always with the awareness that this is a speculative investment without deposit protection, which should only make up part of a broadly diversified portfolio.

11. Indemo: €2,577 invested, up to 25.30% return

Indemo’s business model differs from the other platforms presented here. As a private investor, you gain access to lending secured by Spanish real estate, which are normally only available to institutional investors. The potential returns are well above the P2P average.

However, payouts at Indemo are irregular because the recovery period for these defaulted lending varies greatly. Some projects offer more than 30% interest. On average, I have already earned a 25.3% return per year.

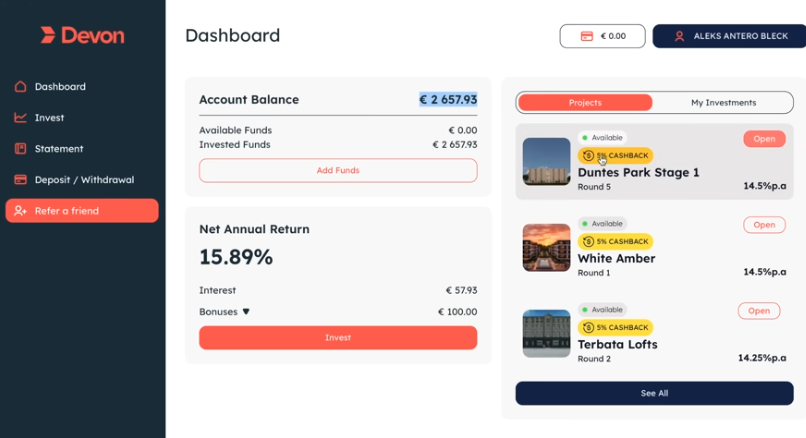

12. Devon: €2,657 invested, up to 15.89% return

I recently added Devon to my portfolio and am currently invested with around €2,657, which has yielded a strong return of approximately 15.89% so far. The platform of the Latvian MJL Enterprises Group, with over 30 years of experience, impresses with transparent real estate projects with repurchase after 90 days, including a secondary market after 6 months.

I was also on site in Latvia to take a look at a current project. I was impressed by the affordable and energy-efficient construction method. I also feel good about the fact that Devon is also building social housing, which underlines its sustainability.

13. Loanch: €2,374 invested, up to 14.50% return

Loanch focuses on consumer lending from Southeast Asia (e.g. Indonesia, Malaysia) with returns of 13 to 14.5% per annum.

I really like the minimum investment of €10 in combination with the auto-invest feature.

14. FF Forest: €3,104 invested, up to 18.00% return

FF Forest is a young Latvian P2P platform for forestry projects that promises high-interest P2P lending with an 18% annual return. Currently, you can even get 3% cashback + 1% additional bonus exclusively through my link, giving you a total annual return of 22%!

The company purchases undervalued or cleared land, reforests it (with CO₂ certificates as a source of income), manages it efficiently and sells it at a profit to investors or banks. Read my experience report on FF Forest for more information.

Conclusion: Are P2P lending a good investment? For me, absolutely!

I have been investing in P2P lending for over 10 years and have now invested more than €100,000 in this asset class. My experience has been almost entirely positive!

Apart from a few minor disappointments (late or incomplete repayments) and one insolvency, P2P providers have delivered what they promised: high interest rates, broad diversification and exciting extras.

- For example, with Monefit, you can withdraw your money at any time and use it as a substitute for a call account.

- Lande offers you investments in agriculture that are secured with tangible assets such as machinery or land.

- Through Debitum Investments, you can lend your money to companies.

- With Swaper, you finance consumer lending and can get your money back very quickly if necessary.

- Ventus Energy operates power plants and other energy projects.

- With FF Forest, you can contribute to improving our planet’s carbon footprint through reforestation.

Choosing the right P2P companies is essential, as there are serious risks involved: borrowers may default, payments may be late, or even the entire platform may go bankrupt!

Based on my personal experience, I therefore recommend only investing in offers that are regulated and publish annual reports.

A buy-back guarantee is also very useful, but is not possible with some P2P lending due to their structure. In these cases, you should only invest money that you can do without for a longer period of time.

If you pay attention to these points and can generally accept a basic level of risk, you can expect high interest rates and great flexibility. Auc

FAQ – Frequently asked questions about the P2P lending experience