Are we facing a cash ban? Here’s how you can protect your assets

Imagine you are standing in a pharmacy and urgently need to buy some medicine. But only digital payments are accepted. Even though you have cash, you can no longer buy it. What sounded like a theoretical discussion a few years ago may soon become reality in many countries.

Cash is gradually being phased out, while cards, apps and soon the digital euro will dominate everyday life. In this article, you will learn what the term ‘cash ban’ really means, what political and technical developments are taking place in the background, and what concrete options you have to preserve your financial freedom and anonymity.

In brief:

- Cash limits of €10,000 across the EU from 2027

- Obligation to accept the digital euro, programmable money (negative interest rates, CO₂ limits, social scoring).

- Protect yourself from the cash ban by consistently paying in cash, holding precious metals and cash reserves, using cryptocurrency (cold wallets) and signing petitions.

Understanding the cash ban

A ban on cash does not have to start as an explicit ban by law, but can creep in over years through upper limits, costs, convenience and the dismantling of infrastructure.

The decisive factor is that, at a certain point, so little cash is paid that the system can be declared politically and economically ‘superfluous’.

- A cash ban can be implemented formally (legal prohibition) or de facto (cash is practically unusable).

- The digital euro and other digital payments are accelerating the structural displacement of cash.

- Current and planned EU regulations (cash limits, obligation to accept e-euros) are systematically shifting the system away from cash.

Formal ban on cash vs. gradual abolition

The term ‘cash ban’ is often misunderstood. A formal ban would be a clear law that makes cash payments completely illegal or illegal above certain amounts, as is already the case in some countries with strict upper limits.

In Greece, for example, any cash payment over €500 has been a criminal offence for years, which makes it virtually impossible to purchase larger items such as laptops, cars or furniture.

But the real danger lies in the creeping abolition, which is more subtle. Here, cash is not banned, but made unattractive: retailers put up ‘no cash’ signs, cash machines disappear and fees rise.

Over the years, usage declines until the expensive infrastructure (logistics, vending machines) is deemed ‘disproportionate’ and dismantled.

| Strategy | Formal prohibition | Creeping abolition |

| Example | Punishable by a fine of over €500 (Greece) | Fewer machines, refusal to accept |

| Time frame | Immediate effect | 5 to 10 years until tipping point |

| Effect | Visibly exposed | Barely noticeable until it’s too late |

In the end, cash may remain legal, but it will be practically useless. In other words, a perfect cash ban without any loud headlines.

first 30€ purchase

Cash, bank deposits and the digital euro at a glance

Our monetary system is based on three pillars that differ fundamentally in terms of control and freedom. Cash consists of physical notes and coins. It is anonymous, can be used offline and is the only genuine legal tender without upper limits (at least in Germany so far). It protects against digital tracking and can always be used, even in crises.

Bank deposits, on the other hand, consists of entries in your account that banks create out of thin air. It is entirely digital, every penny is traceable, and it can be frozen by banks and authorities at any time. This happened in Cyprus in 2013, for example, when accounts exceeding €100,000 were reduced.

The digital euro (e-euro) is being added as a new form of central bank money: also digital, but with planned mandatory acceptance in trade and potentially programmable features.

| Form of money | Anonymity | Can it be used offline? | Controllable? | Status |

| Cash | High | Yes | Low | Legal tender |

| Bank deposits | Low | No | High (banks) | Book money |

| Digital euro | Low | No | Very high (ECB) | Planned legal measure |

While cash offers freedom, bank deposits and e-euros open the door to total transaction control.

Why this topic is so controversial right now

The debate surrounding the cash ban is escalating for several reasons at once. In Northern Europe, such as Norway (only 3% cash payment rate) or Sweden (approx. 10%), cash is almost dead and is no longer accepted in some shops.

At the same time, many EU countries are continuing to lower their upper limits, and from 2027 onwards, the €10,000 limit will apply across the EU.

Particularly alarming: the proposed e-euro regulation of 2023 calls for mandatory acceptance of digital money, while cash can simply be rejected. This threatens scenarios such as negative interest rates or programmable money, with no cash as a way out.

Ways to ban cash: laws, e-euro & infrastructure

The displacement of cash is not happening with a bang, but rather through a network of laws, technical developments and economic constraints that complement each other perfectly in terms of banning cash.

EU regulations, declining usage figures and the digital euro are working like a well-oiled machine to systematically remove cash from circulation.

- Salami tactics make cash payments more expensive, less practical and criminalised.

- The tipping point at less than 10 to 15% cash payment ratio justifies infrastructure reduction.

- Cash limits already exist in many EU countries, and from 2027 onwards, the EU-wide limit will be €10,000.

- The e-euro is given preferential treatment, while cash is disadvantaged.

Salami tactics: How cash is being gradually phased out

Jean-Claude Juncker (former President of the European Commission) once put it aptly: you decide something and wait to see if there is an outcry. If not, you carry on. That is exactly how the salami tactic works with cash: thin slices of freedom are cut away until there is nothing left.

First, large denomination banknotes are criminalised. The 500-euro note was discontinued in 2018 and defamed as the ‘Bin Laden note’, even though the 1,000-CHF note continues to be produced normally in Switzerland. Petrol stations and shops refuse to accept it, even though counterfeit money detectors exist.

At the same time, fees for withdrawals are increasing and cash machines are becoming scarce. Digital payment methods such as Apple Pay are being subsidised and countless credit card providers are constantly beating the advertising drum.

In the end, demand falls so far that no one protests anymore. The goal of banning cash is getting closer and closer.

Cash payment ratio and tipping point of the cash infrastructure

Cash requires an expensive infrastructure: cash transports, ATMs, counting machines. However, as long as many people pay in cash, these costs are proportionate. If the proportion of cash payments in retail falls below 10%, the argument is no longer valid and the costs exceed the benefits.

Nordic countries are leading the way in this disaster: Norway at 3%, Sweden at 10%. In the Netherlands and Germany, the cash ratio is still above 20%.

| Country | Cash payment ratio | Status |

| Norway | 3% | Below the tipping point |

| Sweden | ~10% | Critical |

| Netherlands | 21% | Declining |

| Germany | Still >20% | Endangered |

Once the tipping point is reached, the Bundesbank can argue that it is ‘too expensive for so few users’. The result would be the demise of cash.

first 30€ purchase

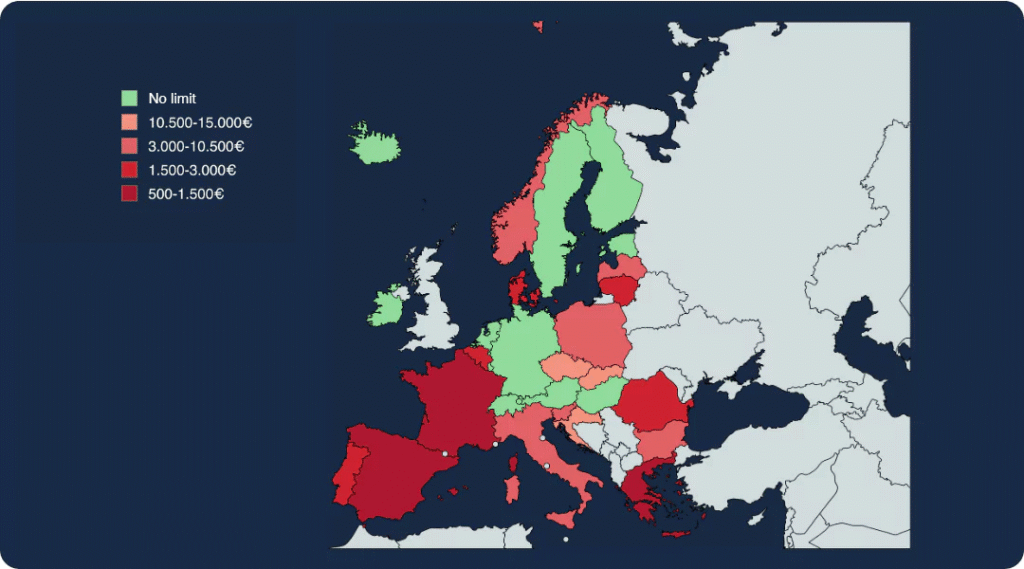

Cash limits in Europe

Cash limits are effectively partial bans: cash payments above this amount are punishable by law. Most EU countries already have limits in place at various levels, as shown in the following chart.

Digital euro: how it works and its role as an accelerator

The digital euro is ECB money in a wallet app and a powerful accelerator of cash displacement. The digital euro is fully traceable and potentially programmable.

- Cash: High anonymity, offline use and crisis-proof

- E-euro: Electricity-dependent, transparent and manipulable

The proposed e-euro regulation of 28 June 2023 (Article 10) stipulates a strict obligation to accept e-euros: retailers may not simply refuse them by displaying a sign. However, the parallel regulation does not impose any such obligation with regard to cash. ‘No cash!’ signs are therefore legal and will become increasingly common in future.

The EU is thus systematically favouring the new over the tried and tested. The clear discrimination is that the e-euro must be accepted, while cash is becoming increasingly unattractive and is being phased out.

Consequences of a cash ban for you as a citizen

Without cash, every transaction becomes traceable; programmable money enables total control of consumption, mobility and freedom; worst-case scenarios harbour the risk of social credit systems, crypto bans and crisis financing without democratic control.

The loss of anonymity and autonomy affects everyone directly and erodes fundamental civil liberties in the long term.

- Every payment is logged. There are no more private transactions.

- Negative interest rates, CO₂ limits or spatial restrictions.

- Total surveillance, payment blocks for dissenters in the worst case.

- In the best-case scenario, diversity with cash protects freedom in the long term.

Loss of anonymity, privacy and freedom of transaction

In a cashless world, every transaction is seamlessly recorded: from your daily coffee to donations to opposition figures, flea market purchases or private gifts to family members.

Anonymous aid efforts in crises, neighbourhood assistance, or small private businesses become impossible. Everything becomes traceable and potentially blockable.

The existing banking secrecy will be broken when cash is no longer used. If cash is banned, the state and corporations will know everything about consumer behaviour, political attitudes and social networks, leading to total transparency with no way to evade it.

| Transaction | With cash | Without cash |

| Coffee | Anonymous | Logged and traceable |

| Donation | Anonymous | Logged and traceable |

| Flea market | Anonymous | Logged and traceable |

Programmable money: negative interest rates, CO₂ budgets and spatial restrictions

Programmable money empowers central banks to control your money. Negative interest rates of, for example, 5 to 8% cause your credit balance to shrink in order to finance banking crises or government deficits. As a citizen, you can no longer evade this by using cash.

CO₂ budgets could put an expiry date on your money if you overconsume, while spatial limits could restrict your use to, say, 30 kilometres, putting you in a digital prison.

Without neutral cash, money becomes the ultimate instrument of control. Thanks to modern technology and AI, this is not a technical challenge for the ECB.

Top 3 investments despite cash ban

If you want to protect your assets from a possible cash ban, it is worth considering alternative investments. There are both physical and digital options available to you, not all of which correlate with the stock market.

- Cryptocurrencies: A popular option is to invest in cryptocurrencies, which you can store securely in a cold wallet, i.e. offline and out of reach of banks or government access. This allows you to retain full control over your digital assets. Alternatively, you could also consider crypto ETFs.

- Gold: Gold can also offer a stable counterbalance. You don’t necessarily have to buy physical bars, as commodity ETFs also allow you to participate in the performance of precious metals without having to store them yourself.

- P2P lending: In addition, P2P lending via platforms such as Mintos or Bondora are an interesting addition. They give you the opportunity to invest directly in private or business lending and thus earn regular interest.

How you can protect yourself from the cash ban

In addition to daily cash payments and political activity, there are concrete, expanded strategies for securing financial sovereignty: diversification, crisis prevention and legal protection guard against displacement and control. Each measure strengthens the cash payment ratio or creates independent alternatives.

- Significantly expand your physical reserves: Store at least 3 to 6 months, preferably up to 12 months, of living expenses in cash, packed in waterproof containers and distributed in different locations (at home, in a safe, with trusted relatives). Supplement these reserves with precious metals in gold and silver. Ideally, as with cash, choose small denominations so that you can exchange them at any time. This will allow you to remain independent and solvent even during a blackout or banking crisis.

- Use cryptocurrencies wisely: Keep cryptocurrencies such as Bitcoin and Monero in cold wallets (hardware such as Ledger), never on exchanges that can be hacked or blocked. Use the Lightning Network for fast, anonymous small payments that work like cash. Learn self-custody: your private key, your coins. No one can take them away from you. If bans are imposed, you can fall back on offshore wallets or decentralised exchanges.

- Local networks & barter economy: Set up neighbourhood groups for exchanging goods and services (apps such as LocalBitcoins or private groups). Learn skills (repair, gardening, hair cutting) that work without money. In times of crisis, you can offer these services and do business independently of the current monetary system.

- Take political and legal action: sign and distribute petitions advocating for the preservation of cash and contact your representatives. Join citizens’ initiatives or associations that are fighting for cash and demand official transparency on all e-euro plans. The more voices, the more effective.

- Secure yourself technically: Protect your digital finances with privacy tools. Use VPNs for anonymous online banking and decentralised wallets for cryptocurrencies. Try out offline payment options that simulate cash equivalents and work without the internet.

first 30€ purchase

Conclusion: Take action now and protect yourself from the cash ban.

Cash is gradually disappearing with the EU cash limit of €10,000 from 2027. The digital euro comes with mandatory acceptance, while the cash ratio in Germany is only around 20% and will continue to fall in the future.

Protect yourself from the cash ban! Without resistance, negative interest rates, CO₂ limits and total surveillance await. But you can take action and fight back.

Pay cash every day, whether at the bakery or when filling up your car, build up a reserve of at least three to twelve months’ salary, mix in crypto in cold wallets and gold (for example, through commodity ETFs). Also, take advantage of alternative investments, such as P2P lending with Mintos or Bondora.

Also, write to your MP and sign relevant petitions. Every little bit counts; your freedom depends on the impending cash ban.

FAQ: Frequently asked questions about the cash ban