The big savings plan comparison: your top investments (2026)

Want to start investing with relatively small amounts and build up your financial future? Create an independent hedge against inflation so you can face the coming years of crisis with peace of mind? Build up a passive income? The answer to these questions is: savings plans. But to save you from having to wander aimlessly through the jungle of hundreds of different savings plans on offer, this article provides a comparison of savings plans to help you in your search.

In brief:

- Savings plans are among the most popular asset classes in 2024

- Its popularity is on the rise, particularly amongst younger investors, due to the low initial investment required

- The various types of savings plans each have their own advantages and disadvantages, depending on the investment objective

What is a savings plan?

The term is often used, even though not everyone knows exactly what a savings plan actually is. It’s time to take a closer look at the precise definition.

A savings plan is essentially just a contract between an investor (you) and a bank or investment company. Under the terms of the contract, you make regular payments into an investment of your choice. These investments can vary widely, ranging from securities and funds to sustainable ETFs.

The amount you pay in is up to you. Some banks or investment firms require a minimum contribution, whilst others (particularly so-called ‘neo-brokers’) allow you to invest regularly from as little as one euro a month. The objectives of savings plans can vary considerably:

- Active saving by contributing to a savings plan. The aim is not simply to put money aside, as was commonly done in the past, where it loses value, but to offset inflation through active investment in a savings plan and thus preserve the value of one’s money.

- More and more investors are dreaming of a relatively substantial retirement provision (known as a ‘share-based pension’) through their savings plans. By saving continuously and, ideally, growing their money in savings plans, the aim is to build up such a reserve.

- The ultimate goal, which is simply regarded as ‘the dream’, is to build up a passive income through savings plans. The idea behind this additional source of income is to use the returns generated by investing to build up a passive income.

Whatever your goal or motivation for starting a savings plan, by reading this article you’re on the right track. Now you’re probably keen to find out what the different types of savings plans are!

5 Different types of savings plans

As mentioned earlier, there is a wide variety of savings plans available. You’ll now get a detailed insight into the different types of savings plans and their respective pros and cons!

Bank savings plan

The bank savings plan is often regarded as the ‘mother of all savings plans’. It is, so to speak, the starting point for all subsequent savings plans. The basic idea is that banks enter into a contract with their customers which specifies a fixed monthly savings amount, a guaranteed annual fixed interest rate or a variable interest rate. This means that, when the contract is signed, it is already clear what amount you can expect to receive at the end of the term.

This type of savings scheme is now actually very rare, but they do still exist. Savings banks, in particular, offer what is known as ‘bonus savings’.

| Advantages | Disadvantages |

| Fixed interest rates and expected amounts | In some cases, very low discount rates, resulting in a relatively low final amount |

| Independent of economic influences | Very inflexible – early exit sometimes not possible/sensible and no response to market changes |

| “Traditional” banks rather than neo-brokers | Depending on the bank where the savings plan is held – consider the risk of insolvency. |

The share savings plan

This savings plan involves buying a single share at monthly intervals. So, instead of sending a certain amount to your bank each month, you invest via a so-called broker. This particular broker then offers you the opportunity to purchase shares. With most brokers – and particularly the neo-brokers, such as the two largest in Germany, Scalable Capital and Trade Republic – you can even do this almost free of charge.

Depending on how much you want your monthly savings allocation to be, you’ll naturally only ever be buying a fraction of a share. This means you can invest in any company, even tech giants such as Apple or Nvidia.

As well as the companies’ dividends, you should also look at their annual growth and market capitalisation. Think carefully about which company you want to include in your share savings plan. Perhaps there’s a particular company – or something else – that you feel a special connection to.

| Advantages | Disadvantages |

| High dividends can provide a source of passive income. | Choosing the right company can often be overwhelming, which may lead you to make a hasty decision – or not make one at all. |

| By investing in fractions of shares, you can invest in specific companies in a targeted manner. | By focusing on a single share, you become heavily reliant on it. Crises or other changes can have a major impact on your savings plan. |

| More flexible than a bank savings account, as you can manage your own investments here – particularly with neo-brokers. | Investing in a single share is a bit of a gamble. You’re always on the lookout and can always find a share that might actually be a better fit. However, constantly reshuffling and rearranging your savings plan is anything but sensible. |

The fund savings plan

What is a fund, and how does investing in funds work? You can think of a fund as a big pot containing a wide variety of shares and bonds. A fund manager uses the investors’ money to buy and sell units, ensuring that the fund remains profitable.

The fund manager and their team are therefore responsible for managing your savings plan and ensuring it performs well. You can also buy funds through any type of broker. But be aware: not every fund is suitable for a savings plan.

You can choose your fund based on various criteria. Either you have an investor you trust who manages their own fund – prominent examples of this would be Warren Buffett or Frank Thelen – or you look at the fund’s recent performance and decide whether its assets and investment decisions appeal to you.

| Advantages | Disadvantages |

| The fund manager’s expertise. They essentially take care of the investing for you. This is often a major advantage if they’re really good at what they do. | One of the consequences of investing in a managed fund is that costs can be high, due to fund management fees and initial sales charges. |

| Compared to a share savings plan, you benefit from a high degree of diversification. This can include a wide variety of different shares, but also different asset classes such as shares, gold, etc. | You are reliant on your fund manager. By investing in their fund, you are placing your trust in them to make the right decisions. Should this not be the case on occasion, the value of your savings plan may fall. |

| Thanks to the diversification I’ve just mentioned, you simply face less risk whilst retaining, in some cases, the same chance of a higher dividend. | With this option, too, you’re quite limited in your flexibility. Of course, you have the option to invest in other funds at any time, but the fund manager’s team makes the decisions for you, and you have no say in the matter. |

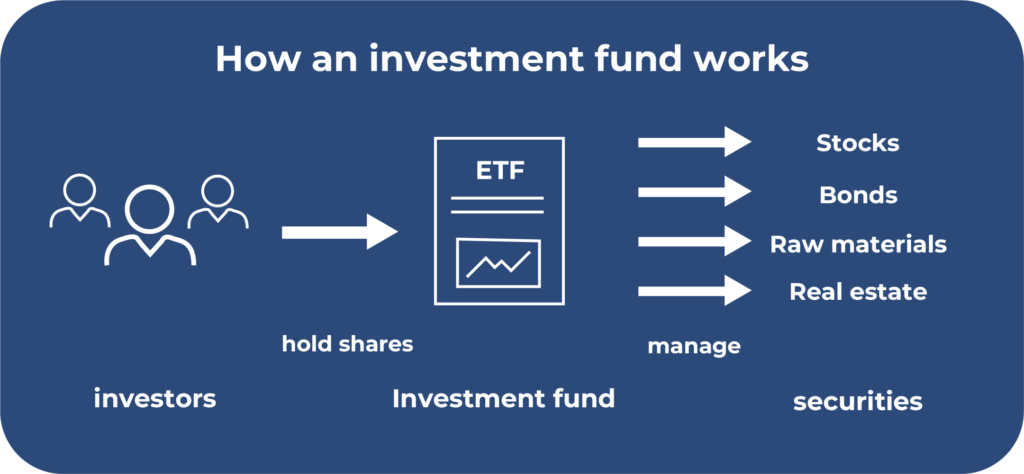

The ETF savings plan

An ETF is, in effect, the more cost-effective alternative to traditional funds. The principle is essentially the same – investments are made in various shares (in fractions). ETFs track exchange-traded index funds. These track the performance of an index such as the DAX or the MSCI World Index. The shares traded on these indices are included in a list, and as the index changes, so does the ETF.

ETFs have become increasingly popular, particularly in recent years. Every ETF savings plan comparison aims to identify the best ETF for different types of investor. This is because, much like mutual funds, ETFs can be structured to be either risk-averse or risk-seeking, depending on the index they track.

| Advantages | Disadvantages |

| Low costs; some providers don’t even charge any fees for investing in ETFs. Da diese nicht gemanagt werden, entfällt auch dieser potenzielle Kostenpunkt. | The ETF savings plan is somewhat “left to its own devices”. Depending on their focus, the indices are entirely at the mercy of the economy. This applies particularly to ETFs that track the global economy. |

| They are completely independent; the relevant index is not monitored by humans but operates automatically. | A degree of caution is advised when it comes to so-called “thematic ETFs”. These are sometimes based on simple trends and do not constitute a genuine index. Examples would include crypto ETFs and the like. |

| Otherwise, you get the same benefits as when investing in funds: potentially high dividends, broad diversification, etc. | |

| Established ETFs sometimes have a lower cost-average effect due to the large number of investors per ETF |

The Riester savings scheme

Although it has fallen out of favour somewhat recently, the Riester savings scheme used to be the model savings plan. This scheme involves state-subsidised savings through selected investment products, which may include funds, insurance policies and bank savings plans. The Riester savings scheme is known for being very conservative. The support takes the form of subsidies and, in some cases, even tax benefits.

The savings scheme actually works in the same way as every other fund-based savings plan presented so far. Investors pay an amount of their choosing into the Riester savings plan, and the managed fund invests its investors’ assets.

| Advantages | Disadvantages |

| The savings plan benefits from substantial government subsidies. This ensures a relatively high degree of stability. You are not dependent on individual shares or banking institutions. | These extremely conservative investments can sometimes put people off. Some people tend to doubt that the Riester savings scheme is a genuine success or a worthwhile investment. |

| Investing offers investors a number of tax benefits. For example, it is possible to claim tax relief on a savings plan and enjoy additional tax benefits instead of government grants. One of these benefits is state support. | Funds and ETFs are straightforward to understand – but the situation is rather different with the Riester savings scheme. The wide variety of investment options and so on often makes it difficult for the average person to understand exactly what is happening to their money. |

| In some cases, the fees are high, although they vary considerably from provider to provider. Generally speaking, however, the costs are not really commensurate with the service, which is usually disappointing. |

The Big Savings Plan Comparison

You’ve now been given a really detailed overview of many possible savings plans. But before we get to the big comparison, here are a few more words on how the savings plans were selected and how they’ve been assessed.

Of course, there are other schemes that would allow you to save money using a system similar to a savings plan. However, the schemes presented here are probably the most popular and successful savings plans. The Riester savings plan, however, is not included in this comparison. The Riester pension is an interesting concept, but it is simply no longer in step with the times.

The aim is to give you a clear picture of the situation and help you identify the savings plan that best suits you. However much advice you may receive, ultimately it will be your own preferences or personal criteria that determine which model you choose.

In this comparison, we examine three categories: flexibility / decision-making autonomy, which assesses the extent to which you can influence the course of the savings plan. The second category is stability, which concerns the future prospects of the savings plan in question and the certainty with which you can plan for your future. The final category concerns the costs of the savings plan in question and the scale on which you need to take these into account.

Category 1: Flexibility / Self-determination:

| Bank savings plan | Share savings plan | Fund savings plan | ETF savings plan |

| The bank savings plan is the most rigid on our list. Once you’ve signed the contract, you’ll receive the pre-agreed amount when it matures. You have no say in the matter. | With a share savings plan, you’re obviously spoilt for choice and enjoy a great deal of flexibility at the start, as you get to choose the shares yourself. Once you’ve made your choice, however, you’re bound by it and shouldn’t change your mind too quickly. | The fund-based savings plan offers a little more flexibility. Thanks to active fund management, you can choose virtually any investment mix. However, once you’ve made your decision, others will make the decisions for you. | Probably the most flexible savings plan of all. No one else decides for you: you choose the index that best suits your needs! |

Overall, the issue of flexibility in savings plans is, in general, quite complex. Once you have chosen a savings plan, it is advisable to continue making contributions for at least 15 years. This is the only way to offset the ups and downs. Nevertheless, an ETF savings plan offers you the greatest possible flexibility.

Category 2: Stability

| Bank savings plan | Share savings plan | Fund savings plan | ETF savings plan |

| In terms of stability, the bank savings plan stands out as a positive option. Right from the start, you know exactly what to expect and, in the end, that is exactly what you get. There are no surprises or anything of that sort. | This is probably the most volatile savings plan on the list. By investing in a single share, you are fully exposed to its price fluctuations. Of course, some shares are more stable than others, but in general they are highly volatile. | The fund-based savings plan is, of course, subject to general economic fluctuations, but thanks to active management, it is able to counteract them effectively. | As there is no fund manager overseeing the ETF, it is 100% exposed to fluctuations in the value of its constituent securities. Thematic ETFs, in particular, are heavily affected by this. |

When it comes to stability, the bank savings plan and the fund savings plan stand out. Of course, the bank savings plan is still slightly more stable, but thanks to active management, the fund savings plan is every bit as good as the former.

Category 3: Costs

| Bank savings plan | Share savings plan | Fund savings plan | ETF savings plan |

| Unfortunately, some bank savings plans come with higher costs. Banks charge a fair bit for this service and levy corresponding fees. | You can usually set up a share savings plan relatively cheaply, or even for free. You don’t need anyone to manage this savings plan. You’re essentially your own boss. | Often involves higher costs and fees. Because of the managers involved, this savings plan is probably one of the most expensive. Well-known investors, in particular, charge a high fee for their services. | The situation here is similar to that of a share savings plan. There are few, if any, fees. |

As they allow you to invest independently, thereby eliminating costly management fees, share and ETF savings plans offer the best value for money.

Investments always involve the risk of loss The WELCOME promotion is

subject to Terms and Conditions. Gift Shares are allocated randomly from a

selection of eligible stocks, with higher-value shares awarded less frequently.

Conclusion on the savings plan comparison: winners and losers

Savings plans are the future of smart retirement planning. That is undeniable. In this article, you have learnt a great deal about the various types and forms of savings plans, their respective pros and cons, and we have carried out a comprehensive comparison of savings plans.

It has become clear that tastes vary and that everyone should choose a savings plan that suits them best. If security and stability are important to you, even a traditional bank savings account is an option. If, on the other hand, you’d prefer to put your trust in an expert and their know-how, a fund savings plan could be the way forward. If you’re looking for something independent with low costs, an ETF savings plan is also worth considering. The choice is entirely yours.

You might also be interested in topics such as “broker comparisons”, “investing in P2P loans” or “buying shares”? Find out more here.

FAQ – Frequently asked questions