Living off interest: How I earn €1,000 a month passively

Like many other investors, you probably also want to become financially independent and no longer have to trade your precious time for money. A popular way of achieving this is to be able to live off interest one day.

But which investment strategies are best for generating passive income, and how much money do you need to invest to achieve this? In today’s post, I’ll show you how I earn over €1,000 a month in passive income and how you too can increase your passive income.

In brief:

- How much capital you need to live off the interest is a personal matter and depends heavily on your lifestyle and the expected interest rate.

- High-yield asset classes such as P2P loans help you build your wealth more quickly, whilst traditional asset classes such as call money and fixed-term deposits offer you greater security.

- Take advantage of the power of compound interest and reinvest your returns to reach your financial goals more quickly.

- When investing, make sure you diversify to minimise your risk, and always take factors such as inflation and tax into account.

Living off interest: Why I make my money work for me

I have been investing for many years and, like most investors I imagine, I dream of one day being able to live off my investment income. To be precise, I would like to achieve financial freedom by 2030. That is why I invest disciplinedly every month across various asset classes, in order to grow my portfolio step by step.

A large proportion of my passive income comes from interest I earn through P2P lending. I now receive over €1,000 in passive income every month – a real milestone for me.

We’ll take a closer look below at which platforms I use for my P2P investments and why they might be of interest to you too.

Good to know:

As P2P lending carry a higher risk than call money or fixed-term deposits, I invest a maximum of 20 per cent of my total portfolio in this asset class.

All my investments are intended to help me achieve financial freedom, thereby allowing me to shape my life as I wish and decide whether and how much I want to work.

This is precisely why this concept probably appeals to so many people: rather than trading one’s time for money, when you invest, your capital works for you. And the higher the capital, the higher the resulting investment returns tend to be.

Living off interest: The best-known investment options

For most people, the dream of financial freedom is a given. However, it is when it comes to choosing the right portfolio structure that questions often arise. Which asset classes are suitable for generating regular interest income?

1. Call money

Call money is one of the most popular forms of investment and is now offered by many banks and brokers. It is one of the safest ways to invest your money and is characterised above all by the fact that the money is available on a daily basis, is covered by the deposit guarantee scheme and generally carries a lower level of risk.

The drawbacks of instant-access savings accounts are the comparatively lower interest rates that investors receive. In some years, inflation may even eat into the expected interest, leaving investors with a negative return. However, as a nest egg, it can certainly be a sensible option.

2. Fixed-term deposit

Unlike call money, which is available on a daily basis, with a fixed-term deposit the capital is invested for a fixed period. The advantages here are the high degree of predictability and the guaranteed interest you receive.

However, interest rates on fixed-term deposits are also on the lower side and are therefore only of limited use for long-term wealth accumulation and achieving financial freedom.

3. Bonds

Government or corporate bonds are fixed-income securities and offer investors predictable and fixed interest payments. The advantages of bonds lie in their very low risk of default (in the case of governments); however, the price and attractiveness of existing bonds may vary depending on the interest rate environment.

4. Peer-to-peer lending

In recent years, peer-to-peer (P2P) lending has become an increasingly popular asset class. It usually offers investors attractive interest rates, but often carries a higher level of risk than traditional asset classes such as call money or fixed-term deposits.

Popular platforms for passive income include Debitum and LANDE. Here, investors can earn up to 15 per cent and 11.2 per cent respectively on their investments.

Platforms such as Bondora and Monefit also offer investors fixed interest rates and daily payouts through their flexible products, whilst providers such as Mintos now also offer the option of investing in corporate bonds.

How much money do you need to invest to be able to live off the interest?

The question that probably interests most investors is: “How much money do I need to invest to be able to live off the interest?”. Of course, there is no one-size-fits-all answer to this question, as everyone’s standard of living is different.

That’s why the first step is to work out for yourself how much capital you need to be able to live a comfortable life on your own terms. For some, €2,000 a month is enough, whilst others need twice that amount.

Good to know:

The formula for calculating your required capital is: Required capital = desired annual income ÷ rate of return

This simple formula shows you that as your rate of return increases, the amount of capital you need decreases. When building up your wealth, it is therefore crucial to invest in high-yield asset classes if you want to live off the interest as early as possible.

The table below shows you how much capital you need for various income targets.

| Monthly income | 4% return | 6 % return | 8 % return | 10 % return |

| 500 € | 150.000 € | 100.000 € | 75.000 € | 60.000 € |

| 1.000 € | 300.000 € | 200.000 € | 150.000 € | 120.000 € |

| 1.500 € | 450.000 € | 300.000 € | 225.000 € | 180.000 € |

| 2.000 € | 600.000 € | 400.000 € | 300.000 € | 240.000 € |

| 3.000 € | 900.000 € | 600.000 € | 450.000 € | 360.000 € |

Please note that these are illustrative scenarios. Real-world market conditions are often subject to fluctuations and may therefore also result in fluctuating returns on investment.

We have created a financial freedom calculator. With this interactive financial simulation, you can find out in just a few steps when you’ll be able to live off the interest.

To do this, enter either your current assets or your desired monthly income. The calculator will then show you your passive income or how much capital you need to achieve your financial goals.

Living off interest calculator

Calculate income from capital or the required assets

💰 Capital → Income

Monthly: –

Annually: –

🎯 Income → Capital

Capital required: –

Good to know:

When planning, don’t forget to factor in inflation and tax. Both factors reduce the real purchasing power of your investment returns and should therefore be taken into account in any realistic calculation.

An exciting alternative: can you start living off interest more quickly with P2P loans?

When it comes to achieving financial freedom, P2P lending has now become an exciting addition to traditional asset classes. Compared with traditional asset classes such as call money and fixed-term deposits, which offer only low interest rates, P2P lending can generate significantly higher returns.

Many platforms even offer investors double-digit returns per year. And as we saw in the previous section, the level of return acts as a powerful lever for the capital required.

Before you start investing in P2P loans, you should bear in mind some key points and familiarise yourself with the potential risks.

What you should know about P2P lending:

- P2P loans are not a risk-free investment

- Borrowers may default

- There are platform risks

- A broad diversification is essential

Let’s take a look at three exciting P2P platforms that help me make a living from interest and could also pave the way for you to earn passive income.

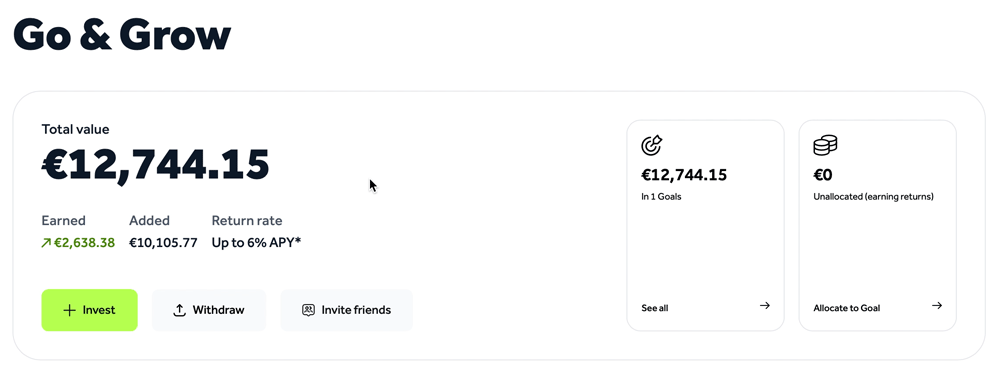

Platform 1: Go & Grow by Bondora

With Bondora’s “Go & Grow” investment product (formerly Bondora Go & Grow), investors put their money into consumer loans provided by the Bondora Group. With over 500,000 investors, Bondora is one of the market’s absolute heavyweights.

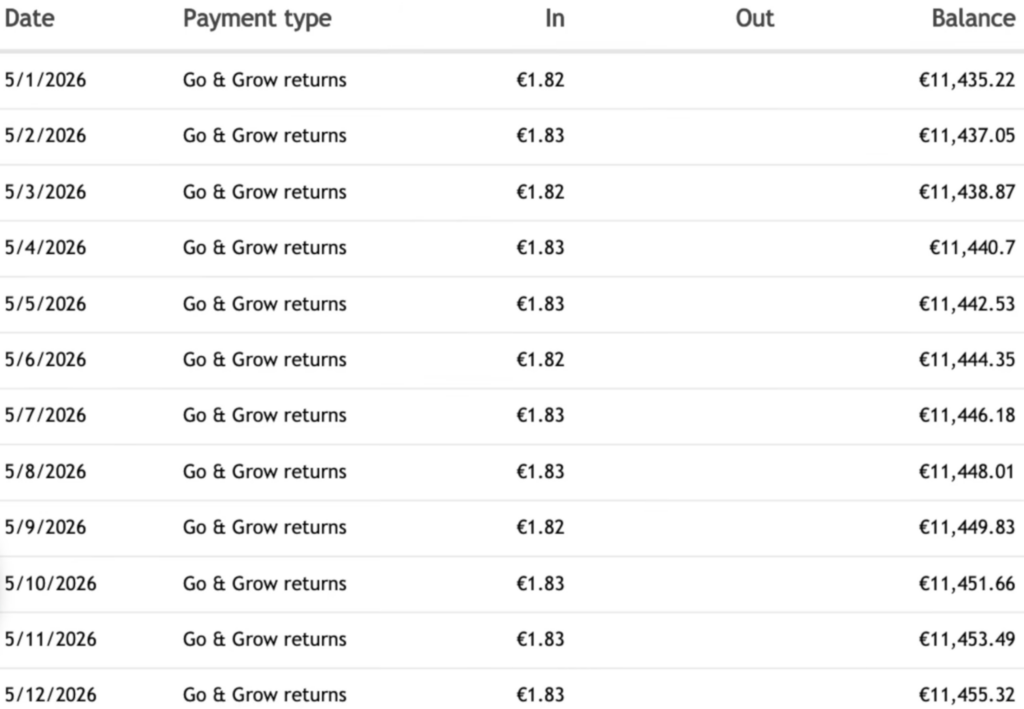

I’ve been with the platform from the very start and now have more than €11,000 in my Go & Grow portfolio.

What I particularly like about the platform is the option to withdraw my money straight away, as well as the daily interest payments I receive here. With my current investment of €11,744, I earn around €1.80 in interest every day – which is almost enough to pay for my morning cappuccino.

Although the interest rates on Go & Grow – at up to 6% per annum – are not among the highest on offer, the platform has proven itself over several years to be a robust and reliable option when it comes to P2P lending.

Go & Grow is often an attractive choice, particularly for beginners, thanks to its simple way of working, automatic investing and low minimum investment of €1.

Have a look at my Bondora review if you’d like to find out more about the platform.

If you’re looking to earn interest of up to 7.5%, Monefit could be an interesting alternative to Go & Grow. You can find out more about the platform in my Monefit review.

Platform 2: Debitum

Debitum enables investors to invest in corporate loans from various sectors, such as energy, forestry and agriculture. In return, investors receive annual interest of between 10 per cent and, for longer-term investments, up to 15 per cent.

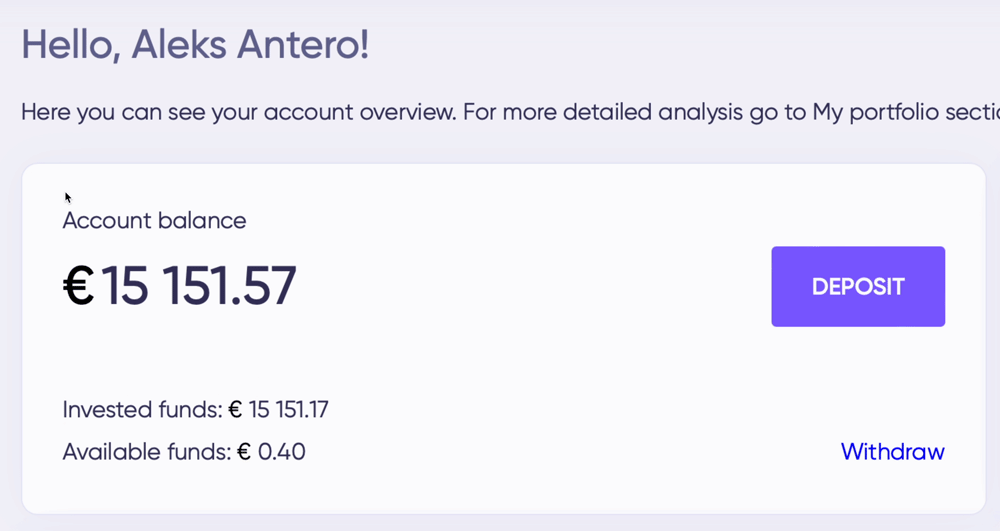

I’ve now invested over €15,000 on the platform, which earned me a tidy €170 in interest in May.

What makes Debitum so interesting is that the loans are secured against tangible assets such as woodland or machinery, which can be realised in the event of default.

Furthermore, at lender level, Debitum has a ‘skin in the game’ of between 10% and 30%. Thanks to this high proportion of capital invested by the lender itself, the lender bears a significant portion of the risk.

Have a look at my Debitum review if you’d like to find out more about the platform.

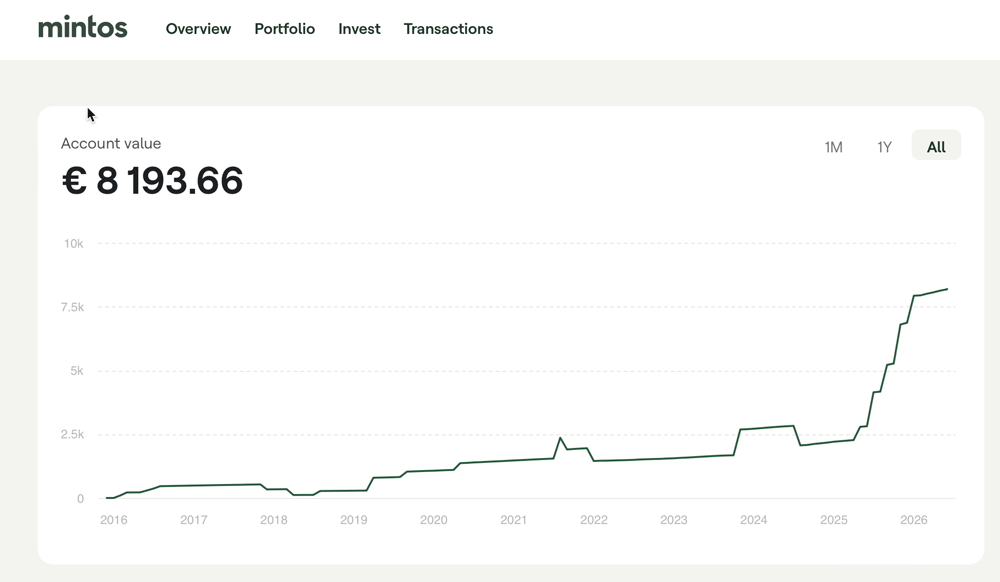

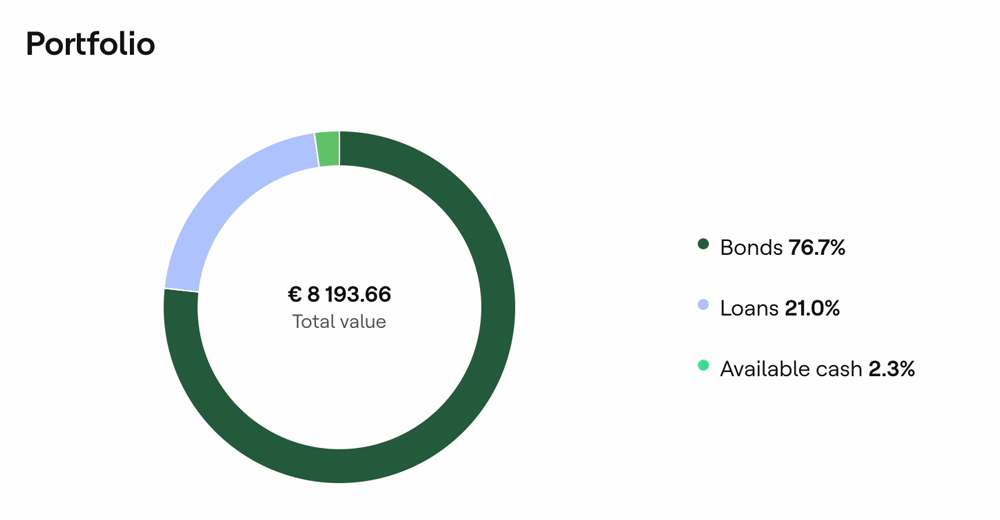

Platform 3: Mintos

Mintos is one of Europe’s leading peer-to-peer lending platforms. The company manages over 800 million euros in assets belonging to more than 600,000 registered users and has generated an average net return of 8.8% for investors since the platform was launched in 2015.

I have been investing with Mintos since 2016 and have since expanded my portfolio to just under €8,200; I am satisfied with how things have gone so far.

My focus on Mintos isn’t on traditional loans, as is the case with Bondora, amongst others, because the interest rates on these are too low and the available loans aren’t attractive enough for me.

Instead, I invest the majority in bonds – 76.7%, to be precise. For me, this is by far the more attractive option on Mintos. Although the term is usually longer here, the higher interest rate makes up for this in my view.

Have a look at my Mintos review if you’d like to find out more about the platform.

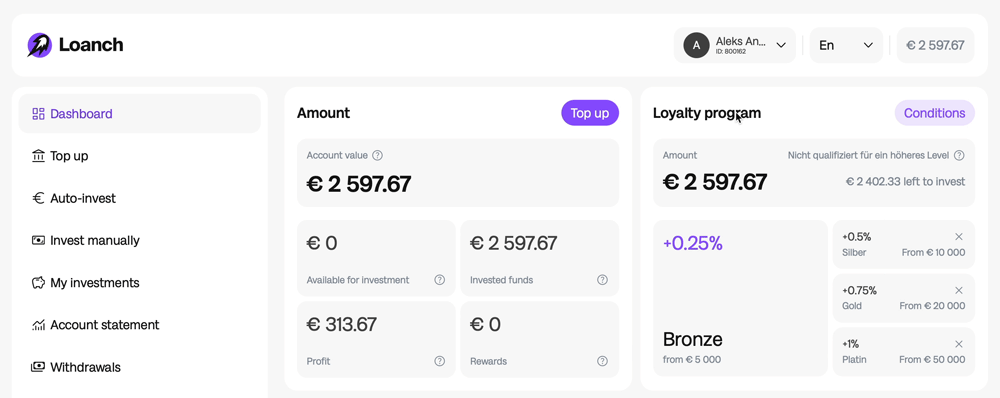

Platform 4: Loanch

Loanch is an exciting new player in the P2P lending market, which has caught my interest for some time now and prompted me to invest.

On the platform, investors invest in personal loans from South-East Asia, which currently offer interest rates of between 14.5 and 15.0 per cent. The loans are granted by the loan originator Tambadana and are in high demand: since its foundation in 2022, the platform has already attracted over 14,500 investors.

The growth speaks for itself too, as within just 12 months Loanch managed to scale its loan portfolio from around €6 million to just under €30 million!

As I’m convinced by Loanch, I’ve already invested over €2,500, which is currently earning me around €33 in interest.

Have a look at my Loanch review if you’d like to find out more about the platform.

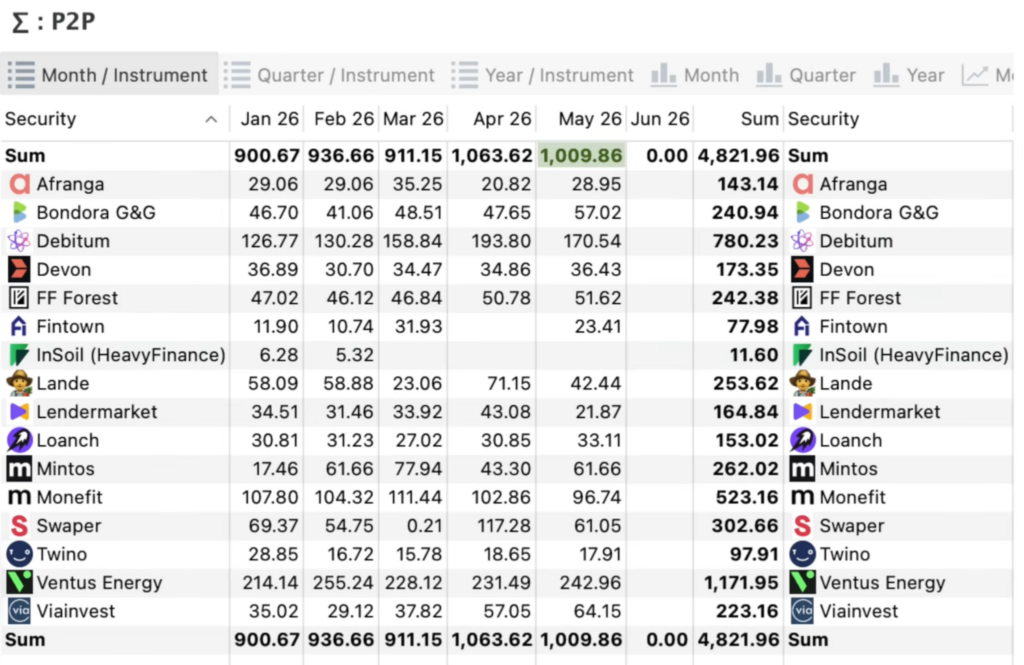

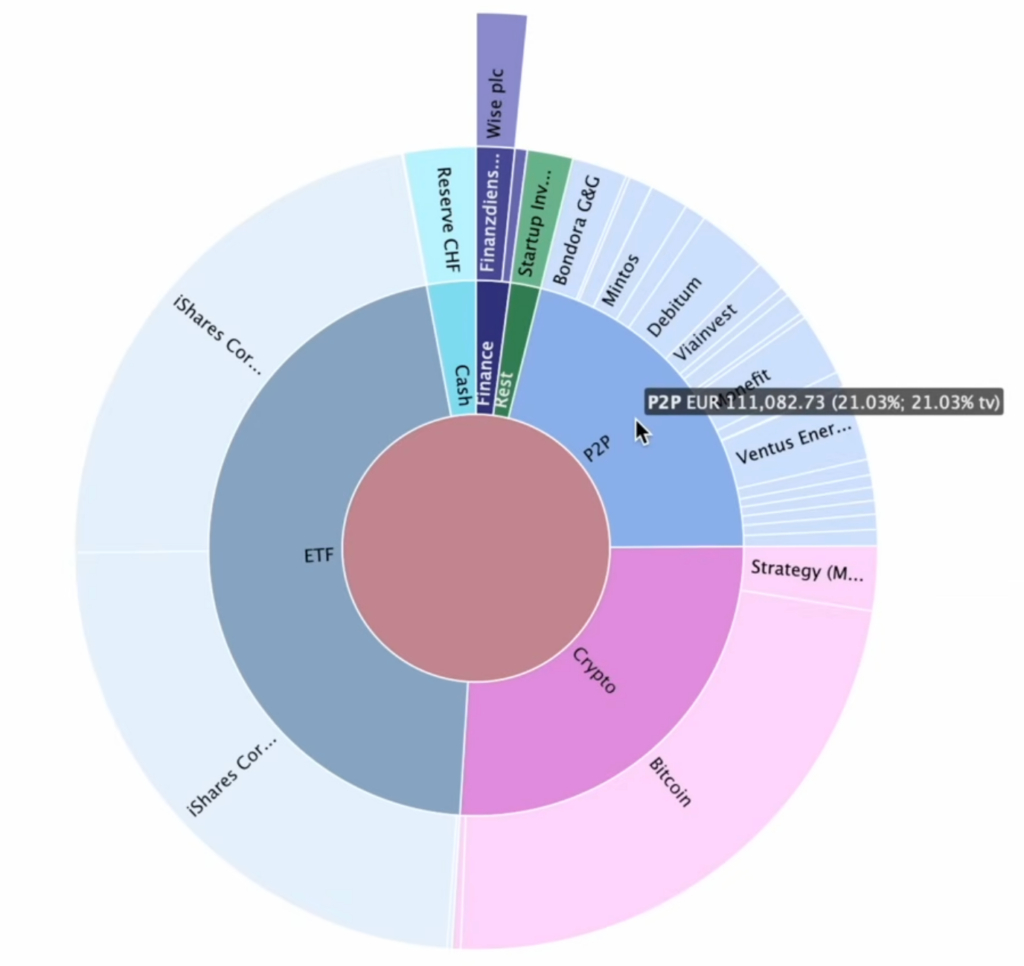

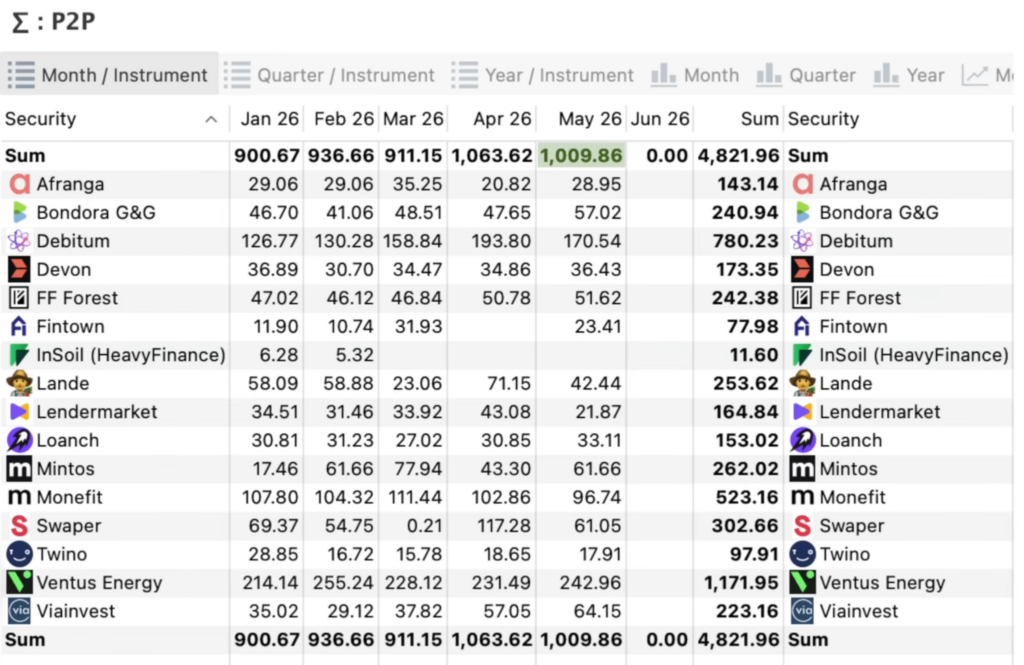

My P2P portfolio: How I earn 1,000 euros a month

I have been investing in P2P loans on various platforms for many years now and intend to continue doing so in the future. So far, my P2P investments have generated solid returns, which, thanks to the often attractive interest rates, should all help me achieve financial freedom.

I have now invested €111,000 in P2P loans. This represents around 21 per cent of my total portfolio. Thanks to this investment, I am currently able to earn more than €1,000 in interest each month without having to do anything.

The projected return this year, across all platforms, is 11.13 per cent – a performance with which I am quite satisfied.

As investing in P2P loans involves certain risks, such as loan defaults and platform risks, it is advisable not to put all your eggs in one basket, but to spread your money across different platforms.

I invest in a wide range of platforms, including:

- Bondora

- Debitum

- FF Forest

- LANDE

- Loanch

- Mintos

- Monefit

- ViaInvest

As with all asset classes, the same principle applies here: consistent investing leads to consistent wealth accumulation. I therefore discipline myself to invest a portion of my money in P2P loans every month, thereby increasing my passive income.

Here’s how you can build up passive income with P2P loans

P2P lending can be an attractive way to diversify your portfolio and boost your passive income. If you, too, would like to get started with this asset class and one day live off the interest, there are some important points to bear in mind:

- Choosing the right platform: The peer-to-peer (P2P) lending market is growing steadily. There are now a wide range of exciting providers who, as well as offering you the chance to invest in personal and business loans, also provide alternative investment options.

With LANDE, for example, you invest in agricultural loans that are secured by physical assets such as land or machinery. Mintos, amongst others, also offers investors the opportunity to invest in bonds. So make sure you get a good overview of the various platforms and choose the ones that suit you best.

- Diversify: Even within the ‘P2P lending’ asset class, you should ensure you have a broad diversification. Do not invest all your capital in a single platform, as this significantly increases the risk of default should any difficulties arise.

- Reinvesting: The effect of compound interest is like a snowball – once it starts rolling, it gets bigger and bigger. Reinvest your interest to benefit from this effect and help your wealth grow faster.

- Auto-Invest: Many P2P platforms offer an Auto-Invest feature that allows you to invest your money automatically according to criteria you set yourself. This makes it easier for you to diversify your portfolio and also saves you valuable time in the process.

- Term: Shorter terms give you greater flexibility, whilst with longer terms your capital is tied up for a longer period.

- Safeguards: The safeguards designed to give investors greater certainty when investing and to boost confidence in the platform include, for example, buy-back guarantees, the company’s track record, regulation and transparency, such as through the publication of annual reports.

- Start small: If P2P lending is new to you, it makes sense to start small at first to get a feel for the different platforms. On most platforms, you can start with as little as €1–10.

Common mistakes when investing

When investing in P2P loans, there are also common mistakes that can cost investors valuable returns. Avoid these from the outset to get the most out of your investments:

- No clear objectives: Investors who do not set clear objectives for their investments are investing haphazardly. Before you start, you should be clear about how much interest income you want to earn, how much capital you wish to invest in which asset class or platform, and for how long this capital should be tied up.

- Lack of diversification: The more capital you have tied up on a single platform, the higher the risk of default. It is better to invest across different platforms, loan types and markets to minimise your risk.

- Ignoring inflation: Not all interest rates are the same. Platforms often advertise attractive interest rates of, say, 10 per cent. However, investors often forget that this is not the real interest rate. To calculate your actual interest income more accurately, you should always take inflation into account.

With inflation at 2%, an interest rate of 10% would give you an 8% increase in purchasing power.

- Don’t forget about tax: income from P2P loans is also subject to tax. Remember to pay this on time if the platform does not do so automatically for you (which is the case with most foreign platforms).

- Don’t let your emotions dictate your decisions: always keep a cool head when investing. Investors who invest rationally and do not allow themselves to be thrown off balance by short-term fluctuations are more successful in the long term. Stay patient and consistent.

Conclusion: Making a living from interest with the right strategy

Many investors dream of being able to live off the interest and no longer having to work actively to earn their money. At first glance, this may sound like a distant, unattainable goal – and with the wrong strategy, it certainly is.

To turn the dream of financial freedom into reality, it is crucial to invest in asset classes that offer high returns. Personally, in addition to traditional ETFs and individual shares, I am increasingly turning to P2P lending for this purpose.

Investors wishing to include P2P loans in their portfolio to further diversify it should familiarise themselves with the features of the various platforms.

But the same applies here: financial freedom is not a sprint, but a marathon. Set clear goals, think long-term and consistently reinvest your returns to build up your wealth and be able to live off the interest in the future.

Take a look at my latest P2P lending ranking to find out more about the individual platforms.

FAQ: How much money do you need to invest to be able to live off the interest?