The best investment for retirement: a guide for 2026

Are you looking for the right types of investment for your retirement, or would you like to invest your money for your children? If you are looking for the best investment for pensioners, there are a few special considerations you should bear in mind when investing.

In brief:

- Around 22% of the German population are pensioners (over 65 years of age). This makes them one of the largest population groups.

- On average, pensioners receive a pension of €1,430, while female pensioners receive even less, at around €1,110.

- In 2021, almost 600,000 pensioners received basic income support, meaning that their normal pension was far from sufficient and they were dependent on state assistance.

(Source: Statistisches Bundesamt)

Difference between financial investments for pensioners and other age groups

As you can see, the situation for pensioners is rather dire. People who have had to work for decades are now partly dependent on social benefits in order to survive.

The main reason for this alarming picture is demographic change. The population is ageing. Young people are moving abroad, many parents are deciding against having children, and the birth rate is falling.

As a result, the number of contributors to the old-age pension is no longer in a healthy ratio to the number of recipients of this old-age pension. While in 1962 there were still 6 contributors for every recipient of old-age pensions, by 2020 this figure had fallen to just 1.8.

Source: Statista

Your retirement provision is in your hands. You cannot really rely on your pension. Even in old age, you should invest so that you can look forward to your twilight years with peace of mind and serenity.

Many older people know this. However, they are not familiar enough with the right investment models to invest their money wisely.

What pensioners should bear in mind before investing money

Retirement brings new challenges for older people. Their usual salary is drastically reduced, while the cost of living remains almost the same. Outstanding loans remain valid and continue to run as usual even after retirement.

What can help you now is to keep a close eye on your income and expenditure. Take a close look at your monthly costs and what you will have available after you retire. This data will give you a very good idea of how much money you have available to invest.

Normally, it is always advisable to invest around 10-20% of your income. However, these are exceptional circumstances. The most important thing is to ensure that you can cover your monthly expenses.

Secondly, you should build up a nest egg. Even in old age, unforeseen expenses can always arise, such as a broken television or a faulty car. To ensure you are prepared for these expenses, you should first build up a nest egg.

Once you have built up your reserves, you can start building your wealth.

In the following article, we will focus exclusively on savings plans. These allow you to invest a fixed monthly amount on a fixed date. Each of the following options we present to you is geared towards savings plans. This means that you do not have to invest a large sum of money at the outset, but can start by investing smaller monthly amounts.

Attention:

If you have saved up for something or need the money for something else, leave it alone and use it for its intended purpose.

These goals could be useful for pensioners

In fact, your goals as a pensioner are not so different from the goals of general wealth accumulation. Even if you are already a bit older, you can still achieve 10-year goals.

- Consider carefully before deciding on an investment method; these investments are often long-term, and you should be able and willing to save regularly for a long period of time.

If you really like two or three options, make a note of them and research them again separately. Or take a look at our blog, where you will also find what you are looking for! Trust in the respective asset class is particularly important for pensioners. And you can only build trust if you understand it 100%.

Investing is also a matter of personal preference. Are you more risk-averse or risk-seeking? Do you already have previous experience, or are you completely unfamiliar with a particular topic? All of these can and should be factors that influence your decision.

However, low-risk alternatives are generally recommended for older people. These cause less excitement for many pensioners and generally provide more stability.

When choosing your investment later on, you should definitely not ignore your personal feelings and experiences! Think about your long-term goal here too. Would you prefer stable wealth accumulation or a thirteenth annual pension?

These investments are suitable for pensioners

You have probably heard something about the possible introduction of a statutory share-based pension. According to the Federal Government, the taxes paid by the working population are to be invested in shares, the profits from which will be used to supplement pensions.

Many older people were critical of the planned project. Their mistrust stemmed primarily from ignorance. Many pensioners do not follow the current stock market or understand many of the new forms of investment.

However, if you take a look at the statistics for investment products by age group, you will see that shares and investment funds are not really the number one choice for any demographic group. Instead, savings accounts remain highly sought after.

Source: Statista

Are instant access savings accounts and fixed-term deposits still relevant?

Compared to ETFs and shares, savings accounts perform relatively poorly, yet at first glance they seem like the perfect asset class for pensioners. We are talking about bank deposits in the form of instant access accounts or savings accounts.

They offer a high level of security thanks to a fixed payment schedule and require little administrative work. Older people can go to their local bank, which they have trusted for years.

However, savings accounts have not really performed at a high level in recent years and months. Returns are low due to low interest rates. The returns offered by banks are so low that they cannot even offset current inflation.

| Advantages of a savings account | Disadvantages of savings accounts |

| Fixed interest rates and expected amounts | In some cases, very low discount rates, resulting in a relatively low final amount |

| Independent of economic influences | Very inflexible – early exit sometimes not possible/sensible and no response to market changes |

| “Traditional” banks versus neo-brokers | Depending on the bank where the savings plan is held – consider the risk of insolvency. |

This asset class is certainly one of the safest, but not necessarily the best in the long term. However, if security is important to you or you want to build up a nest egg that you need to access every day, this asset class could be an option.

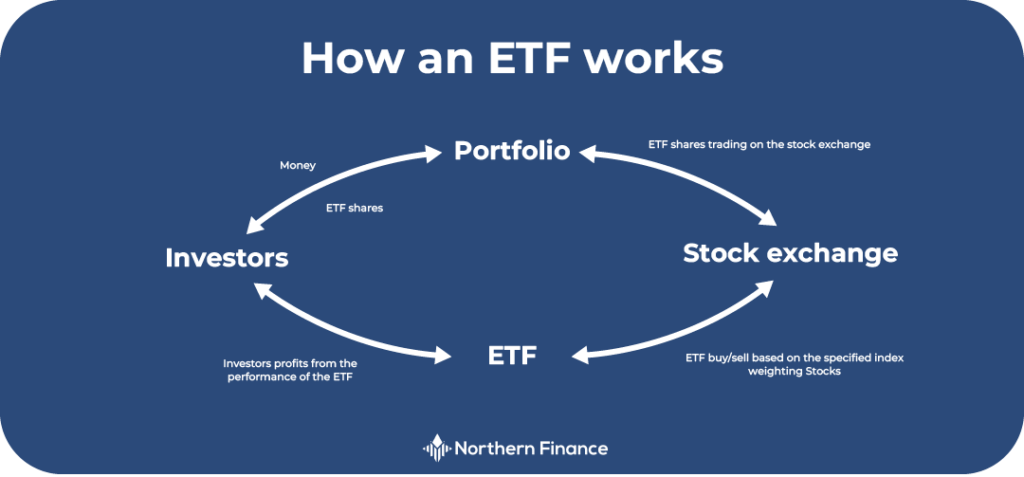

ETF savings plans as the preferred option

As you have already noticed, there are many reasons to invest in shares. However, since your risk is far too high with individual shares, as you are dependent on just one company, you should diversify your portfolio. You can do this with a so-called fund. You can think of this as a large pot into which you throw your monthly sum, and the fund invests your investment in various shares and/or assets.

You should distinguish between actively and passively managed funds. The asset class that will bring you the greatest profit is passively managed funds, also known as ETFs (if you would like to learn more about ETFs, read our ETFs for Beginners Guide).

ETFs are particularly attractive due to their low costs and high returns, averaging 8% per annum. In addition, your investment is automatically diversified.

When considering an ETF savings plan for retirement, you should take into account the respective fluctuations of the index. In order to represent a sound investment for pensioners, it is important that the relevant shares or equity funds exhibit only minor fluctuations over the course of the year.

This reduces the chances of high returns, but at the same time also reduces the risk appetite of the investment. In addition, you should refrain from investing a large portion of your assets in a single stock. This increases the chances of suffering heavy losses in the event of poor economic performance.

P2P lending as a useful supplement

If you are a pensioner and would like to try something new, so-called P2P lending could be an option. These are essentially private loans that you can participate in via certain portals.

The biggest advantage and also the main argument in favour of this asset class is the high returns. On average, investors can expect a profit of 10 to 15%. What is particularly interesting for older people is the short average investment period for P2P loans.

Most P2P lending deals only run for a few months and are then repaid to investors. This is an advantage if the expected time frame in which you can invest as a pensioner is rather limited.

Follow these steps to make your own investment

Many older people often don’t know where to start and end up not doing anything at all. That’s why we’ve put together a short checklist on how to make your first investment.

1. Selecting the right investment

We have already discussed several investments that are suitable for pensioners. ETFs are at the forefront of these. They enable older people to build up a highly diversified portfolio with little effort. Among other things, low costs ensure high returns. Volatile ETFs that offer a high level of security are suitable for pensioners.

2. Select a suitable provider

In our comparison of Scalable Capital vs. Trade Republic, we compared the two largest neo-brokers. You can often use these to purchase the right ETF for you at low cost. Setting up an account is so easy that even older people have no problem doing so.

| Freedom24 | Scalable Capital | Trade Republic | |

| Custody management | free of charge | free of charge | free of charge |

| Order fees | € 2 + € 0,02 (per share) | Gettext € 0,99; XETRA € 3,99 0,01 % (min. € 1,50) | LS Exchange 1 € |

| ETF and share savings plans | not possible | free of charge | free of charge |

| Number of shares | 40.000 | 8.000 | 9.000 |

| Number of ETFs | 1.500 | 2.500 | 2.400 |

| Number of ETF savings plans | 0 | 2.500 | 1.900 |

| Starting bonus | Bonus Freedom24 Free shares worth €79 – €529 (until 30.04.2026) | Bonus Scalable capital No bonus currently available | Bonus Trade republic No bonus currently available |

| Review | Freedom 24 | Scalable capital | Trade Republic |

Which of the three brokers you ultimately choose depends on your preferences. Personally, I prefer Freedom24 because this broker offers me the widest selection of trading venues at very low costs.

3. Be brave and invest

At the end, all you have to do is press the ‘Invest’ button. For many pensioners and older people, however, this is the biggest hurdle. The fear of unfamiliar asset classes and possible financial loss is too great.

But let’s put it this way: if the money remains in the bank, it will lose value faster than most ETFs would due to rising living costs and inflation.

Conclusion: ETFs should also be the instrument of choice for pensioners

Asset classes such as ETFs or P2P lending have not yet entered the minds of many older people. Instead of traditional savings accounts or other bank accounts, these asset classes offer comparatively high returns and low costs. The biggest hurdle is the mindset of pensioners, who are often too concerned with security.

There is no question that such an investment is worthwhile. Pensions are dwindling and inflation is rising. Everything except private pension provision seems to be a viable option. Would you like to learn more about finance? Read our articles on ‘money investment ideas’ and become a financial expert.

FAQ – Frequently asked questions: the best investment for retirement