Investing for your child: How to secure your loved one’s future

From nutrition to education and upbringing: as a parent, you naturally want only the best for your child or children, so that they can get off to a successful start in life. However, a successful future also involves choosing the right investment for your child. In Germany in particular, this important aspect is often overlooked.

In this article, we’ll tell you everything you need to know about building wealth for children – from savings plans and savings accounts to the most relevant providers with whom you can kick-start your child’s investment journey. So that you can secure your child’s financial future today.

In brief:

- The earlier parents start investing for their children, the more they will benefit from the effect of compound interest

- Savings accounts and savings plans are not suitable for building up wealth due to their low interest rates

- Regular saving through a savings plan is often the best way to lay the financial foundations for your children

- How much you should invest each month depends on your individual investment goals – neobrokers allow you to save from as little as €1

Investing for your child: Why the days of the piggy bank are over

We’ve all seen the picture: the lovingly filled piggy bank in the child’s bedroom, fed with coins from Grandma and Grandad. It’s a lovely idea for children to save, but in times of low interest rates and rising inflation, the traditional piggy bank is no longer nearly enough to secure the little ones’ financial future in the long term.

Investing for your child is more important today than ever before and offers the chance to give your children a decisive head start in adult life.

Parents who start investing for their child early on can make a big difference even with small sums: whether it’s funding a driving licence, a degree abroad or even their first home at a young age, setting up a investment account for children can pay off in the long term.

The reason for this is the compound interest effect, which is often described as the eighth wonder of the world. Parents who start investing for their children early on benefit from the power of this effect over the decades and can thus turn small amounts into a considerable fortune.

Good to know:

The compound interest effect refers to the process whereby interest that has already accrued is added to the principal and, in subsequent periods, generates interest of its own, resulting in exponential growth of the principal. Initially, the effect appears small, but over time the growth accelerates sharply; time is therefore the most important factor.

In the following sections, we’ll look at the best ways to invest child benefit, from savings plans for children to savings accounts for children, and highlight which providers offer the most attractive options.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Want to save for your children? Clarify these 5 important questions first

Before you start investing for your child, you should clarify these 5 important questions in advance to ensure you find the right investment strategy:

- What is the investment horizon?

- What is the specific investment objective?

- How high is your risk tolerance?

- How regularly should you invest?

- What should the legal structure be?

First of all, let’s consider the question of the investment horizon: how long can the money remain invested? As mentioned above, a long-term investment horizon is worthwhile due to the effect of compound interest. The sooner you set up a savings plan for your children, the more grateful they’ll be to you later on.

It is therefore advisable to set up a investment account for children as soon as they are born. For a newborn, an investment horizon of 15 to 20 years would therefore be realistic. Over this period, market fluctuations can usually be weathered without any problems.

Next, the question of the investment objective should be clarified. What will the capital be used for later on? Is it for their education, a driving licence, or perhaps even their first home? The more precisely this objective is defined, the easier it is to determine the appropriate asset allocation.

Another important point to consider with any investment is your risk tolerance. If you wish to set up an investment account for children, you should be aware of the level of risk that you – and, later on, your child – are willing to take. This is because, even during periods of significant volatility, you should continue to invest with discipline and avoid selling out of panic.

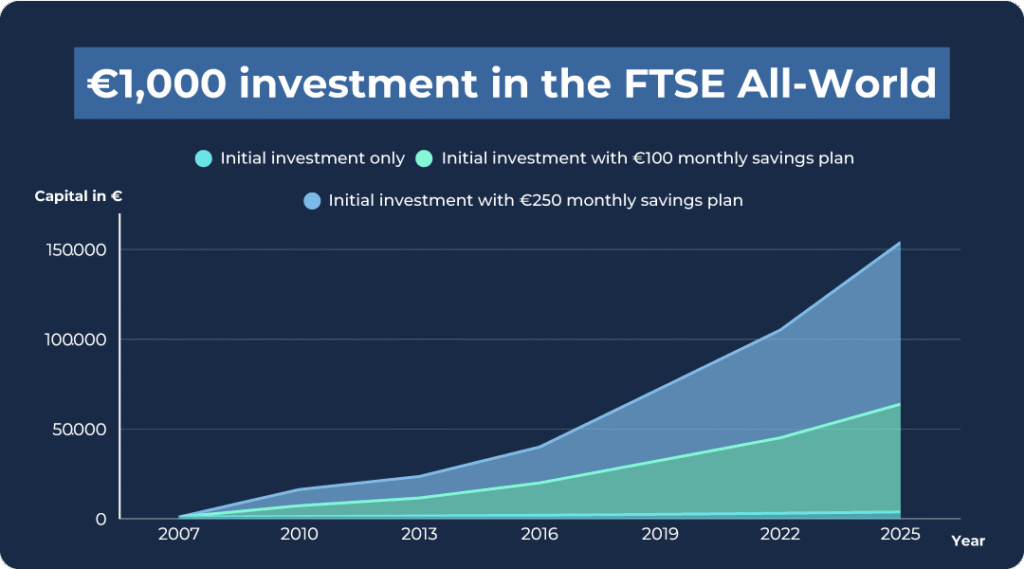

You should also clarify in advance the amount of the investments and the frequency of the contributions. A one-off investment, or perhaps a savings plan for children? The following chart from Vanguard shows that regular contributions certainly pay off in the long term.

As you are investing on behalf of someone else – your child – rather than for yourself, you should clarify the legal structure in advance. Is the money held in your child’s name or in yours? And who has the right to access it?

By answering these questions, you’ll provide clarity for yourself and your loved ones and avoid potential conflicts in the future.

Investing for your child: What is the best investment for a child?

There are several ways to invest money for your children. However, not every option is truly attractive when you take inflation, costs and potential returns into account.

That’s why it’s worth comparing the most common options in more detail, rather than relying solely on supposedly ‘safe’ traditional choices. Below, we look at three forms of investment that are particularly popular for children:

- The savings account: The traditional, very safe form of investment with funds available at any time, but usually offering very low interest rates.

- The savings plan: For investing small amounts regularly (e.g. monthly), often in funds or ETFs.

- The savings agreement: A contractually agreed form of saving with fixed terms and conditions (e.g. a bank savings plan or a building society savings agreement).

In doing so, we examine not only the typical expected returns and the respective risks, but also the cost structure of the individual options.

This is because fees and inflation, in particular, have a decisive influence on how much of the money saved actually remains in the end.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Investing for Child 1: The savings book

In Germany, both the savings book and the instant-access current account remain among the most popular forms of investment when parents want to save for their children.

One reason for this is certainly the simplicity of the products. They are easy to understand and the capital is available at any time.

However, neither savings accounts nor instant-access current accounts are attractive forms of investment. The problem is that interest rates are often significantly below the rate of inflation, which means that the money invested effectively loses purchasing power.

The following chart shows the trend in the average interest rate on savings deposits in Germany, from which it is immediately apparent that saving has become increasingly unattractive over the years.

For this reason, a savings account cannot be regarded as the best way to invest in children’s benefits. Parents who are not only saving for their children but also wish to build up long-term wealth should therefore look for more attractive investment options.

Investment option for children 2: The savings plan

Savings plans for children are becoming increasingly popular. They are among the most effective methods for systematically building up wealth for oneself and one’s children, which is why we are taking a closer look at this form of investment.

The way a savings plan works is simple: parents choose an amount to be invested monthly in selected investment vehicles. These usually include investing in ETFs.

Advantages of savings plans for children:

- Regularity: Automated payments ensure continuous growth.

- Cost-averaging effect: By buying at different market stages (sometimes at higher prices, sometimes at lower prices), the average purchase price is optimised.

- Flexibility: Savings instalments can often be adjusted or paused. One-off payments can also be made.

- Low barriers to entry: Many brokers offer savings plans starting from as little as €1 per month.

ETF savings plans, in particular, are becoming increasingly popular in Germany, including via ETF pension schemes. They enable low-cost, passive investment in broadly diversified indices, thereby significantly reducing the risk of a total loss on ETFs.

Good to know:

The MSCI World is one of the most popular indices; it invests in around 1,500 companies from 23 developed countries and reduces the risk for investors through its broad diversification.

Individual shares may offer high returns, but they also carry a significantly higher risk and require more expertise and time to select. For long-term investments for children, a passive ETF strategy is often the best choice.

To start investing via a savings plan, parents need to set up a custody account for their children. This is a simple but important step towards getting started with investing for children.

Some brokers now offer attractive children’s investment accounts to help parents save for their children. We’ll look at potential providers in detail later on.

Investing for children 3: The savings agreement

The term ‘savings agreement for children’ is often used interchangeably with the savings plan discussed above. However, there are clear differences between the two, and a clear recommendation for parents when it comes to the best way to invest for their children.

Savings agreements are fixed-term savings schemes in which, much like a savings plan, specific amounts are paid in regularly. Classic examples of such savings agreements include bank savings plans or building society savings agreements.

The major advantage of savings agreements for children lies in their predictability. Thanks to their fixed term and savings rate, parents know exactly how their children’s capital will grow.

Good to know:

For parents who have clear investment goals – such as saving for a driving licence or a course of study abroad – savings plans can therefore be a sensible option. They also offer the security of not being affected by fluctuations in the capital market.

The major disadvantage of savings plans for children: the returns and interest rates. The returns on such products are often limited and frequently only slightly higher than the interest rates on a savings account. This also means that, in times of high inflation, purchasing power ultimately declines.

Savings plans are also limited in terms of flexibility, as early termination often entails financial penalties. The question of whether to choose a building society savings plan or an ETF can therefore, in many cases, be answered with “ETF”.

Setting up a custody account for children: a look at providers

Once the decision has been made to start investing for a child, the next crucial step in effectively beginning to build up their wealth is: choosing the right investment account.

Many banks and brokers now offer children’s investment accounts to parents. Traditional providers include banks such as Sparkasse, Commerzbank, DKB and ING.

Through these, parents can set up a custody account for their children, with the child listed as the account holder from the outset. Parents manage the account until their child reaches the age of majority.

Advantages of opening a custody account through a traditional bank:

- face-to-face advice in branch

- often well-established infrastructure

Disadvantages of opening a custody account through a traditional bank:

- higher costs for account management and the execution of savings plans

- often a limited selection of free ETF savings plans

As traditional banks are often more expensive and offer fewer options, neobrokers have become increasingly established in Germany over recent years. They stand out thanks to their cost-effective structure and accessible products.

Below, we present two established neobrokers where parents can set up a custody account for their children: Trade Republic and Scalable Capital.

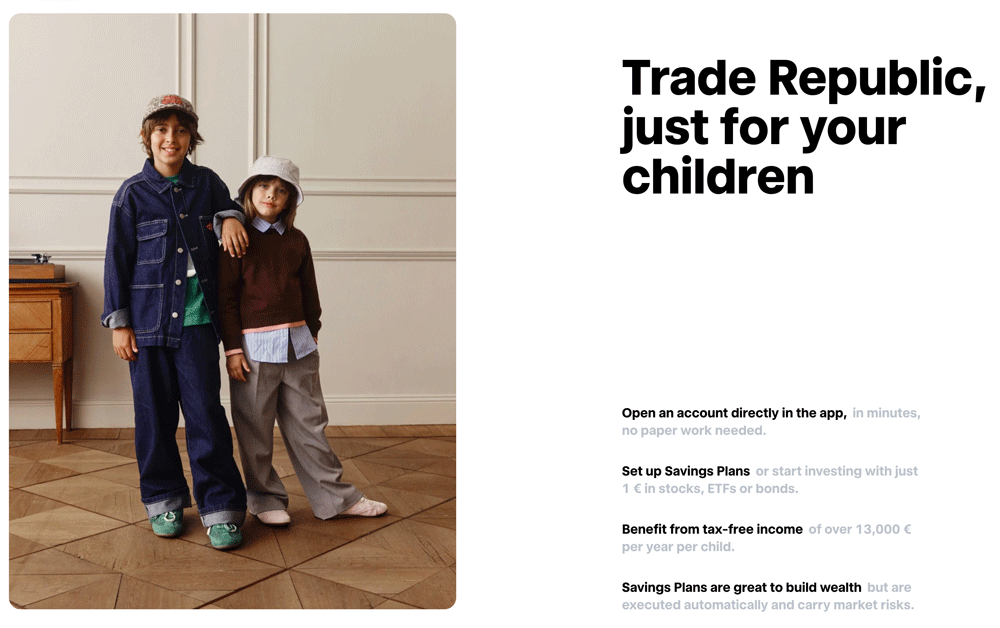

Setting up a custody account for children: Trade Republic

With Trade Republic, parents can set up a children’s custody account for their offspring, which is held in the child’s name and becomes their full property as soon as they turn 18.

Parents benefit from Trade Republic’s familiar user-friendliness and tried-and-tested savings features, and can take advantage of up to €13,000 of tax-free investment income per year per child.

How to open a custody account:

- Opening an account via the Trade Republic app

- You will need the child’s birth certificate and the consent of the other parent (unless you have sole custody)

- Both parents must have an account with Trade Republic

- A separate custody account can be opened for each child until they reach the age of 17.5

Savings plans can be set up as usual from a savings amount of just €1 and paused at any time. In addition, Trade Republic offers a feature allowing family and friends to save for your child.

Another special feature is Trade Republic’s child benefit. Under this scheme, the ongoing fund costs of selected Vanguard ETFs are reinvested into the ETF on a monthly basis. This is intended to further support the child’s future.

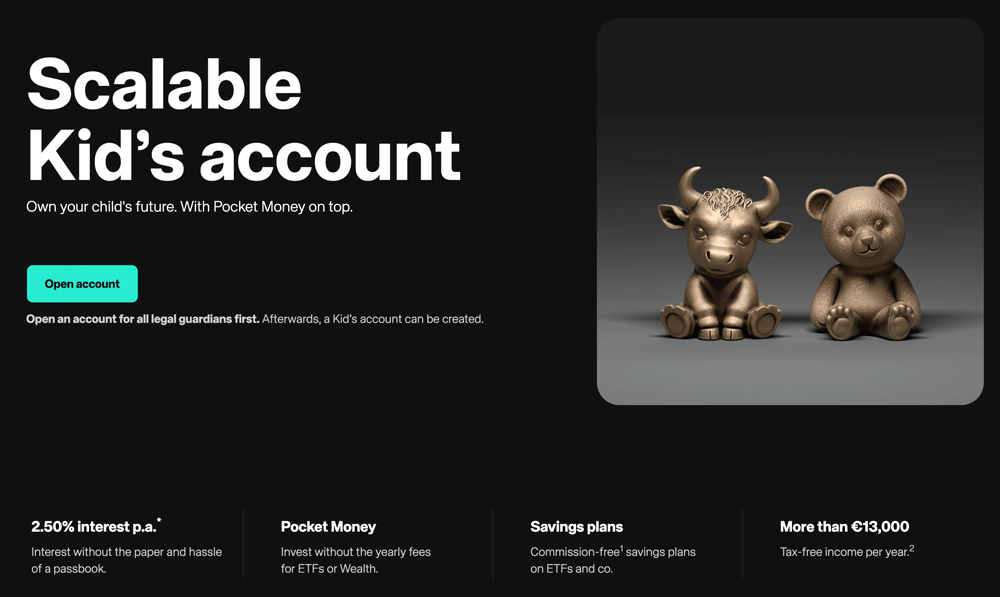

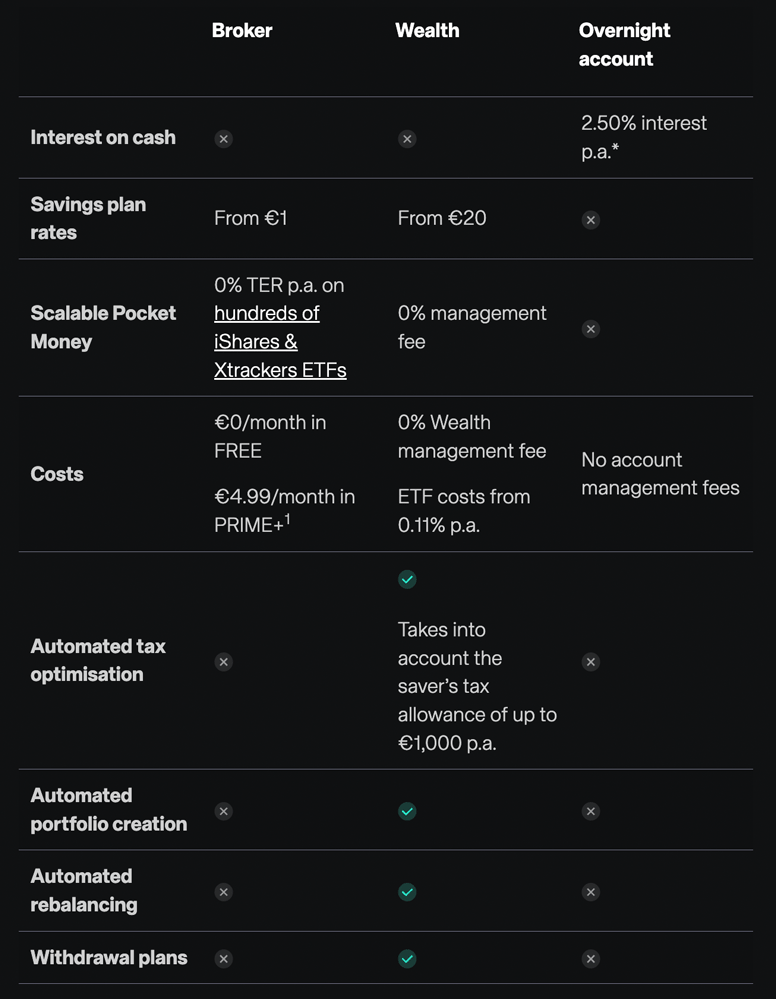

Opening a custody account for children: Scalable Capital

Alongside Trade Republic, Scalable Capital is one of the established neo-brokers in Germany. Here, too, parents have the option of opening a custody account for their children.

There are three different products for parents to choose from:

- Broker

- Wealth

- Call money

With Broker, just like with Trade Republic, you can save from as little as €1 a month, whereas with Wealth the minimum is €20. However, Wealth automatically takes into account the saver’s allowance of up to €1,000 per year, which reduces the administrative burden. More d

Scalable Capital offers the pocket money feature. Here, too, the product costs (TER) of selected savings plans are reinvested, meaning that, on average, up to €320 in pocket money can be saved by the time the child reaches the age of majority.

In addition, there is also the option to invite friends and family to help save for your own child. The “Savings Mentor” feature works without any minimum amount, or you can set up a standing order.

Setting up a investment account for children: Alternative ways to achieve investment goals quickly

As well as savings plans for children through traditional banks or neobrokers, parents with a higher risk appetite also have the option of reaching their children’s investment goals more quickly. We’re presenting two exciting alternatives for this: the P2P lending platforms Go & Grow and Monefit.

With both Go & Grow and Monefit, the money for your child is invested in consumer loans. With Go & Grow, these are loans from the Bondora Group, whilst with Monefit they are loans from Creditstar.

Investors currently have the opportunity to earn 6% per annum with Go & Grow and 7.5–10% per annum with Monefit. For many, P2P loans are therefore a worthwhile option in times of high inflation.

Good to know:

P2P investments are riskier than traditional forms of saving, as borrowers may default and there is no deposit protection. Furthermore, your investment also depends on the stability of the platform.

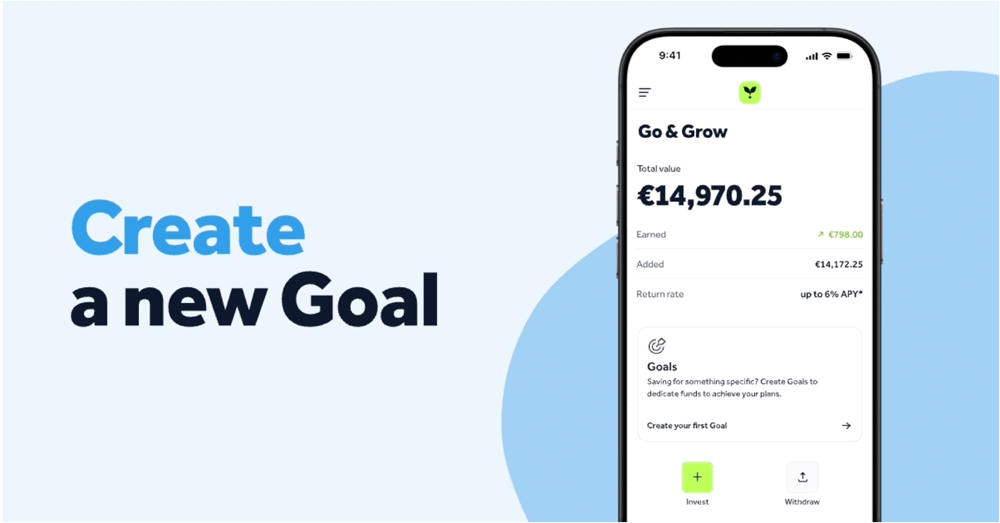

In particular, the new “Goals” feature from Go & Grow could be of interest to parents who want to bring structure, motivation and clarity to their child’s saving process.

Parents can set up individual savings goals for each child, whether it’s a driving licence, a university degree or a deposit for their first home. These can be specified in detail on the platform, which makes them feel much more tangible.

For each of these goals, an individual amount can be set and progress tracked at any time. This makes saving more structured and much better planned.

Another advantage is the flexibility: money can be moved between different goals at any time should priorities change, for example if higher education costs suddenly arise or a goal needs to be achieved sooner.

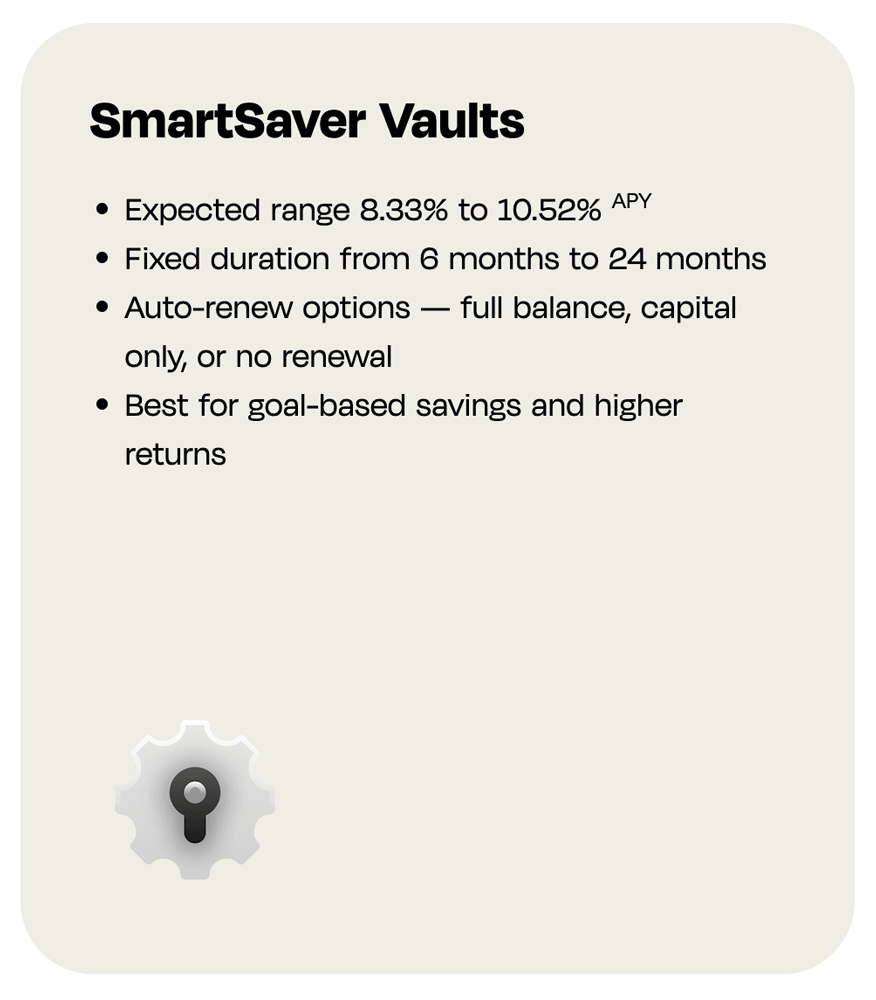

The P2P lending platform Monefit is also an exciting option when it comes to saving for children with higher returns.

With Monefit, parents have the option of parking the money in so-called ‘vaults’ for a term of 6 to 24 months. The money is therefore unavailable for this period, for which parents or the child are rewarded with a higher return of up to 10.5%.

The vaults can also be named, which makes the investment objectives more tangible. Furthermore, choosing a payout date helps with planning, which is another important aspect of investing for children.

Conclusion: Securing your child’s financial future with the right investment

Most parents know that financial provision for children is essential. However, when it comes to the question of the best investment for children, most are still in the dark. Savings accounts and savings plans are no longer attractive investment options due to their low interest rates. Savings plans, on the other hand, have become a favourite investment option in recent years.

They are designed for long-term wealth accumulation and can be set up in just a few simple steps. In particular, neo-brokers such as Trade Republic or Scalable Capital offer low barriers to entry and attractive features that make saving for children easier and help them achieve their investment goals.

When it comes to investing for children, P2P lending platforms can also offer exciting alternatives.

FAQ – Frequently asked questions about investing money for children