Investment opportunities for expats: Investing successfully in 2026

Are you planning to move abroad and want to build a secure financial foundation there? Even though many expats often earn a good income, rising living costs and expenses in popular destinations mean that your financial breathing space can quickly shrink.

Below, you’ll find out how you can build wealth step by step with a well-thought-out investment strategy and secure long-term financial freedom abroad through targeted investments.

In brief:

- Your income abroad provides a solid foundation, but the best way to build real wealth is through targeted investments.

- With ETFs, you can build up your capital over the long term and benefit from stable potential returns with manageable risk.

- P2P loans offer you regular interest income and provide an additional source of income.

Why financial investments are so important for expats

Many expats are deeply immersed in their daily lives, whether it be building a new life abroad, fulfilling professional commitments or adapting to a different culture.

This often leaves little time for personal financial planning. However, building wealth abroad also requires a clear structure, careful planning and a forward-looking strategy to secure long-term prosperity.

If you’re focusing all your energy on your new surroundings, job or family, it’s understandable that you might put off making financial decisions or leave your money in an account that seems safe but pays hardly any interest.

However, those who take responsibility early on, develop a well-thought-out investment strategy and implement it consistently will, step by step, achieve genuine financial freedom.

- A good income: This provides a solid foundation when living abroad, but you’ll only build real wealth if you invest your money wisely rather than spending it all on day-to-day expenses. Without well-thought-out investments, your financial freedom will remain limited in the long run.

- Rising living costs: Inflation means your capital loses value over time, even if your income remains stable. That is why it is important to invest your money in a way that maintains or increases its purchasing power.

- Retirement planning is essential: you cannot always rely on state pension schemes or workplace pension schemes abroad. By making private provisions early on, you can bridge any gaps in your pension provision and ensure you can maintain your current standard of living in retirement.

- Greater freedom and autonomy: Financial independence allows you to make career decisions more freely, take time off or invest in new projects and further training. Without sufficient savings, however, you often remain tied to rigid structures.

These points highlight the fact that expats should take a proactive approach to their financial planning in order to achieve long-term financial stability, security and an independent life abroad.

The power of compound interest: your strongest ally in building wealth

The effect of compound interest shows how your invested capital grows exponentially over time.

If you regularly put a portion of your income into your investment scheme for expats and reinvest both your returns and your initial capital, a process is set in motion whereby profits generate further profits. As a result, your wealth grows at an ever-increasing rate.

- Exponential growth: As returns on previous earnings are reinvested, your capital grows at an ever-increasing rate with each investment period. When it comes to investing for expats, this creates a dynamic effect that allows your wealth to grow at an ever-faster pace.

- The long-term perspective as a key to success: the longer your money remains invested, the more the power of compound interest comes into play. Time is crucial if your capital is to reach its full potential.

- Consistency makes all the difference: even small but regular deposits can add up to a considerable sum over the years. It is important not to withdraw your profits, but to reinvest them consistently.

- Returns as a catalyst: A higher rate of return greatly amplifies the effect of compound interest and leads to significantly greater wealth growth in the long term. Even small increases in returns can, over time, make the difference between average and above-average success.

Take advantage of the power of compound interest when investing as an expat to grow your capital step by step. With perseverance, discipline and a smart strategy, you can build a solid financial foundation for yourself abroad.

How exactly does the effect of compound interest work?

The money you invest generates returns, which you don’t withdraw but reinvest. This means that later on, you’ll earn interest not only on your initial capital but also on the profits you’ve already made. Over time, your wealth grows at an ever-increasing rate and your capital curve rises exponentially.

A simple example illustrates this clearly: if you invest €1,000 at an annual interest rate of 7%, you will make a profit of €70 in the first year, which you then reinvest. By the second year, €1,070 will be working for you, generating around €75 in interest. After two years, you will have around €1,144.

This snowball effect intensifies with each period: the curve becomes steeper and steeper because interest is compounded on interest.

You can think of it as an avalanche that gathers more and more momentum as it rolls, making it go faster. You make targeted use of this mechanism when investing as an expat, with the aim of growing your wealth over the long term and achieving financial freedom abroad.

Example: 7% annual return with a continuous savings plan

To illustrate just how powerful the effect of compound interest is when it comes to investing for expats, let’s consider this scenario: as an expat, you invest your capital in a broadly diversified ETF portfolio that yields an average annual return of 7%.

| Monthly amount | 5 years | 10 years | 20 years | 25 years | 30 years |

| 250 € | 17.305 € | 40.905 € | 115.674 € | 166.712 € | 235.978 € |

| 500 € | 34.610 € | 81.810 € | 231.347 € | 333.424 € | 471.956 € |

| 1.000 € | 69.220 € | 163.619 € | 462.693 € | 666.849 € | 943.912 € |

This scenario clearly illustrates the crucial role that time plays in investing.

Even if, as an expat, you only invest modest amounts each month, the combination of consistency and the power of compound interest means that your capital will grow significantly over the decades.

The sooner you start, the more you’ll benefit from your returns being reinvested, creating a real snowball effect. If you start early, you often need to set aside much smaller monthly amounts to achieve the same long-term goals.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Keep track of your spending: low fees maximise the power of compound interest

To allow the compound interest effect to work to its full potential in your investments, your capital should remain invested for a long time without any interruptions. High costs significantly offset this effect, as they continuously reduce your return.

Even seemingly small annual fees of 1 to 2% can add up to five-figure losses over the course of decades. These are deducted directly from your profits, meaning there is less capital available to generate further interest.

When choosing funds and ETFs, you should therefore deliberately opt for products with a low TER. This way, more of your returns stay in your investment portfolio instead of being eaten up by fees.

If you are planning to emigrate, it is essential to carry out a detailed cost analysis in order to make the most of the power of compound interest. Keeping your spending low makes your wealth-building more efficient and helps you reach your goals faster.

Attractive investment opportunities for expats: investing wisely and profitably

If you want to plan for your long-term future, it’s worth setting up a clear savings plan involving regular investments in ETFs and a moderate allocation to P2P loans. This allows you to combine the potential for strong returns with broad diversification of your capital.

- ETFs (Exchange-Traded Funds): They track entire market indices and benefit from overall economic growth, making them ideal for long-term wealth accumulation. With an ETF savings plan, you can diversify your investments globally with even small amounts and benefit from the price gains of many companies.

- P2P lending: Through these platforms, you lend directly to individuals or small businesses and receive regular interest payments in return. They offer higher returns but carry greater risks, such as defaults or platform issues, and should only make up a small portion of your portfolio.

The combination of ETFs as a stable foundation and P2P loans as a supplement strikes a balance between security, returns and risk diversification for expats looking to invest their money. This is how you invest your money systematically, spread the risk wisely and build up your wealth step by step for the future.

ETFs: Diversify globally and benefit from growth

Exchange-traded index funds such as the MSCI World (ISIN: IE00B4L5Y983) or the S&P 500 (ISIN: IE00B5BMR087) track entire markets. When investing as an expat, you can invest in hundreds of companies through a single product and capitalise on global economic growth.

As soon as you invest in an ETF, you indirectly become a co-owner of many companies and benefit from their long-term price appreciation.

The fund management companies take care of everything else: administration, dividend payments and regular rebalancing. It’s a simple and time-saving way to put your capital to work for you.

Example: 9% return per year with the S&P 500

The S&P 500 is one of the leading US stock indices and has delivered an average annual return of around 9% over the last two decades. When investing as an expat, choosing the right ETF means you automatically benefit from the growth of the US economy.

Why ETFs are ideal for expats:

- A solid foundation for your portfolio: despite price fluctuations, they reduce risk through broad diversification and are ideal as the core of a long-term wealth-building strategy.

- Minimal effort: use monthly savings plans. Once it’s set up, everything runs automatically without you having to track the courses.

- Wide-ranging risk diversification: Your money is spread across many regions, sectors and companies, so that losses in one area are often offset by gains elsewhere.

As you can see, ETFs offer you, as an expat, a smart and stress-free way to grow your wealth over the long term.

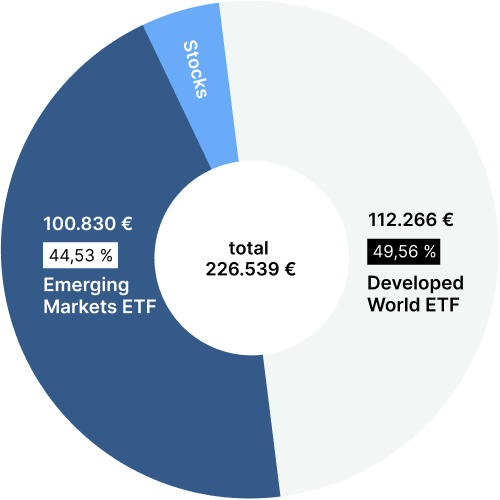

This is how I invest in ETFs with a return of around 9%

In my investment portfolio for expats, I have structured my portfolio so that around 37% is invested in ETFs tracking developed markets and around 42% in emerging markets (emerging market ETFs). This is how I capitalise on the stability of established economies and the higher growth potential of emerging markets.

Emerging market ETFs offer attractive long-term growth rates, but they are more volatile and, in my view, represent the riskier option.

I hold my investment portfolio with Scalable Capital, a neobroker offering a wide range of ETFs and fee-free savings plans. This makes my regular investing simple and cost-effective.

The intuitive app and automatic savings plans are perfect for my life as an expat with little time for active portfolio management.

This mix of developed and emerging markets strikes a balance between security and potential returns. The allocation suits my risk profile, and I’m planning for the long term.

Here’s how you could get started:

- Choose two broadly diversified global ETFs: go for one ETF covering developed markets and a second one covering emerging markets. This way, you can cover your global needs and benefit from both stability and growth.

- Set up an automatic savings plan: Set up monthly investments via a neobroker. This happens automatically in the background, so you don’t have to keep thinking about it.

- Review and rebalance annually: Check once a year to see whether your portfolio allocation still aligns with your goals. Adjust as necessary to maintain a balance between risk and return.

With this clear investment strategy for expats, you can systematically build up your wealth, spread your risks globally and achieve strong long-term returns. Simple, well-organised and hassle-free.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

P2P lending: Additional returns independent of the stock market

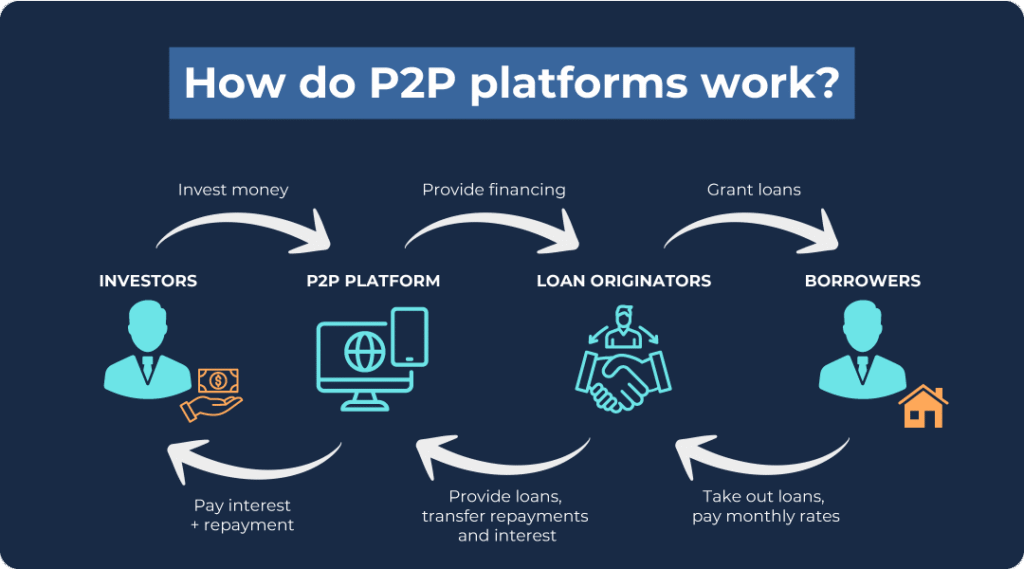

With peer-to-peer (P2P) lending, you lend your money directly to individuals or small businesses, without a bank acting as an intermediary. Through platforms such as Bondora or Mintos, you can invest as an expat and often earn higher interest rates than on traditional savings accounts.

The providers check the creditworthiness of borrowers and handle the administration and repayment process. As an investor, you will receive the agreed interest on your capital on a regular basis.

P2P lending is particularly useful for people who are looking for or wish to offer financial opportunities outside the traditional banking system.

As an expat, you can currently achieve returns of 6 to 15% per year with such investments, which is a lucrative alternative to a call money account.

How a peer-to-peer loan works in practice

- Individuals and businesses apply for loans via specialist platforms for various purposes, such as home improvements, major purchases or business investments.

- The platform then thoroughly checks the applicants’ creditworthiness and assesses the risk in order to decide whether a loan will be approved and, if so, on what terms.

- You choose how much you want to invest, and together with other investors, you finance the total loan amount.

- As soon as the borrower makes a repayment, the instalments plus the agreed interest are paid into your account on a regular and pro-rata basis.

- The platform handles all administrative tasks, the ongoing monitoring of loans and, in the event of problems, debt collection procedures.

With this investment approach, you can diversify your overall portfolio effectively when investing as an expat and benefit from steady returns that are unaffected by share prices and stock market trends.

Why P2P loans are particularly attractive to expats

- Predictable returns: On many platforms, you receive interest payments and principal repayments on a monthly or even daily basis. This provides expats with a stable, automatic source of additional income that continues to come in regardless of your job abroad.

- Independence from the stock market: Even when stock markets are sluggish or falling, P2P investments still generate regular returns. Equity portfolios often do not offer this level of consistency.

- Minimal time commitment: Automated tools such as Auto-Invest on Mintos or Go & Grow on Bondora take care of everything from loan selection to monitoring repayments. You don’t have to do anything yourself.

P2P lending is the perfect complement to your investment portfolio as an expat, providing an additional source of income and helping you to grow your wealth over the long term, particularly when combined with ETFs.

This combination helps to smooth out fluctuations in your portfolio and safeguards your financial stability as you work towards your goals.

1. Invest easily with Bondora and earn interest daily

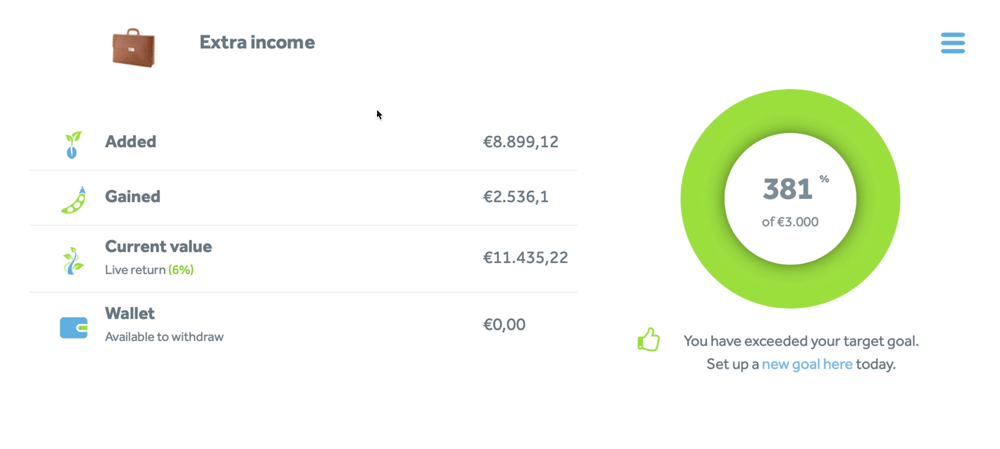

If you’re looking for a particularly simple way to grow your money when investing as an expat, Bondora’s Go & Grow is the perfect place to start.

Simply transfer your funds to the Bondora account, and the platform will automatically distribute them across a range of different loans. Here’s how you can earn interest every day with minimal effort. The current return is around 6% per year.

The benefits of Bondora at a glance:

- It’s incredibly simple: you don’t have to search for loans one by one or deal with the paperwork. Everything runs automatically in the background.

- Available for withdrawal at any time: you can withdraw your money at any time; it is usually available again after one working day.

Passive income: Interest is credited to your account every day. - Important to note: Even reputable P2P platforms such as Bondora involve risks when it comes to investing for expats. Borrowers may miss payments or default.

Good to know:

Bondora has been in business for around 17 years, has over half a million investors worldwide and has facilitated more than €1.7 billion in loans. Investors have received around €159 million in interest to date.

2. Invest flexibly with Mintos and achieve higher returns

If you’re looking to invest as an expat and want more control over your investments, Mintos offers an exciting, flexible option.

On this platform, you invest in loans to private individuals and small and medium-sized enterprises from various countries and regions. This gives you access to a wide range of different loan projects, allowing you to allocate your capital according to your preferences.

Your advantages with Mintos:

- Attractive returns: Depending on your risk appetite, you can achieve annual returns of between 6% and 15% with Mintos.

- Buyback guarantee: If a borrower defaults on payments, many lenders on the platform will buy back the loan. This gives you, as an investor, extra protection.

- Flexible control: With the Auto-Invest feature, everything runs automatically, or you can select individual loans manually if you want more control.

- Wide diversification: Spread your capital across many borrowers and countries to minimise the risk of individual defaults.

Please note, however, that some lenders have experienced problems in the past, with repayments sometimes being made only partially or late. Mintos offers a wide range of filter options, which makes the platform a little more complex but gives you plenty of freedom when it comes to your investment strategy as an expat.

3. Sustainable investments at Ventus Energy

Ventus Energy allows you to invest directly in green projects such as wind farms, solar power plants or energy storage systems as part of its investment scheme for expats. This way, you can support the transition to renewable energy whilst earning regular interest on your capital.

Your advantages at Ventus Energy:

- Lucrative returns: Annual returns of up to 17% are possible.

- Continuous interest payments: Daily credit entries amplify the effect of compound interest and promote dynamic growth.

- Transparent investments: All projects are presented clearly, with regular buy-back options to ensure flexibility.

Ventus Energy targets larger sums, with a minimum stake of usually €1,000. Investments in the energy sector fluctuate in line with market and economic conditions, which entails a risk of loss.

For you as an investor, this is a great opportunity to combine a return on investment with sustainable investing.

Ventus Energy is currently undergoing restructuring and is not accepting new investors or investments. That's why I'm investing my new funds on Monefit. As a welcome gift, you'll receive a €5 bonus + 0.75% (for 90 days).

This is what your investment could look like in 2026

In my portfolio, I carefully combine different types of investment to ensure long-term security and generate a steady additional income. You can use this approach as a template and adapt it to suit your goals. Make sure you bear the following key points in mind:

- Attractive returns with controlled risk: strike the right balance between potential returns and capital security.

- Regular income for greater independence: automated cash flows make you less reliant on your income from abroad.

- High levels of automation save time: with less manual effort required, the strategy fits seamlessly into your life.

Your exact strategy will depend on your risk tolerance and your personal circumstances. Some investors are primarily looking for stability and steady returns, whilst others are willing to take on more risk in order to achieve higher returns. There are many paths to success.

In my view, it is particularly worthwhile to opt for passive, automated systems that require little maintenance. Below are two suitable options for this.

- Conservative portfolio for security and stability

| Investment | Share in the portfolio | Goal |

| ETFs | 70 % | Long-term, stable growth |

| P2P lendings | 20 % | Regular cash flow |

| Cryptos | 5 % | Additional yield driver |

| Call money | 5 % | emergency reserve |

- Aggressive portfolio with a focus on returns

| Investment | Share in the portfolio | Goal |

| ETFs & individual shares | 50 % | Long-term, global growth |

| P2P lendings | 25 % | Regular interest income |

| Cryptos | 20 % | High potential for returns, but with higher risk |

| Call money | 5 % | Short-term reserves for emergencies |

Why this strategy makes sense for long-term investment:

- ETFs: They form the stable foundation of your investment portfolio when investing as an expat. This allows you to benefit from global economic growth in the long term, whilst managing moderate risk and typical market fluctuations.

- P2P lending: It generates additional sources of income. The regular interest payments steadily increase your available capital and provide a reliable source of income with minimal effort.

- Cryptocurrencies: This asset class is characterised by high volatility, but offers enormous growth potential and above-average returns.

- Call money: Ideal as a cash reserve if you need access to your money at short notice or want to invest it safely for a short period without being tied into a fixed term.

These investments are a perfect fit for your expat portfolio:

- ETFs: Many investors opt for a mix of developed and emerging markets, such as the iShares Core MSCI World (ISIN: IE00B4L5Y983) and the Vanguard FTSE Emerging Markets (ISIN: IE00B3VVMM84). This way, you can capitalise on the stability of established markets and the growth of emerging regions.

- P2P lending: Bondora and Mintos offer attractive returns with manageable risk, combined with user-friendly platforms, extensive experience and automation.

- Cryptocurrencies: Adding a small amount can boost your overall return. Platforms such as Binance or Trade Republic make it quick and easy to get started.

- Call money: At Trade Republic, you currently earn around 2% interest on uninvested funds (as of April 2026).

This combination offers a well-balanced investment for expats, offering long-term growth, passive income and a good level of security.

Conclusion: High-yield investments for expats in 2026

As an expat, it is essential to build a well-thought-out investment portfolio in order to achieve long-term financial freedom.

Even though your income abroad is usually fairly stable, you shouldn’t rely solely on your job or potential pay rises.

Use the investment opportunities outlined here to actively grow your capital and become more financially independent. A combination of ETFs, P2P lending and a bit of crypto provides a solid foundation. This way, you can benefit from global economic growth, receive regular interest payments and avoid having to keep an eye on share prices every day.

Many options can be fully automated, which saves you a lot of time and minimises the effort involved. By diversifying widely across asset classes and regions, you can reduce the risk of losses in the long term.

The earlier you start, the greater the impact of compound interest and the faster your wealth will grow.

With this investment scheme for expats, you can combine security with the potential for strong returns and build your future efficiently, simply and with a long-term perspective, without neglecting your life abroad.

FAQ: Frequently asked questions about investing for expats