My Afranga review: 14% interest | €3,000 invested

Afranga is a relatively unknown P2P platform from Bulgaria that has also been overlooked by Northern Finance so far. A mistake, as my personal experience shows! I have invested €3,000 so far and taken a close look at the provider for you.

In brief:

- Afranga is a peer-to-peer marketplace from Bulgaria that allows you to invest in consumer lending.

- Stikcredit, which has been successfully granting lending since 2013, is behind the platform. Other lending originators account for only a small proportion.

- The concept has been operating safely and reliably since 2021.

- My experiences have been very good so far, and I will continue to increase my investment here.

What is Afranga? All the important information + my review

The market for P2P lending has grown massively and has now reached a size that makes it difficult to keep track of. In recent months alone, new and highly interesting platforms such as Devon, FF Forest and Loanch have been launched.

It’s easy to overlook a P2P provider! Afranga is one such case: the Bulgarian platform has been delivering reliable results for investors since 2021, but has remained largely unknown.

A few months ago, I finally got started and added some investments there to my portfolio. My initial experiences have been extremely positive:

- Here, you invest directly in credit brokers (as a business loan), who in turn use this money to grant consumer loans.

- The most important credit broker behind the platform is Stikcredit. They are very successful and have substantial reserves, which speaks for the security of the offer.

- It is a financially regulated service provider that must meet strict requirements in terms of transparency and security.

- The interest rates are up to 14%, which you can increase even further with my sign-up bonus and cashback.

- Afranga recently revamped its website – and it shows! Everything looks very tidy and stylish.

Here is an overview of the most important facts about Afranga:

| Foundation | December 2020 (start: 2021) |

| Company headquarters: | Sofia, Bulgaria |

| Management: | CEO Svetlin Sabev, Founder |

| Assets under management: | €19.4 million |

| Lending financed: | Over €50 million |

| Regulated: | Fully regulated European Crowdfunding Service Provider |

| Annual report: | Available for main lender Stikcredit. Profit of €1.8 million. |

| Investors: | 2.100 |

| Returns: | Up to 14%, with Northern Finance bonus and cashback up to 15.5% possible |

| Buy-back guarantee: | Not available |

| Minimum investment amount: | 10 EUR |

| Auto-Invest: | No |

| Secondary market: | No, planned for spring 2026 |

| Tax certificate: | Yes |

| Bonus programmes: | 1% cashback + 0.5% bonus interest when you sign up via my link |

Who is behind Afranga?

If you already have extensive experience in the P2P sector, you may be familiar with Stikcredit. Among other things, the credit broker was active on Mintos and generated reliable interest rates for its investors.

The founding of Afranga was the logical next step in removing the middleman Mintos and offering even more lucrative investments. It is therefore not surprising that there is a lot of overlap in personnel between the P2P platform and the credit broker Stikcredit:

- CEO Svetlin Sabev has been with Stikcredit since 2018. He is the founder and CEO of Afranga, but remains a member of the supervisory board at Stikcredit. He is also the co-founder and managing director of Lendivo, the second-largest originator on the platform. He is therefore a well-connected expert with a wealth of experience!

- COO Veniamin Istomin is responsible for day-to-day business. The Czech manager previously gained extensive experience at the P2P marketplace Bondster, particularly in dealing with loan originators.

- CTO Zdravko G. is responsible for technology. He is an experienced software developer and manager who has worked in the fintech sector, among other areas. Afranga’s new, excellent web interface is largely thanks to him.

How the business model works

Due to regulations and the associated requirements, Afranga’s business model includes an additional step. At first glance, it seems complicated, but it is actually very simple:

- Credit brokers such as Stikcredit lend money to private individuals who cannot or do not want to turn to traditional banks (for example, because they need money very quickly).

- You receive high interest payments from your customers.

- The originators want to grow and issue even more loans. To do so, they refinance their expenses via P2P platforms, among other things.

- Private investors like you and me can provide the capital for this. In return, we receive a large share of the very high interest rates that these companies earn.

- Investors and lenders come together via P2P marketplaces such as Afranga.

Afranga is a service provider regulated by the financial authorities. As such, the platform is not permitted to offer individual lending for investment. So instead of financing a new PlayStation or car repairs for an individual customer, we make our money available to the lending originators themselves.

This means you are investing in the initiator’s entire loan portfolio at the same time! This creates excellent diversification, as you are not dependent on a single loan. The concept is similar to P2P service providers such as Bondora or Monefit, where we also invest directly in a credit company.

The disadvantage, however, is that you cannot select individual loans and focus areas in your portfolio. If you want to invest specifically in a particular type of loan, you will need to turn to competitors such as Mintos or Swaper.

Good to know:

A small portion of the interest income also goes to Afranga itself. However, as it is a platform specifically designed to finance Stikcredit, Afranga’s profit is less significant.

Which lending can you invest in with Afranga?

Through Afranga, you invest in personal loans, i.e. money that individuals borrow to cover purchases, unexpected expenses or the waiting period until their next salary. It is the most popular loan category in my P2P lending comparison.

However, Afranga can cause confusion:

- We grant a corporate loan to the respective loan originators via the platform itself.

- The credit brokers, in turn, grant consumer loans to private individuals.

- Strictly speaking, we are therefore investing in business loans here. However, the profits from which our interest is paid are generated by personal loans.

The distinction has no real impact. You will reliably receive your interest, regardless of whether it is labelled a ‘business lending’ or a ‘personal lending’. In my experience, however, misunderstandings arise time and again because all loans available at Afranga are labelled as ‘business lending’.

How to register with Afranga

Does up to 15.5% interest sound attractive to you? Then it’s high time to register via my link!

The registration process is relatively extensive, as Afranga, as a regulated provider, has to meet numerous requirements. However, most of the questions are simple, and you just need to click on the options that apply to you. In my experience, despite the extent of the process, it only takes a few minutes to complete.

You must meet the following requirements:

- You are a citizen (or have your residence/tax residence) in an EU country or Switzerland.

- You have a bank account to deposit money into your Afranga account.

- You are at least 18 years old

- You have an email address, a mobile phone number and a smartphone with an internet connection.

My link will take you to the Afranga website. Here, select the green ‘Create Account’ button in the top right-hand corner.

Let’s start with the basics: enter your first and last name, email address, telephone number and choose a password.

Good to know:

Companies can also invest via Afranga! You must select the ‘Company’ tab at the top. However, as private individuals make up the majority of investors, the correct option, ‘Individual’, is already preselected.

Once you have entered all the information, you will be immediately redirected to a confirmation page. Afranga shows you how far along your registration process is. The company tries to take you by the hand and guide you through the process. In my experience, competitors tend to leave you to your own devices.

Your account has now been created, but you still need to fill it with funds before you can start investing.

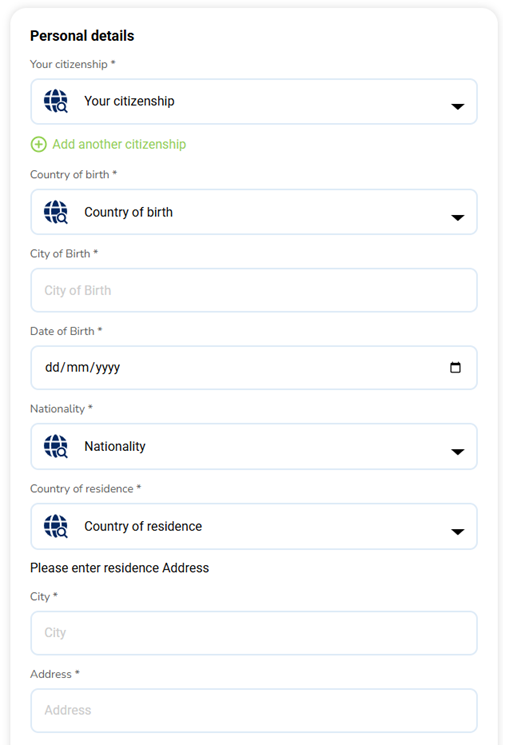

Enter personal details

When you click on ‘Continue’, an input mask will appear, requesting your personal details. Here are the required items in order:

- Your citizenship(s). If you have more than one, you can add them using the green plus symbol.

- Your country of birth

- The town where you were born

- Your date of birth

- Your nationality (an unnecessary field. Simply select the same option as above under ‘Citizenship’)

- Country of residence

- Your address (town, street and house number, postcode)

Further down (‘Other Information’), you can add your birth name and an address supplement, if necessary.

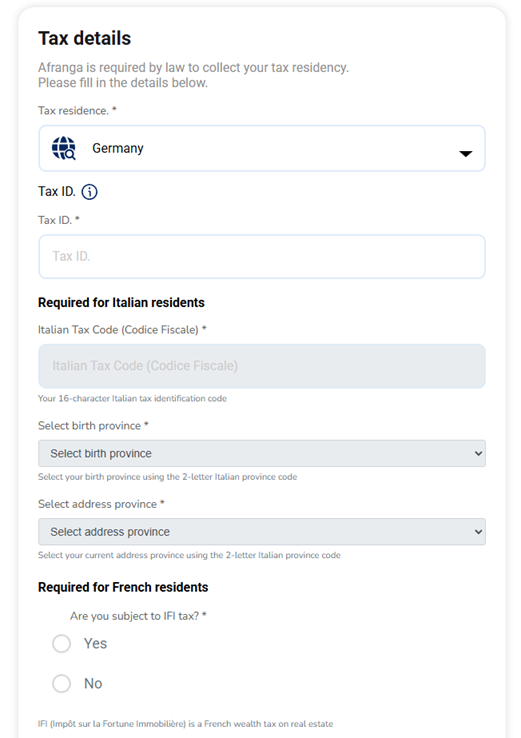

Enter tax details

The profits you make on Afranga must, of course, be included in your P2P tax return later on. The platform itself must also record your income correctly, as it is a regulated provider. Next, you will be asked to provide your tax details:

- Country where you pay taxes

- Your tax number. You can find it on your income tax assessment and some other documents from the tax office, for example.

- Additional information for persons residing in Italy or France

- Your profession/occupation. Here, people tend to be unnecessarily specific, and in my experience, the many English terms can quickly cause confusion. I recommend using a translation plug-in here.

Answer questions about yourself

Immediately afterwards, Afranga wants to know whether you are a ‘politically exposed person’. If you (or a close relative) hold an important political office, for example, the answer is “Yes”. Otherwise, select ‘No’.

This is followed by the question of legal capacity:

- “Full legal capacity” = Full legal capacity

- Limited legal capacity = Restricted legal capacity

- “Under guardianship” = Under guardianship (not legally competent)

Next, they want to know how much you earn annually and what your sources of income are. You can select multiple options here.

- ‘Income’ is probably the most common choice and refers to all income from self-employed or employed work.

- In my experience, financial investments are also very important. These include income from other P2P platforms, dividend ETF payouts and other passive income.

- The other options are quite specific, but may be relevant to individual investors. Here, you must make the appropriate choice yourself.

If you select several items, you will also be asked what your main source of income is.

Finally, you must declare your total assets, i.e. your capital, investments, property, etc.

Complete verification

You’re almost done! Just check your telephone number and the information you’ve entered one last time, and you can continue with the verification process.

You will need your smartphone to confirm your identity. You must take a photo of your ID document and a selfie. Everything is done automatically and you will not have any contact with a service representative.

After a few seconds, your registration will be complete and you will receive a confirmation email. You can now deposit money and start investing!

My Afranga review: How I earn 14% interest

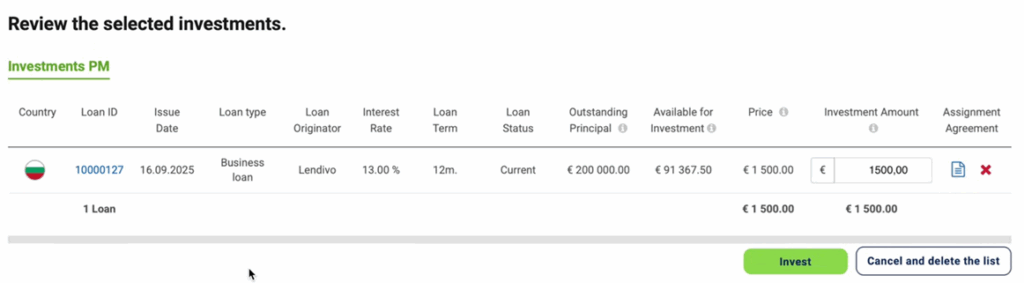

At Afranga, several loan originators are available for investment. I opted for the two largest companies, as they also have the most experience in the P2P sector and the largest lending portfolio.

I invested €1,500 in each of the two providers:

- Stikcredit is the driving force behind Afranga. With a loan portfolio of €22 million (€5 million of which is financed through Afranga), it is also the largest provider on the platform. Depending on the term, the interest rates offered are up to 14% per annum.

- Lendivo is a Bulgarian credit broker founded by the Stikcredit team. On Afranga, this provider has already received €4 million (since regulation in February 2025) in investments. Here, you can earn up to 13% interest per year.

Thanks to the combination of two investments and the currently available cashback bonus, my interest rate has stabilised at just over 14%. This is a very good rate for a platform that has been paying out reliably for several years!

Tax at Afranga: A minor disadvantage of the Bulgarian platform

A glance at my P2P lending ranking immediately shows that all interesting providers are based outside Germany. Unfortunately, many countries levy withholding tax on the profits we earn there. However, we can usually offset this against our own tax in Germany without any problems, so there is no loss.

Unfortunately, this is not the case with Afranga:

- Afranga is based in Bulgaria.

- Bulgaria and Germany have a double taxation agreement that should actually prevent double taxation.

- Unfortunately, this rule does not apply to the winnings you earn at Afranga.

- The provider will deduct 10% of your earnings directly and pay it to the Bulgarian tax office.

- You CANNOT claim these deductions on your tax return and thus get them back.

It is important to emphasise that this is 10% of your profits and not 10% of your capital! In plain language, this means that your return will decrease by 10% as a result of this tax.

In my case, I earn around 1.4% less per year (1/10 of 14% = 1.4%) or 12.6%, which is still an attractive amount for me.

Note: According to information on the Afranga website, 5% of the withholding tax retained should be creditable in the income tax return. In this case, the total return would not be reduced by 10%, but effectively only by around 5%, which would correspond to a return of approximately 13.3%. This does not constitute tax advice.

Afranga risk explained: How dangerous is the P2P platform?

P2P lending are not exactly among the safest investments – double-digit interest rates can only be achieved with a certain amount of risk! However, there are significant differences between individual providers, and it is very important to take a close look at security.

Afranga is doing very well here:

- Afranga is a government-regulated platform that has to meet very high standards. These include, for example, a high level of transparency so that we can identify any problems in good time. The mandatory separation of company capital and investor capital also benefits us.

- The risk of individual loan defaults (a borrower is unable to repay their debt on time or at all) is significantly reduced. This is because you invest directly in the loan originators and do not have to deal with private customers yourself.

- The platform is backed by the credit broker Stikcredit, which has been operating very successfully for many years. The company has already weathered the COVID crisis and the war in Ukraine and has sufficient reserves to overcome any future problems.

- Afranga itself has been active since 2021 and has not recorded a single loan default since then! Investors have always received their interest payments on time, even when the economy was weak or the stock markets collapsed.

Overall, Afranga therefore offers the highest level of protection conceivable for P2P investments. While there is no such thing as 100% security, given the very attractive interest rates, I find the residual risk to be entirely acceptable.

Advantages and disadvantages of Afranga

Based on my experience with Afranga, I can see several clear advantages, but also disadvantages:

| Advantages | Disadvantages |

| Attractive interest rates of up to 14% per annum, which can be further increased through various bonuses | Basic risk: double-digit interest rates always come with a fundamental risk. |

| The platform is regulated by the authorities and meets the highest standards of transparency and security. | Website currently only available in English and Bulgarian |

| Solid selection of different credit companies and terms | Withholding tax is not creditable, so we lose around 10% of our return. |

| Behind the platform is Stikcredit, which has been operating successfully for years and has been able to overcome past crises without any problems. | Due to official regulations, the registration process is rather cumbersome. |

| Since its foundation in 2021, Afranga itself has always paid interest reliably and has not yet recorded any loan defaults. | The platform is still quite small (currently around 2,000 investors), making long-term forecasts difficult. |

| The two most important credit facilitators, Lendivo and Stikcredit, are growing steadily and form a secure anchor for Afranga. | A secondary market is not yet available (but is in the planning stage). Therefore, it is not possible to exit an investment prematurely. |

Overall, my opinion of Afranga is therefore positive. In my experience, it is a reliable platform with good interest rates, which offers additional security thanks to its regulation.

Possible alternatives to Afranga

In my opinion, Afranga does a lot of things right, but it also faces stiff competition. If the Bulgarian provider doesn’t appeal to you, there are numerous alternatives available:

1. Debitum Investments

With Debitum Investments, you also invest in business loans and receive around 13% interest per annum. In addition, both Debitum and Afranga are very stable platforms that have been paying out reliably for years. And you don’t have to compromise on transparency with either of them.

Debitum could therefore be a possible alternative or supplement to an Afranga investment: by dividing your money between both providers, you can achieve even greater diversification!

2. Monefit

Monefit pursues a slightly different business model, but is similar to Afranga in that you do not invest in individual consumer loans here. Instead, you make your capital available directly to a loan originator, in this case the Creditstar Group.

In return, you will receive ‘only’ 7.5% interest, but you can withdraw your capital at any time! This is a major advantage over traditional, fixed-term P2P investments.

I have already had very good experiences with this offer and use it as a lucrative alternative to instant access savings accounts.

Conclusion: Good experiences with Afranga – I have increased my investment!

Afranga is a Bulgarian P2P platform that is known to only a few investors. However, it is well worth investing in: currently, there is up to 14% interest per annum, which can be increased to 15.5% through my registration link and a cashback bonus!

At the same time, Afranga offers a high level of security, as the platform is regulated by the authorities. This ensures a high degree of transparency and additional protective mechanisms that benefit us as investors.

Furthermore, the provider behind the credit broker is Stikcredit, which has been operating very successfully for many years. This puts Afranga on a secure footing, as its large reserves and healthy profits should enable it to weather any future crises.

Based on my experience so far, I can only see one serious disadvantage: the 10% withholding tax cannot be credited in Germany. This means you lose a tenth of your return. However, in my opinion, the remaining 90% is still very attractive.

Afranga is therefore a new addition to my portfolio, and one that is sure to play an important role in the future.

FAQ: Frequently asked questions about Afranga