Investing for civil servants: Secure assets through ETFs & P2P

You are a civil servant and have a secure job, but still wonder whether that will be enough in the long term? A relaxed life in old age, educating your children or owning a home in a good location are now much more expensive than they were a few years ago. Despite the security they offer, civil servants’ salaries often fail to keep pace with the rising cost of living, especially in large cities.

If you want more than the bare minimum, you have to take action yourself. As a civil servant, you are in an ideal position to make smart provisions early on. Today, I will show you how you can build up your assets with a solid investment to become more financially independent in the long term.

In brief:

- As a civil servants, you have a secure but limited income, so you need investments that allow your money to work effectively for you.

- ETFs are a stable foundation that is well suited for long-term capital accumulation with good growth.

- P2P lending provides regular interest payments, regardless of stock market movements.

- Cryptocurrencies are suitable as a small addition for additional potential.

- Automation enables you to invest efficiently even alongside a busy working life.

Why is investing money so important for civil servants?

civil servants generally receive a good, stable salary, but it is not necessarily above average. Becoming a civil servants offers you security and a state pension, but in many federal states, civil servants’ salaries have barely kept pace with inflation and the cost of living.

In addition, your pension will only amount to a certain percentage of your last salary, while your expenses in old age are unlikely to decrease significantly. If you want to maintain your standard of living in retirement, you should make provisions for this yourself in good time. The later you start investing, the more returns you will miss out on due to the lack of compound interest.

What makes investing even more relevant for civil servants:

- Limited salary growth: Promotions and pay adjustments are largely predetermined and predictable, but not exorbitant. Investments can help supplement your income in the long term.

- Inflation and loss of purchasing power: Even with stable income, real purchasing power declines a little more each year. Long-term investments compensate for this and protect your assets from devaluation.

- Job security: Your stable job allows you to invest regularly without any existential risks. This consistency is a huge advantage for building wealth, which you should take advantage of!

With a sound investment strategy, you can invest your income in such a way that it works for you in the background. Over the years, this can generate considerable additional wealth, making you more independent in retirement or even allowing you to slow down earlier.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

Investing money for civil servants: This is how much you can achieve

The earlier you start, the better the compound interest effect works for you. Not only does your invested capital earn interest, but so do the returns you have generated in the meantime, i.e. interest on your interest. If you invest regularly at a good rate of return, this creates a kind of snowball effect over time, even with moderate amounts. You benefit from this in the following ways:

- Greater security in retirement, regardless of how much your pension is or how remuneration systems develop.

- More freedom in your professional life, for example to work part-time, support your family or simply live more independently financially.

- Build up assets that will give you long-term security, for example for buying a house or covering unexpected expenses.

The longer your investment horizon and the higher the average return, the greater the effect. This means that your capital grows faster with each passing month and you get a little closer to your goals every year.

You can see how much this can pay off over time in this example, based on a conservative 8% annual return:

| Monthly amount | 5 years | 10 years | 20 years | 25 years | 30 years |

| 250 € | 18.369 € | 45.736 € | 147.255 € | 237.757 € | 372.590 € |

| 500 € | 36.738 € | 91.473 € | 294.510 € | 475.513 € | 745.179 € |

| 1000 € | 73.477 € | 182.946 € | 589.021 € | 951.027 € | 1.490.360 € |

Over the course of your entire civil service career, this can add up to several hundred thousand euros! Regular financial investment for civil servants therefore literally pays off.

In the best-case scenario, you can withdraw a few per cent of your saved assets each year. For example, a 5% payout per year can result in around €40,000 to €50,000 in additional income annually without touching your original capital!

Which types of investment are particularly suitable for civil servants?

As a civil servant, you have a high degree of job security, but that is precisely why the issue of capital growth is often underestimated. However, with rising living costs and limited pay rises, it is important that your money does not just sit in your account, but works for you. The best way to do this is to invest in solid, automatable investments with a reasonable risk-return ratio.

These two asset classes complement each other perfectly:

- ETFs (Exchange Traded Funds): These track entire markets and grow in line with the global economy over the long term.

- P2P lending: Specialised platforms allow you to lend money directly to private borrowers or companies. In return, you receive ongoing interest payments, usually on a monthly basis, regardless of stock market fluctuations.

ETFs and P2P loans thus combine the best of both worlds: on the one hand, you generate a good return for long-term wealth accumulation, even if the markets fluctuate somewhat in the meantime. On the other hand, you receive ongoing interest income and thus have a stable additional income, regardless of what is happening on the stock market.

ETFs: Invest easily, profit globally

Exchange traded funds track entire markets or indices, such as the MSCI World or S&P 500. When you buy shares in an ETF, you automatically invest in many companies at once and benefit from their growth. Administration, dividends and rebalancing are handled by the fund, so you don’t have to worry about any of that.

Example:

The S&P 500, one of the best-known US indices, has achieved an average annual return of 9.06% over the last 20 years (source:https://www.investopedia.com/ask/answers/042415/what-average-annual-return-sp-500.asp). This shows that those who invest in this form of investment over the long term are participating in global economic growth!

What makes them particularly worthwhile as investments for civil servants:

- A stable foundation for your portfolio: ETFs fluctuate, but significantly less than individual shares. This makes them the ideal basis for sustainable capital growth.

- Minimal effort: You can use them as an ETF savings plan or a one-off investment. Once set up, your ETF savings plan runs automatically without you having to check charts every day.

- Broad diversification: Your assets are spread across many countries, sectors and companies. This reduces the risk of losses if individual companies lose value or in times of economic uncertainty.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

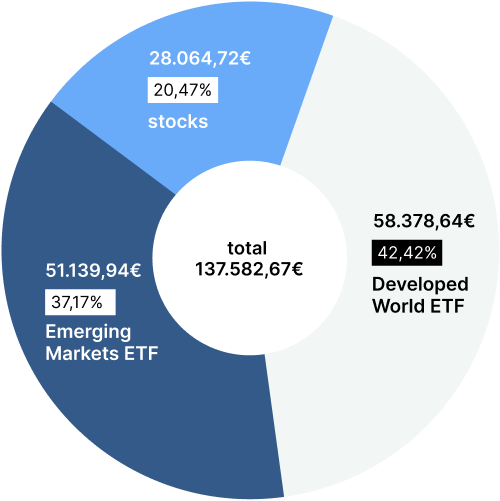

How I use ETFs to achieve a 9% return

In my portfolio, I combine approximately 37% industrialised country ETFs and 42% emerging market ETFs. This gives me stability from Western countries and, at the same time, growth potential for above-average returns from emerging market ETFs. I manage my portfolio on Scalable Capital, where I particularly like the wide selection and free ETF savings plans. The fact that the accompanying app is super easy to use is an added bonus for me!

This is what your start could look like:

- Select two broadly diversified global funds (e.g. World + Emerging Markets).

- Set up a monthly, automated savings plan.

- Check about once a year whether your target ratio in your portfolio has changed. If necessary, rebalance it accordingly.

This combination makes it easier for you to systematically build up your assets with little administrative effort. Your capital is spread globally and you receive robust returns. The perfect foundation for a successful long-term investment!

P2P lending: Additional income regardless of stock market performance

P2P stands for peer-to-peer, and it involves investing directly in loans to individuals or businesses. This is done through specialised platforms such as Bondora or Mintos, which handle the lending, credit checks and repayment processing. In return, you receive the interest accrued.

Because there is no middleman in the form of a bank, the profits go straight to you. Currently, returns of around 6% to 15% per year are realistic. That is significantly more than any bank offers, making it an ideal alternative to instant access savings accounts!

In practice, the principle works as follows:

- Borrowers submit applications, e.g. for car repairs, investments or short-term liquidity.

- The platform checks creditworthiness and risk profile and decides whether and on what terms the loan will be granted.

- Your money is invested together with other investors, either as many small loan shares or in specific loans that you can select according to various criteria, depending on the platform.

- Borrowers make monthly repayments, including interest, which you receive on a pro rata basis.

- The platform takes care of everything else, such as billing, monitoring and, if necessary, reminder processes.

Why investing money is particularly interesting for government emplyees:

- Predictable additional income: Most platforms pay out interest and repayments on a monthly or even daily basis. This is perfect if you are looking for a regular source of additional income.

- Stock market-independent returns: Even if share prices fall, your credit investments will still generate repayments and interest.

- Minimal effort: Features such as Auto-Invest at Mintos or Go & Grow at Bondora take care of selecting individual loans for you.

This makes this type of investment the perfect second pillar in your portfolio! With P2P, you generate passive income while simultaneously building long-term wealth with ETFs. This reduces fluctuations in your overall portfolio, ensuring greater financial stability, especially if you have longer-term goals in mind.

1. Easy to get started: Invest effortlessly and earn interest daily with Bondora

If you are looking for a simple P2P solution, you can invest in Bondora’s Go & Grow. You deposit funds into your account, which the platform automatically distributes across many small loans. You receive daily interest, currently 6% per annum.

Advantages:

- Super simple: you don’t need to select loans or invest manually because everything works automatically.

- Available daily: You can access your credit at any time; it is usually paid out within one working day.

- Passive income: Interest is credited to your account daily. I think this type of regular income is great!

What you should know:

- Although Bondora is one of the most established P2P providers, this does not make the investment completely risk-free. Even if defaults are cushioned by provisions, it remains an investment in loans.

Nevertheless, Bondora has been on the market for over 17 years and now has 500,000 investors. To date, a total of €1.7 billion has been invested and around €159 million in returns has been paid out. This definitely makes it a stable platform!

2. Stay flexible: actively select and achieve high returns with Mintos

If you would like to manage your investment in a more targeted manner, Mintos is an exciting option. As one of the largest P2P platforms in Europe, it allows you to invest in loan portfolios from a wide range of providers. These include consumer and business loans from many countries. I find it particularly convenient that you can choose between fully automated investment (Auto-Invest) or manual selection.

Advantages:

- High returns: Depending on the risk profile, 6% to 15% per annum is realistic.

- Buy-back guarantee: Many lenders will buy back loans in the event of late payments.

- Flexible automation: You decide whether you want to configure Auto-Invest according to your criteria or invest manually.

- High diversification: Your capital is spread across different borrowers and regions, which reduces your risk.

What you should know:

- In the past, there have been defaults by lenders, which is why some repayments have been delayed or only partially received.

- Mintos offers many options, but this makes it somewhat more complex to use. You should allow for a certain amount of familiarisation time or start with small amounts.

3. Sustainable interest rates at Ventus Energy

Ventus Energy offers you the opportunity to invest directly in renewable energy and energy infrastructure projects, such as wind power, photovoltaics and energy storage. In doing so, you actively support the energy transition and receive regular interest payments in return.

Advantages:

- Attractive target returns of approximately 17% per annum

- Daily interest credits that you can reinvest directly

- High transparency across all projects and repurchase options offered

What you should know:

- Ventus Energy is not suitable for small amounts; the minimum investment is usually €1,000.

- Energy projects are subject to market and price fluctuations, so you must expect higher risk here.

Ventus Energy is currently undergoing restructuring and is not accepting new investors or investments. That's why I'm investing my new funds on Monefit. As a welcome gift, you'll receive a €5 bonus + 0.75% (for 90 days).

Portfolio proposal for financial investments for civil servants

In my portfolio, you can see how I use a mix of different asset classes to not only build long-term wealth, but also generate additional monthly income. You can either adopt it directly or adapt it to your specific needs; the system behind it remains the same:

- the highest possible return with moderate risk,

- regular returns for greater flexibility,

- Automate financial investments as much as possible.

Depending on how risk-averse you are and what your personal circumstances are, you can structure your investments in different ways. While some people prefer stability, others may want to add more promising investments with a little more risk to their portfolio.

Here are two examples of what a mix might look like, both with a high degree of automation and passive income as the goal:

1. Conservative portfolio for security and stability

| Investment | Share in the portfolio | Goal |

| ETFs | 70 % | Long-term, stable growth |

| P2P lendings | 20 % | Regular cash flow |

| Cryptos | 5 % | Additional yield driver |

| Call money | 5 % | emergency reserve |

2. Aggressive portfolio with a focus on returns

| Investment | Share in the portfolio | Goal |

| ETFs & individual shares | 50 % | Long-term, global growth |

| P2P lendings | 25 % | Regular interest income |

| Cryptos | 20 % | High return potential with higher risk |

| Call money | 5 % | Short-term reserves for emergencies |

Why this combination makes sense as an investment for government employees:

- ETFs form the foundation of your portfolio. You benefit from global economic growth in the long term, with calculable risk and comparatively moderate fluctuations in the meantime.

- P2P brings in additional income. Regular interest payments mean liquidity and further stabilise your income without requiring much effort on your part.

- Cryptocurrencies are significantly more volatile, but can significantly increase your overall portfolio return.

- Your instant access savings account is your financial safety net for absolute emergencies.

You can specifically incorporate these products:

- ETFs: My portfolio contains a mix of developed market and emerging market ETFs, such as Vanguard FTSE Developed World and iShares Core MSCI World, as well as Vanguard FTSE Emerging Markets / iShares Core Emerging Markets. This combination allows you to invest in established developed markets while also benefiting from growth opportunities in emerging markets.

- P2P lending: For solid returns at medium risk, you can invest in Go & Grow (formerly Bondora Go & Grow) or Mintos, for example. Both providers are very easy to use, well established in the market and make automated investing easy for you. This saves time and earns interest!

- Cryptocurrencies: As a small addition to your portfolio, cryptocurrencies can significantly increase your overall return. If you don’t want to participate in day trading, you can use Binance, for example. Personally, I am very happy with the platform because it offers me a wide selection of coins and makes buying and holding easy without having to spend a lot of time on it.

Investments always involve the risk of loss. The value of your investments

can go up or down. The forecast or past performance is no guarantee or

prediction of future results.

Do your own research or seek financial advice before making any invest-

ments. The WELCOME promotion is subject to Terms and Conditions. Gift

Shares are allocated randomly from a selection of eligible stocks, with high-

er-value shares awarded less frequently.

My conclusion: high-yield investments instead of overnight money

A stable financial investment for civil servants works best with a well-thought-out portfolio. You may have a reliable income, but especially with only small salary increases, it is important that you let your capital work for you.

With ETFs, P2P loans and a small portion of cryptocurrency, you can build a robust foundation for the long term. You benefit from global economic growth, receive regular interest payments and don’t have to follow the stock market news every day.

Automation takes most of the work off your hands and reduces your risk through broad diversification. And the sooner you start, the faster you can grow your money and take advantage of the snowball effect!

FAQ – Frequently asked questions